Download

1 / 40

1.57k likes | 4.84k Views

Employee State Insurance Act 1948. EFFORTS by : DEPARTMENT OF SOCIALWORK . What is ESI??. Comprehensive Social Security Scheme. Designed to protect employee in organisated sector Components are Sickness Maternity Disablement Death Medical care.

E N D

Employee State Insurance Act 1948 EFFORTS by : DEPARTMENT OF SOCIALWORK

What is ESI?? • Comprehensive Social Security Scheme. • Designed to protect employee in organisated sector • Components are • Sickness • Maternity • Disablement • Death • Medical care

How does the scheme help the employment ?? • Provides full medical care. • Provides financial assistance to compensate loss of wages during absenteeism. • Provide medical care to family members.

Who administered ESI Scheme? • Employee State Corporation • Members are : • Employers • Employee • Central Government • State Government • Medical Profession • Parliament

The Director General is the Chief Executive officer of the corporation

How the Scheme is Funded?? • Self financing scheme • Primarily built our of contribution from employers and employees payable monthly at a fix % of wages paid. • State government also contribute 1/8 the share of the cost of medical benefit.

Who are other bodies?? • At National: • Standing committee [Administrative affairs • Medical Benefit Council Advises • At regional level • Regional boards review and suggestions. • Local committee

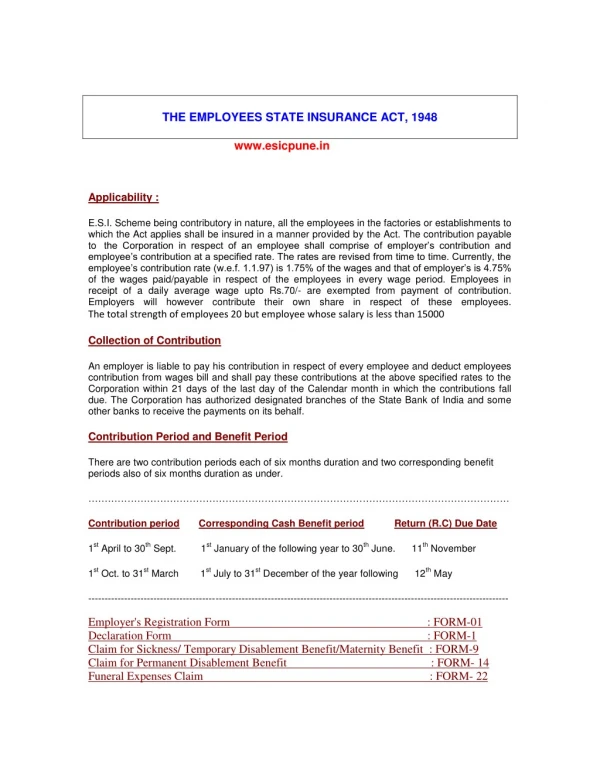

Is it Mandatory for employer to Register under scheme ?? • Yes, statutory responsibility of the employer under sec 2 A , regulation 10 B register their factory establishment under ESI Act within 15 days from the date of its applicability. • FORM – 01

What is Code number in ESI ??? • It is a 17 digit identification number alloted to factory /establishment by the regional officer on receipt of Form 01 or survey report from the social security officer.

Whether person employed are not coverable under the Act?? • All person employed in the premises including the precincts thereof irrespective of their wages including • Casual trainee • Contract employees • Even the directors employed are to be counted

Who are person not to be counted? • A proprietor or partner not to be counted. • A contractor lending the service of his employee. • An apprentice engaged for the first time under the Apprentice Act 1961. • Person employed on contract for service. • Person employed in branch of sales/office away from the factory not come under ceiling.

Establishment that attract coverage under ESI?? • Shops • Hotel or restaurants not having manufacturing activity but engaged in sales. • Cinemas • Road motor transport estb • News paper estb • Private educational institution and Medical institutions.

Is there any provision for exemptin of factory or establishment from ESI Coverage? • Yes if the employee in a factory or establishment are other wise in receipt of benefits substantial similar or superior • The appropriate govt may grant exemption for a period of one year at a time.

Employer??? Principal Employer Immediate Employer One who executes any work inside the premises of the principal employer of f/e One who executes the work of a f/e outside the premises under supervision of principal employer One lets on hire the service of his employee to the principal employer A contractor • Owner • Occupier • Managing agent of occupier • Legal representative • Manager • Specified authority • Head of the dept

Who are the person to be covered as Employees??? • Directly employed by the principal employer. • Employees of the Immediate employer. • Employed in the premises on any work under supervision of principal employer or agent. • Part director of the company • Employees lent or let on hire to the principal employer on any work of the factory

Exclusion : • An apprentice engaged for the first time under the Apprentice Act 1961. • An employee drawing wages above the wage ceiling prescribed by central govt. Wage Ceiling 15000 per month – Regular employee 25000 per month – Disable employee.

