Download

1 / 35

350 likes | 363 Views

HAR-RV with Sector Variance. Sharon Lee March 18, 2009. Intuition. The returns of an individual equity should be correlated with returns from its sector Using the predictive model HAR-RV, how does incorporating sector realized volatility affect the predicted values for an equity?.

E N D

HAR-RV with Sector Variance Sharon Lee March 18, 2009

Intuition • The returns of an individual equity should be correlated with returns from its sector • Using the predictive model HAR-RV, how does incorporating sector realized volatility affect the predicted values for an equity?

Background Mathematics Realized Variance, where rt,j is the log-return Sector Realized Variance: Average of equally-weighted same sector stocks in S&P100

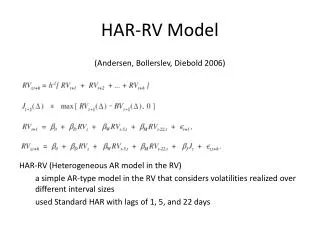

HAR-RV Model • HAR-RV makes use of average realized variance over daily, weekly, and monthly periods. • h=1 corresponds to daily periods, h=5 corresponds to weekly periods, h=22 corresponds to monthly periods • These time horizons correspond to day-ahead, 5-day ahead, and month-ahead predictions of average realized variance.

Sectors • Consumer Goods • Healthcare • Financial • Technology • Stocks with less than 2000 observations were removed

New Questions • Since the R-squared analyses show that sector variance affects individual stocks in different degrees, what can be said about investor behavior for particular sectors across each time horizon? • Do the risk factor (beta) for sectors have any correlation with results?

Next Steps… • Add Basic Materials, Industrial, Services, and Utilities Sectors • Investigate betas