Download

1 / 34

340 likes | 430 Views

Personal Debt Write-off from an Economic Perspective. Tom McDonnell TASC 19 April 2012. What is TASC?. An independent, progressive think-tank dedicated to promoting equality, democracy and sustainability in Ireland through evidence-based policy recommendations.

E N D

Personal Debt Write-off from an Economic Perspective Tom McDonnell TASC 19 April 2012

What is TASC? • An independent, progressive think-tank dedicated to promoting equality, democracy and sustainability in Ireland through evidence-based policy recommendations.

Part 1Growth Prospects and the Impact of Debt Tom McDonnell TASC 19 April 2012

Outlook for Growth • Debt dynamics are immensely challenging • Growth is the only panacea short of debt restructuring • Growth constraints • Debt overhang (C) • public/commercial/household • Aftershock of banking crisis (I) • lack of lending • Fiscal consolidation (G) • negative multipliers • Weakening exports (NX) • uncertainty and fiscal consolidation in Europe • Celtic Tiger catch-up has played out • Benign conditions will not be replicated

Scale of the Debt Overhang (end 2011) GDP = €156 billion • Government Debt • circa €166-168 billion (105%) • Increasing y-o-y (government balance in deficit) • Will peak • Household Debt • circa €185-190 billion (119%) • Decreasing y-o-y (household deleveraging) • Business Debt • circa €140-150 billion (90-95%) • Decreasing y-o-y (deleveraging/write-downs)

Discretionary Fiscal Tightening, DOF, Nov, 2011 Green = Undertaken,Blue = Planned, Red = Fiscal Compact

Impact of Debt Overhangs • Cecchetti et al (2011) – Empirical analysis of 18 OECD countries • Evidence suggests there is a drag on growth beyond certain thresholds • Government debt - 85% • Household debt – 85% • Corporate debt – 90% • Ireland exceeds all three thresholds

Part 2Housing Aftermath Tom McDonnell TASC 19 April 2012

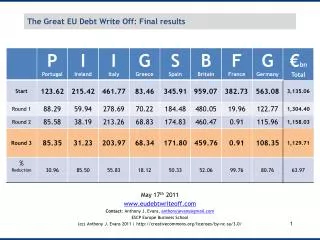

Wealth Destruction Daft Asking Prices (2007 average = 100) • March 2007 = 100.3 • March 2008 = 96.2 (y-o-y decline = 4.1%) • March 2009 = 80.3 (y-o-y decline = 16.5%) • March 2010 = 67.1 (y-o-y decline = 16.4%) • March 2011 = 57.3 (y-o-y decline = 14.6%) • March 2012 = 47.6 (y-o-y decline = 17%) Daft – fall of 53% since peak CSO – fall of 49% since peak National House Price Register to be launched this Year

Falling Prices and Multiple Equilibria • Falling house prices generate a self reinforcing cycle • Falling prices mean declining net worth • Unwise to dismiss negative equity as a problem • A barrier to second hand transactions • Continuous downward cycle of household deleveraging drags on growth • We should be cautious not to distort the market again but market is likely to overshoot downwards in the absence of a positive exogenous shock

Residential Mortgage Arrears (end December 2011) • Total residential mortgage loans outstanding • €113.48 billion • Total mortgage arrears cases outstanding • In arrears 91 to 180 days = €3.27 billion • In arrears over 180 days = €10.67 billion • Value of arrears for the above = €1.12 billion • Restructured mortgages (Balance) • €13.29 billion (of which not in arrears = €6.1 billion) • Approx. 75,000 restructurings so far

Projected losses • BlackRock Stress Case Projected Loss - €10.53 billion • CBI Three-year Projected Loss • €5.92 billion

Ending the Decline Housing market is moribund • Fewer than 4,000 mortgages per quarter • Around 15,000 mortgages for a housing stock of almost 2 million units • No reason to assume market will recover in the foreseeable future Price should reflect underlying value • Prices may have further to fall • Clarity around personal insolvency legislation would help put a stable floor on the market • That in itself will help resuscitate the market • Recovery will only occur when the economy recovers

Part 3Historical Experiences and Policy Options Tom McDonnell TASC 19 April 2012

Historical Experiences Pre Great Recession Crises • USA (1933) • Home Owner Loan Corporation (HOLC) • Mexico (1998) • Punto Final program • Colombia (1999) • Uruguay (2000) • Korea (2002) • Argentina (2002) • Taiwan (2005)

Contemporary Experiences The Great Recession • Iceland (2008) • USA (2009) • Hungary (2011) • Ireland (?)

