Download

1 / 35

350 likes | 454 Views

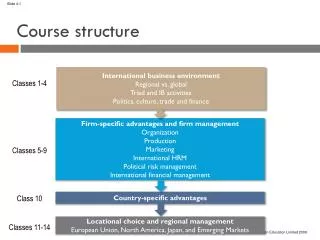

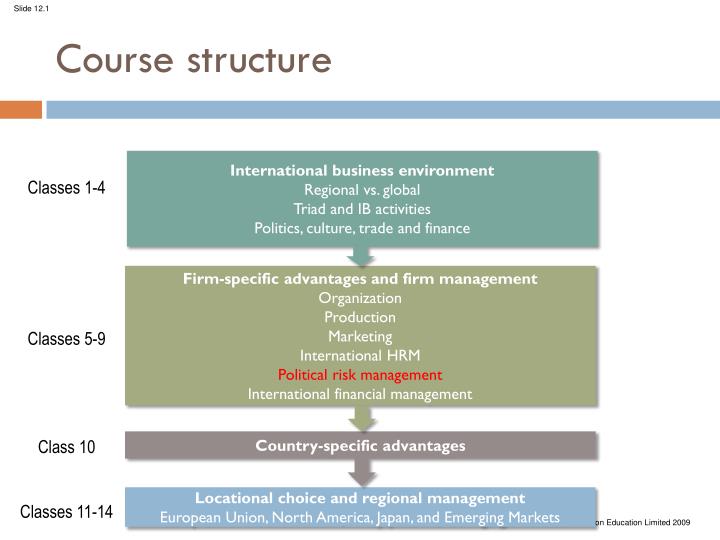

Course structure. Classes 1-4 Classes 5-9 Class 10 Classes 11-14. International business environment Regional vs. global Triad and IB activities Politics, culture, trade and finance. Firm-specific advantages and firm management Organization Production Marketing International HRM

E N D

Course structure Classes 1-4 Classes 5-9 Class 10 Classes 11-14 International business environment Regional vs. global Triad and IB activities Politics, culture, trade and finance Firm-specific advantages and firm management Organization Production Marketing International HRM Political risk management International financial management Country-specific advantages Locational choice and regional management European Union, North America, Japan, and Emerging Markets

Political risk • Political risk: The probability that political forces will negatively affect a multinational’s profit or impede the attainment of other critical business objectives. A very recent example: “Negotiations for a major free-trade agreement between the European Union and the U.S. have been postponed after Washington expressed its inability to continue them because of the partial government shutdown. Officials from EU member-states and the U.S. were scheduled to meet in Brussels next week to discuss the Transatlantic Trade and Investment Partnership, or TTIP, which upon its successful conclusion would be the world’s largest free-trade pact. However, U.S. Trade Representative Michael Froman informed EU officials Friday that the federal government shutdown has made it impossible to send a negotiating team to Brussels as scheduled.” Source: International Business Times, October 10, 2013, 3:12PM EDT. http://www.ibtimes.com/us-government-shutdown-hits-free-trade-pact-talks-eu-1415360

Political risk Unstable political forces (e.g., government, legal system, etc.) Some examples: • Expropriation (with/without compensation) • e.g., in Oct 2010, Venezuelan president Hugo Chavez’s forced takeover of Agroislena, a Spanish vendor of agricultural products that has operated in Venezuela for more than 50 years. • Indigenization laws • e.g., on March 9, 2008, Zimbabwe’s President Robert Mugabe signed the Indigenization and Economic Empowerment Bill into Law. The bill gives indigenous Zimbabweans the right to take over and control over many foreign owned companies, where an indigenous Zimbabwean is defined as “any person who before the 18th of April 1980 was disadvantaged by unfair discrimination on the grounds of his or her race, and any descendent of such person”. • Restriction of operating freedom, e.g., hiring and production • Breach of contracts • Damage to property and/or personnel from terrorism, riots, etc. • Loss of financial freedom • Increased taxes and other financial penalties

Levels of political risk • Macro political risk: a risk that affects all foreign enterprises in the same way. • Micro political risk: a risk that affects selected sectors of the economy or specific foreign businesses.

Types of political risk • Legal/governmentalrisks: are potentially harmful to foreign businesses but are the product of, or permissible within, the existing political, economic and legislative system. • Non-legal or extra-governmentalrisks: lie outside the system and are a violation of existing laws.

