Download

1 / 38

390 likes | 639 Views

Professional Opportunities for CAs in Co-operative and NPO Sectors. By. CA. Charanjot Singh Nanda, Chairman, Committee for Co-operatives and NPO Sectors of The Institute of Chartered Accountants of India. Committee for Co-operatives and NPO Sectors. Significant non-standing Committee

E N D

Professional Opportunities for CAs in Co-operative and NPO Sectors By CA. Charanjot Singh Nanda, Chairman, Committee for Co-operatives and NPO Sectors of The Institute of Chartered Accountants of India

Committee for Co-operatives and NPO Sectors Significant non-standing Committee Constituted during the year 2011-12

Functions To suggest suitable reforms in the statutes regarding Co-operatives and NPOs. To promote uniform accounting framework for Co-operatives and NPOs. To formulate guidelines for statewise auditors empanelment to interact with the concerned authorities. To promote good governance, best practices and prudent financial management in the Co-operatives and NPO sectors/ mutually aided Co-operative Societies [MACS]/ Self help groups/clusters and federations. To promote social audit concept in the NPO and Co-operative Sectors and conduct awareness programmes for the benefit of the stakeholders. To provide technical and governance inputs through training, workshops, resource materials, publications to the management personnel and members of Governance of Co-operatives and NPO Sectors. To constitute an award/recognition for corporate social responsibility initiative by any NPO/Co-operatives/Corporates. To support the initiatives of the State and Central government and corporations in this sector.

Functions cont… To develop necessary technical guides and publications for the benefit of Co-operative banks, Co-thrifts and credit societies and other Co-operatives as a national movement. To develop a knowledge portal providing information regarding subsidies and other support received by the NPOs from the State and the Central Government and to promote various government initiatives to implement social welfare schemes of the NPO Sector and facilitate sharing of knowledge regarding Governance, legal compliance and best practices in financial management. To help the government in monitoring financial discipline in the NPO sector by prescribing transparent guidelines and procedures including documentation and evidence of actual work done and to advise the government on limitations to be imposed on administrative and other expenditures of the NPOs specially those incurred out of government grants. To suggest recommendation on issues related to the Foreign Contributions Regulation Act, 2010, Rules , regulations and guidelines framed thereunder and any other laws affecting this sector with a view to ensure smooth flow of funds on one hand and national security and national interest on the other.

Non-Profit Organizations An Overview

HISTORY In the early 1970s a new breed of organizations emerged called ‘voluntary organizations.’ These organizations were started by people committed to the cause of the poor and the downtrodden. In the late seventies and early eighties, such organisations multiplied and spread all over the country. They started receiving both local and international donations for various programmes and activities.

Developments The non-profit organizations are important for the development of a country as are the for-profit organizations. In India, NPOs operate in varied fields such as health, poverty reduction, education etc. and as active movers in socio- economic change of the country. Of late, these organisations have started utilising the services of various professionals to improve upon the quality as well as impact of the organisations’ works in different areas of activity.

Funding and resources deployed by NPOs Employment of huge financial as well as human resources. Were started and managed mostly by people of goodwill who did not necessarily have professional qualifications or competence. This sector has started utilising the services of experts from diverse professions. This sector offers challenging and rewarding opportunities to accounting professionals in particular. NPOs are increasingly taking the services of accounting professionals for various crucial functions including external auditors, internal auditors and advisors. NPOs have begun to view Chartered Accountants as pathfinders rather than faultfinders.

Sources of funds The main sources of receipts for NPOs in India are mainly from: Self-generated funds, loans, grants and donations funds from the Governments of other countries numerous funding organisations who provide from their own funds funds raised from the public or their respective Governments The Government of India and the State Governments also provide large amounts of funds from the social sector allocation and make it available to the various organisations working in the NPO sector in India.

Financial Management- An Overview Financial accountability, transparency and good governance are the need of the hour in the NPO sector. As the financial and human resources employed in this sector grow year after year, the need for proper financial planning, financial management and financial accountability is also increasing accordingly. Various components of financial management for a non-profit organisation can be explained with the help of the adjoining diagram.

