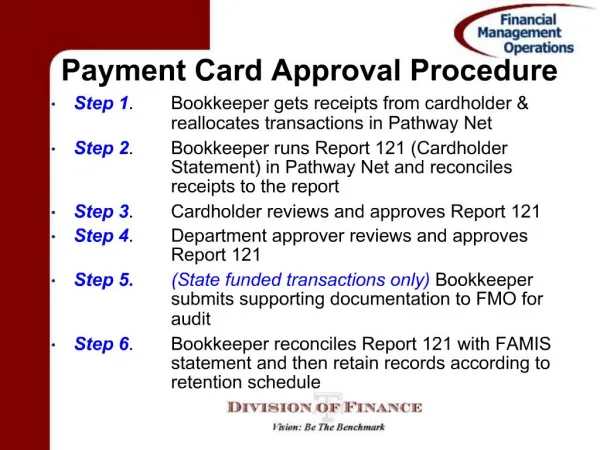

Download

1 / 21

210 likes | 432 Views

Local card infrastructure a new payment paradigm. Leonid Delberg Chairman & CEO Richard Schweger CFO/COO BGS Smartcard Systems New technologies for SME finance The World Bank, Washington D.C. December 4-6 2002. Overview. Company profile Global vs. local DUET concept

E N D

Local card infrastructure a new payment paradigm Leonid Delberg Chairman & CEO Richard Schweger CFO/COO BGS Smartcard Systems New technologies for SME finance The World Bank, Washington D.C. December 4-6 2002

Overview • Company profile • Global vs. local • DUET concept • Delivery channels

Company profile>>>bgs BGS >>> The smart card pioneer, developing smart card solutions since 1991. Headquarters>>> Vienna/Austria. Offices >> >>> Brazil, India, Kazakhstan, Russia, Ukraine Distributors >>> Bosnia-Herzegovina, Egypt, Ecuador, Mexico, Macedonia, Paraguay, GCC, Philippines, Romania, Uruguay, Uzbekistan. Leading supplier of smart card payment systems to the CIS market. 500 installations with 4.500.000 cards issued and 20.000 POS. 55 highly qualified R&D professionals. Expert know-how from 10 years of DUET projects, 50 specialists covering entire project life-cycle.

Company profile>>>Sbercard Issuer Problem Start Date Now Next step Savings Bank of Russian Federation Secure, fast, country-wide money transfer 5 banks, 3.000 cards, 30 POS December 1993 300 banks, 2,3 m cards, 1200 ATM, 11.000 POS Opening acquiring for other Russian banks

Company profile>>>NBU Issuer Problem Start Date Now Next step Uzbekistan National Bank of Foreign Affairs Retail business outside of bank control 1 branch, 5.000 cards, 50 POS terminals April 1995, now 7 other domestic banks 200K cards, 1000 POS, 130 ATMs, National card system, obligatory for all banks

Company profile>>>OAB Issuer Problem Start General Next step Oman Arab Bank Secure, country-wide government payments Q3 2002, 50 000 cards, 300 terminals Strategic goal to offer full payment service handling all government bodies transactions 70.000 cards, Country-wide usage for b2b, b2c

Overview • Company profile • Global vs. local • DUET concept • Delivery channels

Global versus local>>>globalization • The target of Globalization is to gain access to new markets by accepting competition at home • Globalization was initiated by developed countries already having a strong domestic infrastructure base • Equal interest for the further extension of both networks inside and outside of the country • Emerging countries (EC) also have a strong desire to be connected to the global networks • Missing local infrastructure in EC represents a large competitive disadvantage • Risk ! - Development of the global networks in EC will dampen investments in the local infrastructure

Global versus local>>>competition • Competition based on standardized global products ends in favor of large international corporations • The winner often does not ensure the set up of a full coverage infrastructure within the whole territory • Today foreign as well as local issuers invest in credit card deployment instead of developing local mass markets • Development of global card systems by domestic issuers opens the door to local markets for major international competitors • Only innovative & highly localized card products can successfully support domestic issuers

Global versus local>>>card markets • Emerging countries are still cash based economies • Conventional online debit and credit card systems represent solutions for developed markets • There are substantial differences between developed and emerging card markets: • Low household income results in substantial un-banked population • Much higher number of POS are required in emerging countries • Small merchants can’t afford on-line card operation • Missing trust (collateral) to consumer requires card products with no overspending

Overview • Company profile • Global vs. local • DUET concept • Delivery channels

issuer acquirer 400 500 100 merchant card client card DUET concept>>>payment Client account Preathor.funds Transf. funds 400 Merchant account settlement obtain funds deposit funds purchase

Account on-line PIN1 off-line Agent PIN2 PIN-A Merchant off-line PIN2 PIN-M DUET concept>>>client card SCA FSL E-contract

Loyalty Points Area DUET MF-Software Issuer Data, Key, Client PIN 1. Savings book 2. Time deposit ID Data Area 3. Preauthorized debit 4. Bank credit 5. Micro-lending 6. Differed payment 7. Merchant credit 8. Client data VISA VSDC MC M-Chip DUET concept>>>applications Card EMV OS

Overview • Company profile • Global vs. local • DUET concept • Delivery channels

Delivery channels>>>competing cash • As of today cash is the only payment instrument to compete with in all retail mass markets • There many reasons to throw cash out from circulation: • cash is very expensive • cash doesn’t generate interest • cash is slow moving • cash is always anonymous • cash is uncontrollable • There is a sufficient savings potential to finance cash substitution

Delivery channels>>>payments • A standardized global card is the wrong instrument to solve domestic problems in different countries • Creation of separated payment environments is supported by geographically limited area of consumer spending • Consumer interest is of primary importance for local card systems, guaranteeing overall merchant acceptance • Offering cards with credit facilities is the best attraction for any consumer • Targeted spending power can substantially minimize credit risk

Delivery channels>>>money flow Purchase Rent Service Utility Taxes Car Savings Salary Pension Allowance Credit Loan

Delivery channels>>>infrastructure Retail Landlord Service Utility Authority Petrol Finance Enterprise Authority Social Bank Credit

Delivery channels>>>summary • Creation of domestic card infrastructure is an investment process, profits are generated through services offered over such networks • Development of a standardized global system could benefit a competitor’s business • The competition with large international enterprises can only be won by capitalizing on local market know how • Technology can help a local enterprise to differentiate itself through functionality and faster response to market • Proprietary knowledge transformed in innovative solutions is the key for a successful business

Contact • BGS Smartcard Systems AG • Gersthoferstrasse 131; A-1180 Vienna • phone: +43 1 47601 301; fax +43 1 47601 330 • info@bgssmartcard.com - www.bgssmartcard.com