Download

1 / 10

100 likes | 208 Views

Coalition for Sustainable Flood Insurance. April 16 , 2014 Coastal Protection and Restoration Authority. CSFI Key Principles. NFIP should: Be long-term sustainable Be actuarially responsible Protect home and business owners who have “played by the rules” Built to code

E N D

Coalition for Sustainable Flood Insurance • April 16, 2014 • Coastal Protection and Restoration Authority

CSFI Key Principles • NFIP should: • Be long-term sustainable • Be actuarially responsible • Protect home and business owners who have “played by the rules” • Built to code • Maintained insurance • Not had repetitive losses • We believe in three key principles about NFIP:

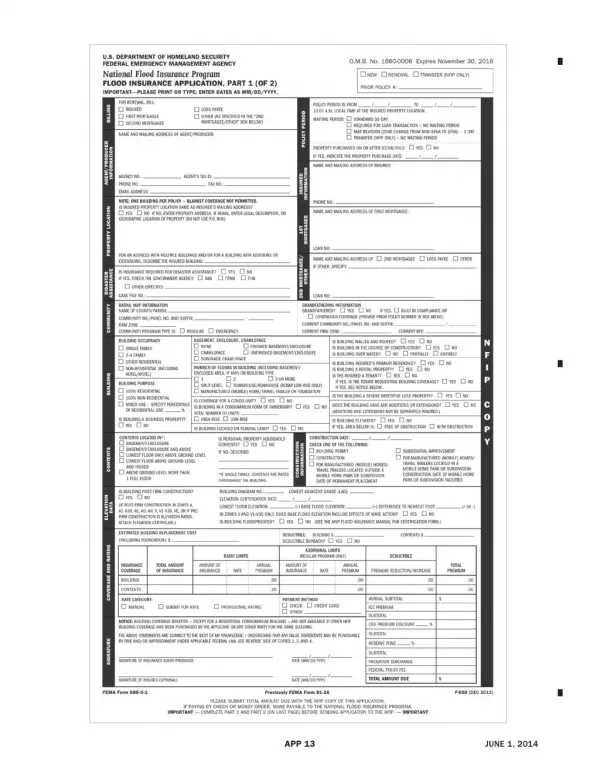

NFIP - Problem • Example: Primary Homeowner May Problem: Premium will go from $633to $17,723 per year. 2013 • Belle Chasse, LA • Built in 1998, fully to code • Built 2’ above FEMA required elevation at the time • House never flooded

NFIP - Problem • Properties become uninsurable • Properties become unsalable • Property values go to zero • Owners lose everything • Banks lose mortgage portfolio • Real estate market freezes • Companies lose workers • Local governments lose tax base • Economies are destroyed • NFIP, itself, goes into “death spiral” as people leave program • If this problem was not addressed, the potential impact could have proved devastating:

CSFI Formation • Building a National Coalition Response: Coalition for Sustainable Flood Insurance May – Dec • GNO, Inc. • Parish Presidents • American Bankers Assoc. • Independent Comm. Bankers Assoc. • Mortgage Bankers Assoc. • Nat’l Assoc. of Counties • Nat’l Assoc. of Home Builders • Nat’l Assoc. of Realtors • 34 states • 200+ organizations from across USA 2013

CSFI GOALS • Educating Congress and Citizens about perilous impacts of Biggert-Waters • Advocating for affordable, sustainable flood insurance • Education and Advocacy

CSFI Results • Passage of H.R. 3370 • Homeowner Flood Insurance Affordability Act March Result: Bipartisan, Bicameral Action for LA and USA 2014 72 votes 22 votes 77% ✔ 77% 306 votes 91 votes ✔

The Homeowner Flood Insurance Affordability Act • Reinstates Grandfathering • Removes the Property Sales Trigger • Requires for FEMA to strive for 1% of policy cost limit (and report) • Caps Annual Premium Increases at 15% • Reimburses Policy Holders for Successful Map Appeals • Refunds Policy Holders w/ Exorbitant Rates • Funds and Mandates Completion of Affordability Study within 2 Years • Allows for $25 Annual Surcharge • Includes Minimum 5% Increase on Pre-FIRM properties • What the Bill Does:

CSFI Next Steps • Formalization into 501(c)(6) w/ National Board and Advisory Council • Continued Dialogue with FEMA and Congress on Implementation • Proposal of Long-Term Options for Affordable Flood Insurance • Ensuring Successful Implementation and Reauthorization

Contact Information • Caitlin Berni • O: 504.527.6980 • C: 985.502.7688cberni@gnoinc.org • Michael Hecht • O: 504.527.6907 • C: 504.715.5037 • mhecht@gnoinc.org On the web csfi.info gnoinc.orgtwitter.com/gnoincfacebook.com/gnoinc • Our address • 365 Canal Street • Suite 2300 • New Orleans, LA 70130 10