Download

1 / 4

40 likes | 52 Views

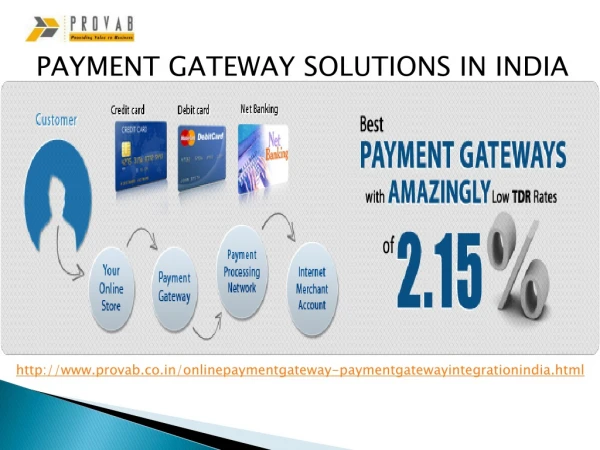

Consumers today prefer digital payments across all touchpoints such as payment counters at retail outlets, petrol pumps, transit modes, e-commerce websites, Kiosks, etc. While digital payments are prevalent in almost every sector, a new wave of digital transformation is likely to be seen in mobility payments.<br>

E N D

Convenience in Mobility Payments | AGS India The Indian payment ecosystem has evolved significantly over the last few years, especially post demonetisation and the pandemic. Consumers today prefer making digital payments across all touchpoints such as payment counters at retail outlets, petrol pumps, transit modes, e-commerce websites, Kiosks etc. While digital payments are prevalent in almost every sector, a new wave of digital transformation is likely to be seen in mobility payments. For decades, cash has been the preferred mode for transit/mobility payments. However, post demonetisation and post-pandemic era, digital modes of payments have witnessed an unprecedented growth. One of the most important reasons for this is consumers’ growing preference towards safe, secure and convenient payments. To cater to this demand, various mobility service providers are collaborating with payment players to offer hassle-free digital payment solutions. Let us understand how convenience in mobility payments is shaping the way for a more seamless transit/mobility payment ecosystem in India: Rise of super apps India has witnessed the proliferation of ‘super apps’ in the last decade. These are all-in-one mobile applications that can be used for ordering food, hailing taxis, online shopping, buying travel tickets like Metro, flights etc., recharging phones and so on. In context of Indian mobility, these applications let you make payments for such services on-the-go by the way of QR codes, UPI etc. This reduces the hassle of navigating

through a zillion applications, thus enhancing overall user-experience and providing added convenience. Fuel payments becoming more ‘swift’ Fuelling is an important part of the mobility ecosystem of our country. Traditionally, fuel Retail Outlets i.e. ROs have been cash intensive. However, post pandemic there is an increased adoption in contactless/digital payments across OMC’s fuel retail outlets. This is evident by the various digital modes of payments such as card payments, UPIQR on PoS or otherwise offered across fuel retail outlets. Various technology solutions such as AGS Transact Technologies’ Integrated Payment Solution or IPS, provides merchants additional control over transactions, greater transparency to end consumers, thus encouraging digital payments via PoS at fuel retail outlets. Growing awareness, the Government of India’s initiatives of incentivising digital payments have encouraged both the consumers & merchants to opt for digital modes of payments, especially at fuel retail outlets. According to an industry survey conducted in 2020, around 90% of the petrol pump customers in Mumbai use wallets and other digital payment modes such as cards witnessed over 50% increase in petrol pumps outside big cities. Digital payments are continuously enhancing customer experience by offering added convenience in the form of reduced time spent at the RO (need for exact change in cash payment is negated), greater transparency in the overall process and hassle-free management of e-receipts and transaction history. Further, the reward/loyalty points earned add to this experience.

As experience & convenience-based offerings gain momentum, many payment players have renewed their value proposition. For instance, AGSTTL through its digital payments brand Ongo, is pilot-testing RFID-based refuelling across a leading OMC’s fuel retail outlets. This solution aims to enhance overall fuelling experience of the by offering ‘convenience’. Introduction of mobility cards or the National Common Mobility Card With interoperability gaining momentum and the GOI’s introduction of National Common Mobility Card (NCMC), India is set to be at par with its counterparts. The National Common Mobility Card, supported by RuPay network enables payments for multi-modal transit in India. This card allows consumers to make payments at RuPay-accepted touchpoints across sectors like the metro, bus, suburban railways, retail, toll, and parking. Such services are expected to boost cross-platform payments in a safe & secure manner. A payment mode such as this improves customer experience and integrates ‘convenience’ deeply in the value chain of mobility payments. Recently, Hon’ble Prime Minister Narendra Modi symbolically inaugurated Bangalore Metro and its Rupay National Common Mobility Card, issued by RBL Bank and powered by AGS Transact Technologies. In addition to Bangalore Metro stations, the NCMC card can also be used at any NCMC enabled metro stations across the country such as Kochi Metro, Delhi Metro and Mumbai Metro. Being an open-loop card, it can be also used to shop and pay for parking. Toll payments going digital

FASTag, the GOI’s product for electronic toll collection in India, speaks volumes about how convenience has found home even in the most traditional payment channels such as toll collection. Based on RFID technology, this tag is affixed on the windscreen of user’s vehicle, and it is scanned the moment passes through the toll gates. This has resulted in reduced wait time at toll plazas and negated the hassle of exchanging exact change, thereby enhancing the overall convenience involved in an individual’s day-to-day commute. These benefits have led to an exponential increase – with the number of transactions using FASTag witnessing a growth of approximately 48% in 2022 as compared to 2021. In addition, FASTag is extended for another crucial component of the mobility ecosystem – parking. Being interoperable, FASTag issued by any member bank is accepted at all NETC enabled parking spaces. This facility eliminates the need for cash transactions, resulting in quicker entry/exit. To conclude, while cash is touted to be the most convenient and thus preferred mode of payment across sectors, the growing need for convenience will be the primary/driving force in mobility payments. This could be achieved by innovation, integration, and collaboration to offer ‘payments-on-the-go’, with the aim to provide a seamless, swifter travelling experience. Hence, in a cut-throat world, what will truly differentiate one offering from the other is the level of convenience that the user will get to enjoy.