NON-PROFIT ORGANIZATIONS Untapped Area-Full of Professional Opportunities

As Statutory and Internal AuditorsAudit under Incorporation Laws Non Profit Organisations are generally registered as legal entities in the following three categories: Societies under the Societies Registration Act, Central or respective State Acts. Public trusts under the Indian Trust Act 1882. Companies registered under Section 25 of the Companies Act, 1956. Mutually Aided Cooperative Societies Act (MACS) and Self Help Groups (SHGs) Depending upon the law under which it is registered, it has to get its accounts audited as required under the respective laws. Hence, there are plenty of opportunities for auditors to play this role in NPO sector organisations.

Audit under Income-tax Act, 1961 Where the total income of the organisation exceeds the basic exemption limit in any previous year, the accounts of the organisation have to be compulsorily audited as required under section 12A(b) of the Income-tax Act 1961. The auditor has to issue the report in Form 10B, which is mandatory for obtaining exemption under the above Act. The auditor has great opportunities to advise the organisation regarding application of income, accumulation of income, investments of funds, filing application for accumulation and such other requirements to obtain the necessary exemption under the Income-tax Act 1961.

Audit under Foreign Contribution (Regulation) Act, 2010 Every organisation in receipt of foreign contribution must get its accounts audited by a Chartered Accountant under Rule 17(1) of the Foreign Contribution Rules 2010. The Audit Report has to be given in Form FC 6 as prescribed under the above Act together with the Balance Sheet as on 31st March and Receipts and Payments for the year ended 31st March. As there are more than thousands of registered organisations in India, there are plenty of opportunities to audit the accounts of the organisations registered under the above Act. In addition, there are organisations that may have received prior permission, who also have to audit their accounts. In the case of a registered organisation, audit is compulsory even though no funds are received during the year.

Auditors on behalf of donors and funding agencies Donor organisations, both international as well as local, make grants or provide funds and enter into an agreement with the recipient non-profit organisation. In the above agreement various important provisions are made regarding the purpose of the grant, manner in which it should be utilised and the time frame, etc. An auditor has to peruse the above agreement to report on the compliance on the terms of the agreement. Most donors require an audit report and an audited statement of accounts. While certifying the report to donors, the auditor should ensure that the project has been implemented in accordance with the agreement executed.

CAs as reviewers of Financial Management Systems Financial Management in NPO sector organisations has to be of high standards to meet the demands of the various stakeholders. When the NPO receives funds from international agencies, this is even more important as the NPOs financial management has to meet both, national and international standards. Both the international agencies and the NPOs are interested in improving the standards of accounting, financial reporting and legal compliance aspects. The service of a financial expert becomes very useful for studying the ongoing system and recommending improvements. This is yet another area for Chartered Accountants to provide expertise to the NPO Sector.

Advisors on Financial Management and Systems Donor agencies have several requirements in relation to financial accounting and reporting when they provide funds to the NPO. Also, there are many large NPOs who provide funds to other smaller NPOs who are known as partner organisations. In such a situation, the larger NPOs need good and timely advice regarding applicability of tax laws, foreign contribution (regulation) Act, banking etc. For all of the above, NPOs need good advisors on the financial management and legal aspects for themselves, and other organisations dealing with them. Here again, Chartered Accountants have an excellent opportunity to serve NPO sector organisations.

Trainers / Resource Persons in financial management and related aspects The NPO sector attracts many persons for various roles such as staff, management team, board persons and officer-bearers. By and large, they are from diverse fields and not necessarily experts on financial management. Smaller NPOs find it extremely difficult to get qualified persons for accounting and financial management. In the above context, the financial staff of NPO sector organisations need a lot of training on the topics of accounting, reporting and legal compliance aspects. The programme staff also needs some orientation on financial matters as they also deal with funds. Even board members need orientation on financial management so that they can play their role effectively as treasurers or members of Finance Advisory Committee.