Recent evidence in aluminum industrySource: Jo Jakobsen (2010). Old problems remain, new ones crop up: Political risk in the 21st century. Business Horizon, 53, 481-190. • Guinea: in April 2007, when the former civilian government moved to withdraw the agreement it had made with Russian aluminum giant Rusal, allegedly as part of a planned review of mineral contracts in general. • Micro & legal/governmental

Recent evidence in aluminum industry (cont’d)Source: Jo Jakobsen (2010). Old problems remain, new ones crop up: Political risk in the 21st century. Business Horizon, 53, 481-190. • Azerbaijan: in March 2006, the government moved to terminate the 25-year contract it held with Dutch company Fondel for management of the Azeralumnium smelter, opting instead to take over management of the plant itself. To avoid a blatant case of breach of contract, the government contended that certain aspects of the contract were “against Azerbaijan’s interests” • Micro & legal/governmental

Recent evidence in aluminum industry (cont’d)Source: Jo Jakobsen (2010). Old problems remain, new ones crop up: Political risk in the 21st century. Business Horizon, 53, 481-190. • The Dominican Republic: in October 2008, U.S. bauxite miner Sierra Bauxita Dominicana had to leave the country because of Dominican government’s expropriation of the firm’s bauxite deposite at a port in the Caribbean country without compensation. • Micro & legal/governmental

Recent evidence in aluminum industrySource: Jo Jakobsen (2010). Old problems remain, new ones crop up: Political risk in the 21st century. Business Horizon, 53, 481-190. • Guinea: In November 2008, aluminum majors Rusal, Alcoa, and Alcan were forced to stop production and evacuate employees because of several social unrest. • Macro & non-legal/extra-governmental

Recent evidence in aluminum industry (cont’d)Source: Jo Jakobsen (2010). Old problems remain, new ones crop up: Political risk in the 21st century. Business Horizon, 53, 481-190. • Nigeria: in June 2007, six Russian workers employed by Rusal were kidnapped, and their Nigerian driver killed, by gunmen entering Rusal’s residential compound in Ikot Abasi, Nigeria. The abductees spent over 2 months in captivity, before being released physically unharmed in August. • Micro & non-legal/extra-governmental

Recent evidence in aluminum industry (cont’d)Source: Jo Jakobsen (2010). Old problems remain, new ones crop up: Political risk in the 21st century. Business Horizon, 53, 481-190. • Brazil: in 2004, local environmentalists and protests, who are afraid of being resettled, succeeded in delaying a $400 million hydroelectric power project in Brazil – a project whose purpose was to secure access to cheap energy used in primary aluminum production. The project consortium, led by Alcoa, eventually had to agree to a substantial compensation package and to increase its spending on environmental measures. • Micro & non-legal/extra-governmental

Does (why does) political risk will deter FDI? Empirical evidence. Logarithm of (FDI stock)

Quantifying risk vulnerability • All risk is relative. • The political/legal, economic, socio-cultural and technological environment of a foreign country has different implications depending on the type of international business that a firm is evaluating. • For example: export restrictions are more important if a firm is seeking to set up a plant to produce goods for exports than if the products are for the local market. Weighted Country Risk Assessment Model

The Weighted Country Risk Assessment Model Sources: The approach and the items in the table draw from prior risk assessment models and studies, including D. W. Conklin, “Analyzing and Managing Country Risks,” Ivey Business Journal, vol. 66, no. 3 (January/February 2002), pp. 36–42; S. T. Cavusgil, “Measuring the Potential of Emerging Markets: An Indexing Approach,” Business Horizons, vol. 40, no. 1 (1997); A. I. J. Dyck, Country Analysis (Boston, MA: Harvard Business School Press, 1997); E. Dichtl and H. G. Köglmayr, “Country Risk Ratings,” Management International Review, vol. 26, no. 4 (1986), pp. 4–12

The Weighted Country Risk Assessment Model (Continued) Sources: The approach and the items in the table draw from prior risk assessment models and studies, including D. W. Conklin, “Analyzing and Managing Country Risks,” Ivey Business Journal, vol. 66, no. 3 (January/February 2002), pp. 36–42; S. T. Cavusgil, “Measuring the Potential of Emerging Markets: An Indexing Approach,” Business Horizons, vol. 40, no. 1 (1997); A. I. J. Dyck, Country Analysis (Boston, MA: Harvard Business School Press, 1997); E. Dichtl and H. G. Köglmayr, “Country Risk Ratings,” Management International Review, vol. 26, no. 4 (1986), pp. 4–12

Political risk protection • Indirect approach • A priori analysis • Risk transfer (e.g., sell out the politically risky assets) • Risk insurance (e.g., purchase a political risk insurance policy) • Direct approach: negotiation with the host government

Negotiation for political risk mitigation Host Country Has: Natural resources Physical infrastructure Labor costs Human capital – productivity Support industries/services Science and technology infrastructure Domestic market-size of market: Per capita GDP (buying power) + potential future growth Policies toward FDI: openness; liberalization + incentives to attract FDI Economic stability Political stability: risk MNE Wants: Access to raw materials Cheaper products/manufacturing base Access to technology/expertise Market access Investment in growing firms (including equity in privatized firms) Host Government Wants: Employment Technology transfer + training (knowledge transfer) Capital investment Local multipliers Increased exports (forex earnings)

New theories and practices Two of my research papers in 2013

Case Study 1:Political risk management through business-government negotiation Mining MNEs in Tanzania Summarized from Jing Li, Aloysius Newenham-Kahindi, Daniel M. Shapiro, and Victor Zitian Chen (2013). “Bargaining model revisited: Theory and evidence from China’s natural resource investments in Africa”. Global Strategy Journal, forthcoming.