Policy OptionsDirect Payments to Individuals in Trouble Option 1: Direct Payments to those in trouble (support through the social safety net) • Individuals in trouble will have disproportionately high MPCs MPC = Marginal Propensity to Consume • Virtually all of the disposable income of low income households cycles back into the local economy as consumption • Very high multipliers • If not direct payments? • The Government’s fiscal adjustment should seek to ring fence low income households as much as possible from discretionary adjustments • Taxes/cuts aimed at those on low incomes are more damaging to aggregate demand and therefore have larger impacts to growth and employment

Policy Options Temporary Macroeconomic Stimulus Option 2: Temporary Macroeconomic Policy Stimulus • Government spending targeted at financially constrained households But • No control over monetary policy or exchange rate policy • Limited fiscal space Nevertheless • Policy choices do exist within the envelope of tax and spend • Slightly over half of employment destruction has been in the construction sector

Policy Options Assistance to the Financial Sector Option 3: Assistance to the Financial Sector • Government capitalisation of banks • Government purchase of distressed assets (already happened for commercial loans – NAMA) • Support by the monetary authority is critical • Doesn’t necessarily incentivise the lenders to engage with borrowers But • Can be a complementary policy

Policy Options Support for Household Restructuring Option 4: Setting up Frameworks for Debt Restructuring • Legislation – improving the institutional or legal frameworks • Frameworks for voluntary debt restructuring • Frameworks for ‘automatic’ debt restructuring Other possibilities • Governments buying distressed mortgages from lenders directly or through an intermediary institution • Quid pro quo • Restructuring in exchange for moving trackers to the IBRC

Household Debt Restructuring:International Best Practice • Pitfalls • Incentives • Key principles

Part 4Reasons for Caution? Tom McDonnell TASC 19 April 2012

Burden on Taxpayers? Restructuring involves clear winners • All taxation and public spending choices involve transfers of resources from one section of society to another • Bank bailout was itself a transfer of wealth • Social cohesion cuts both ways Rationale for the taxpayer • High ‘propensity to consume’ of those in trouble • Benefits to the taxpayer in the form of increased aggregate demand, higher growth and employment

Implications for Property Rights? Constitutional issues International reputation • Crucial that there be clearly defined and transparent rules for debt restructuring • What type of system? • Automatic triggering versus case by case discretion • What would the triggers be? • Get it right the first time • Consistency and predictability

Impact on Lending? A genuine dilemma • What can the Government do? • A grand deal involving the EFSF • IBRC as a bad bank • Medium-term support from the Euro system is crucial • What about impact on the future cost of mortgages? • It is entirely appropriate that the cost of future mortgage borrowing accurately reflect the underlying risk • Dangers of cheap credit

Impact on Government Debt Dynamics? • Second bailout is likely in any event • Medium term funding requirements • Irrational not to seek an extension of the current programme • Targeted debt restructuring would help growth dynamics

Part 5A Wider Perspective Tom McDonnell TASC 19 April 2012

A Multidimensional Crisis There is no single silver bullet • Tinbergen • Achieving ‘n’ policy goals require a minimum of ‘n’ policy levers • The interlocking crises of the Euro area

Causes of the Debt crisis • Design flaws • Optimal Currency Area • Asymmetric shocks • Single interest rate – Goldilocks syndrome • Massive credit inflows to the periphery • Current account imbalances • Asset price bubbles • Multiple equilibria • No lender of last resort • No mechanisms, protocols or conditions for writing down debt • No EU-wide special resolution regime for the banking sector • Failure to construct a banking union • No centralised financial regulation

Regulation and Governance in a Monetary Union • Workable monetary union requires centralised oversight and enforcement of financial institutions • Narrow focus on ‘headline’ inflation rate is insufficient • Addition of additional indicators is helpful • Mandate of the ECB is too narrow • Flexibilities required to counterbalance the one-size-fits-all interest rate that creates localised private credit bubbles and amplifies the boom and bust cycle • There are no protocols and conditions for debt write-down and debt restructuring • There are no European wide special resolution mechanisms for insolvent banks

Other IssuesFinancial exclusion • Financial Exclusion • What about the people with no property? • Putting mortgage interest relief into context • ‘Respectable debt’ versus ‘shadow debt’ • Shadow financial sector • Reform is needed

Other IssuesFinancial exclusion – The Trap • Basic bank accounts • Hyperbolic Discounting • Below the radar personal finance • Payday loans • Cheque cashing operations • Buyback shops • Cash for gold etc