Finance Managers and CFOs Large NPOs employ trained and qualified accountants and Finance Managers on a regular basis on attractive pay packages. Chartered Accountants are also doing good work as CFOs and Finance Managers in many medium and large NPOs.

Senior management team members and CEOs Chartered Accountants have moved up to the top management and leadership positions in many companies in the corporate sector. This trend is picking up in NPO sector organisations also as quite a few national and international bodies have selected Chartered Accountants for the top positions in their organisations. Indeed, it is an interesting responsibility to lead a non-profit organisation whose main goal is changing the lives of people especially the downtrodden and the underprivileged in society.

Member or chair of Advisory Bodies As the Boards and Governing Bodies of NPO sector organisations do not always have sufficient time and expertise for financial management and legal compliance; they rely on the advice of sub committees like Finance Advisory Committees. There is a good scope for Chartered Accountants to become members of these Committees and play a useful role.

Members in the Board or Governing Boards As much as corporate governance is critical in the corporate sector, good governance is a critical part of the functioning of NPO sector organisations. There is a great need for financial experts in the Boards, Governing Bodies and Committees of NPO sector organisations. Chartered Accountants can play a vital role in the Governance of the above bodies for promoting good governance and thus increase the performance of these organisations to realise their vision and mission as well as their goals and objectives.

Advocacy/Lobbying for Accounting Standards, Laws etc. The sector faces many challenges due to new laws, rules and regulations; some of which are necessary but some others are neither necessary nor supportive to the well being of the sector. In these circumstances, there is a great need to lobby with the respective authority or the Government Agency to amend the respective legislation or the regulation. This is an area where accounting professionals can play very important roles as no one may be as well placed as the Chartered Accountants.

Accounting Profession- Direct contribution to nation building The NPO sector offers special opportunities especially for smaller firms, individuals and proprietorship firms of Chartered Accountants and for those in the rural areas and small towns too, as there are many NPOs located in the rural areas and smaller towns. Offers excellent methods to fulfil one’s social responsibility by contributing professional expertise to the society especially for the cause of the poor, the needy and the downtrodden.

Co-operative sector AN OVERVIEW

HISTORY The cooperative movement in India owes its origin to agriculture and allied sectors. Towards the end of the 19th century, the problems of rural indebtedness and the consequent conditions of farmers created an environment for the chit funds and cooperative societies. The farmers generally found the cooperative movement an attractive mechanism for pooling their meagre resources for solving common problems relating to credit, supplies of inputs and marketing of agricultural produce.

Legislative History Cooperative Credit Societies Act, 1904 - The First Incorporation As its name suggests, the Cooperative Credit Societies Act was restricted to credit cooperatives. Cooperative Societies Act, 1912 With the developments in terms of growth in the number of cooperatives, far exceeding anticipation, the Cooperative Societies Act of 1912 became a necessity and cooperatives could be organized under this Act for providing non-credit services to their members. With this enactment, in the credit sector, urban cooperative banks converted themselves into Central Cooperative Banks with primary cooperatives and individuals as their members. Multi-Unit Cooperative Societies Act, 1942 With the emergence of cooperatives having a membership from more than one state such as the Central Government sponsored salary earners credit societies, a need was felt for an enabling cooperative law for such multi-unit or multi-state cooperatives. Accordingly, the Multi-Unit Cooperative Societies Act was passed in 1942, which delegated the power of the Central Registrar of Cooperatives to the State Registrars for all practical purposes.

Legislative History cont… NABARD Act, 1981 The National Bank for Agriculture and Rural Development (NABARD) Act was passed in 1981 and NABARD was set up to provide re-finance support to Cooperative Banks and to supplement the resources of Commercial Banks and Regional Rural Banks to enhance credit flow to the agriculture and rural sector. Multi-State Cooperative Societies Act, 1984 With the objective of introducing a comprehensive central legislation to facilitate the organization and functioning of genuine multi-state societies and to bring uniformity in their administration and management, the MSCS Act of 1984 was enacted. Multi-State Cooperative Societies Act, 2002 Unlike the State Laws, which remained as a parallel legislation to co-exist with the earlier laws, the MSCS Act, 2002 replaced the earlier Act of 1984.