Interviews • A case study on mining firms’ investment in Tanzania, a politically risky country • Time of the interviews: • May-Jun 2010 • Jul-Aug 2011 • Sample organizations interviewed: • 4 Western (2 Canadian, 1 Australian, and 1 British) • 2 Tanzanian government officials • 5 Chinese (3 state-owned and 2 privately owned) * • * we suspect that Chinese firms/government are different.

One-Tier Bargaining Model (Traditional) • Based on developed-market MNEs with firm-specific advantages (FSAs) Host-Country Government MNEs

Findings: Two-Tier Bargaining Model (US, UK, Germany, Australia) Home-Country Government Tier-1 Bargaining Official development assistance Friendly FDI environments General information Host-Country Government Investment opportunities Community modernization Each MNE Tier-2 Bargaining

Findings: The Modified One-Tier Bargaining Model (Chinese) Host-Country Government Home-Country Government Each MNE Consortia of MNEs

Findings: The Modified One-Tier Bargaining Model (Chinese) Host-Country Government Official development assistance Infrastructure improvement Multiple purpose projects Friendly FDI environments Investment opportunities Home-Country Government Promise executers Investment opportunities Collaboration opportunities Infrastructure support Financial resources Consortia of MNEs

Case Study 2: Political risk management through creative strategy International private equity/venture capital (PE/VC) in China Summarized from Sunny Li Sun, Victor Zitian Chen, Mike W. Peng, and Liang Hao (2013). The process of international institutional entrepreneurship: Transfer of equity ratchet in China. working paper.

Political risks facing international PE/VC in China • Required political environment for PE/VC • Strong rule of law that enforces contracts specifying the rules of forming and transferring equity ownership before it’s actually listed in the capital market • Strong property-rights defining and protecting the possession and transfer of equity ownership • Strong credit system that tracks and sanctions credit history • Strong capital market allows capital exit through initial public offerings (IPOs) • Corrupt legal-political system and market failures in China • Weak rule of law featured by weak legal enforcement • De facto lack of property-rights regime • Nonexistence of credit system (no sanctions on credit default) • Non-fluent capital market

Successful international PE/VCs in China • A consortium of Morgan Stanley (US), CDH Investment (Hong Kong), and ACTIS (UK) invested in Chinese Mengniu, a dairy products manufacturer and retailer, in October 2002 and October 2003 and successfully cashed in HK$ 2.61 billion via Mengniu’s IPO in Hong Kong. • A consortium of Morgan Stanley (US) and CDH Investment (Hong Kong) invested in Chinese Yongle, an electronics and appliances retailer, in January 2005 and cashed in HK$0.84 billion via Yongle’s IPO in Hong Kong. • Morgan Stanley (US) invested in Chinese Dongxiang, a sportswear manufacturer and retailer, in May 2005 and cashed in more than HK$2.5 billion in Dongxiang’s IPO in Hong Kong. • A consortium of Deutsche Securities Nominees (HK), Baytree Investment (Mauritius), and Indopark Holdings (US) invested in Evergrande, a Chinese real estate company, in 2007 and cashed in via Evergrande’s IPO in Hong Kong.

Strategy 1: creation of a flexible deal • Introduced a new practice into China which focuses on monetary motivation and flexibility under uncertainty • Equity ratchet • a contingent contract between an PE/VC investor and an investee (e.g., entrepreneur, top management of a private company, etc.) • Benchmarking the performance of a firm to a future target (e.g., IPO, stock price at IPO, growth rate, profitability, etc.) • Grants VC/PE a higher ownership from the management if the management underperforms the target • Grants the management a higher ownership from the VC/PE if the management overperforms the target • Expires without exercise if the management simply meets the target

Strategy 2: locational choice at the sub-national level • Three coastal economic centers (Bohai Gulf, Yangtze River Delta, and Pearl River Delta) are less politically risky. • More transparent governments • More effective legal enforcement • More advanced market development (capital markets in both Shanghai and Shenzhen)

Strategy 2: locational choice at the sub-national level Dongxiang @Beijing Yongle @Shanghai Evergrande @Guangzhou

Strategy 3: careful partner selection The underlying theory: when formal institutions such as political system do not work stably and effectively, business has to rely on the prevailing informal institutions such as cultures and norms to enforce cooperation and transactions.

Strategy 3: careful partner selection (cont’d) • Carefully selected Chinese investees • Strong informal institutions in China (recall the Google case) • Political connections • Chen Xiao, CEO of Yongle, was a former VP of Yongle Appliance Company, a large scaled state-owned enterprise (SOE) • Social trust and “face/image” reputation • Gengsheng Niu, CEO of Mengniu, was a former VP of Yili Group, the largest and one of the oldest dairy company in China, and had a high public recognition in social responsibility • Dongxiang’s long-time franchise relationship with Kappa, a popular Japanese brandname • Xu Jiayin, a famous Chinese philanthropist