Types of Co-operatives Although all types of cooperative societies work on the same principle, they differ with regard to the nature of activities they perform. Followings are different types of co-operative societies that exist in our country. Consumers’ co-operatives Producers’ Co-operative Society Co-operative Marketing Society Co-operative Farming society Housing Co-operatives Agricultural Co-operatives Co-operative banks which may be further sub-classified as: Primary Urban Co-operative Banks. Primary Agricultural Credit Societies. District Central Co-operative Banks. State Co-operative Banks. Land Development Banks.

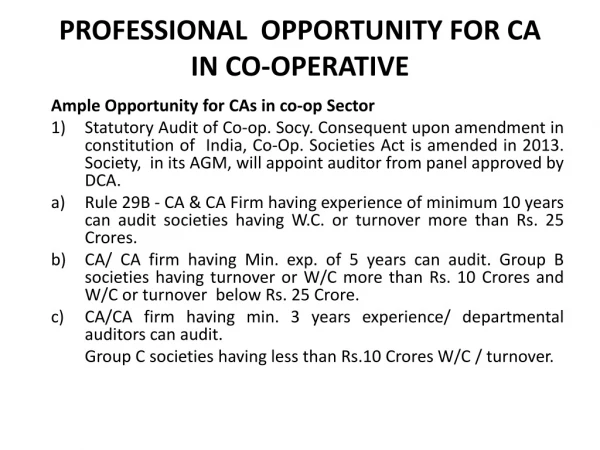

As Statutory and Internal Auditors Various Laws Applicable to Co-op. Credit Societies The Maharashtra Co-op. Societies Act, 1960 (MCS Act) (applicable to any co-operative society registered in Maharashtra and having no branches outside Maharashtra). The Co-operative Societies Act and Rules of the respective state in which the society is registered (Bihar-1935, Orissa-1935, Assam-1950, Karnataka-1959, Madhya Pradesh-1961, Tamil Nadu-1961, Gujarat-1962, Andhra Pradesh-1964, Rajasthan-1965, Kerala-1969, Himachal Pradesh-1971, Delhi-1972, West Bengal-1973). The Co-operative Societies Act, 1912 and Rules (applicable to any state, which does not have its own co-operative law). The Multi-State Co-op. Societies Act, 2002 and Rules (applicable to all societies whose objects are not confined to one state). Depending upon the law under which it is registered, it has to get its accounts audited as required under the respective laws. Hence, there are opportunities for auditors to play this role in Co-operative sector.

Audit of Co-operative Banks Apart from the Statutory Audit, the Reserve Bank of India has mandated co-operative banks to carry out: concurrent audit EDP audit Stock & Book Debt audits are required to be carried out for large borrowers. Hence Chartered Accountants have a professional opportunity in the area of audit of co-operative banks.

Accounting professional Many accounting professionals have already entered the field and are making very good contributions from their expertise in the co-operative sector. Some accounting professionals serve in the co-operative sector as finance managers, finance directors with financial management responsibility.

As advisors in the co-operative sectors Chartered Accountants can offer advisory services in the co-operative sector. They may act as advisors for: Financial Management Legal compliance matters Consultants/Advisors for specific projects

Members in the Board or Governing bodies As much as corporate governance is critical in the corporate sector, good governance is a critical part of the functioning of Co-operative sector as well. There is a great need for financial experts in the Boards, Governing Bodies and various Committees of Co-operative sector. Chartered Accountants can play a vital role in the Governance of the above bodies for promoting good governance and thus increase the performance of these organisations to realise their vision and mission as well as their goals and objectives.

Envisaging future professional opportunities The above are merely some of the roles played by the members in the co-operative and NPO Sectors. But from the emerging scene, it is very clear that more roles are yet to unfold for the Chartered Accountants in these sectors.

The Institute of Chartered Accountants of India Partner in Nation Building Thank You 38