Exempted Employee • An employee who is exempted from payment of employees contribution is called an exempted employee. • Rs 100/- w.e.f 2011 • However employers contribution is payable on these wages.

Contribution Rate • Employer contribution:- • A sum equal to 4.75% of the wages payable to an employee. • Employee Contribution • A sum equal to 1.75% of the wages payable to an employee.

What is the Time limit?? • Contribution shall be paid in respect of an employee in to bank duly authorised by corporation within 21 days of the last day of the calender month . • Manner of payment would be • Challan • Demand Draft • Cash • Cheque • Online (Form 5)

Penal Provision – Sec 85 (a) • Period of Delay Rate of Damage • Less than 2 months 5% • 2 to 4 months 10% • 4 to 6 months 15% • 6 months & above 25%

Contribution and Benefits • Contribution period • 1st April to 30th September & 1st October to 31st March of next year. Benefit Period 3 months after the end of relevant contribution period Jan to June and July to December.

Record Maintenance • In addition to Muster Roll, wage record and Book of Account maintained under the laws, • Form 6 Employee Registration in New Form • Form 11 Accident Register • An inspection book • Immediate employer is required to maintain.

What is Registration of IP??? • At the time of joining Declaration Form. • For period of 3 months temporary identification number to employee and his family. • Online Smart card name PEHCHAN CARD separately for self and family with biometric details are issued. • Cash benefits through out the country.

Medical Benefit • It means – medical attendance & treatment to IP and families. • Only benefit provided in kind through state government. • There is no ceiling on expenditure on the treatment of an Insured Person or his family member. Medical care is also provided to retired and permanently disabled insured persons and their spouses on payment of a token annual premium of Rs.120/-

TYPE OF MEDICAL BENEFITS PROVIDED • FULL MEDICAL CARE • EXPANDED MEDICAL CARE • IMMUNIZATION • FAMILY WELFARE SERVICES • SUPPLY OF SPECIAL AIDS

Sickness Benefit • Form of cash compensation at the rate of 70 per cent of wages is payable to insured workers during the periods of certified sickness for a maximum of 91 days in a year • Prescribed certificates are; Forms 8,9,10,11 & ESIC-Med.13.

Qualifying Conditions • To become eligible to Sickness Benefit, an IP should have paid contribution for not less than 78 days during the corresponding contribution period. • A person who has entered into insurable employment for the first time has to wait for nearly 9 months before becoming eligible to sickness benefit, because his corresponding benefit period starts only after that interval.

Sickness Benefit is not payable for the first two days of a spell of sickness except in case of a spell commencing within 15 days of closure of earlier spell for which sickness benefit was last paid. This period of 2 days is called "waiting period". This provision should be clearly understood by IMOs/IMPs as actual experience shows that such of IPs who want to avail medical leave on flimsy grounds generally come for First Certificate/First & Final Certificate within 15 days of earlier spell, usually on unpaid holidays and/or on each weekly off etc, to avoid loss of benefit for 2 days due to fresh waiting period.

Extended Sickness benefit (Sec 99) : Extendable upto two years in the case of 34 malignant and long-term diseases at an enhanced rate of 80 per cent of wages. • An insured person who has completed 2 years of insurable employment and contributed not less than 156 days during this period entitled to get these benefits for period of 309 days – 34 diseases.

Extended upto 730 days or till the insured person attains the age of 60 year whichever is earlier. • Family is also entitled to get medical benefit during this period.

Enhanced sickness benefit. • Promote small family norm • Cash benefit for undergoing tubectomy & vasectomy • 7 days for vasectomy operation • 14 days for tubectomy operation • Post operative complication – period can be extended.

Maternity Benefit • Maternity Benefit for confinement/pregnancy is payable for three months,. • Which is extendable by further one month on medical advice at the rate of full wage subject to contribution for 70 days in the preceding yr

Maternity Benefit is payable to an Insured Woman in the following cases subject to contributory conditions: • Confinement-payable for a period of 12 weeks (84 days) on production of Form 21 and 23. • Miscarriage or Medical Termination of Pregnancy (MTP)-payable for 6 weeks (42 days) from the date following miscarriage-on the basis of Form 20 and 23. • Sickness arising out of Pregnancy, Confinement, Premature birth-payable for a period not exceeding one month-on the basis of Forms 8, 10 and 9. • In the event of the death of the Insured Woman during confinement leaving behind a child, Maternity Benefit is payable to her nominee on production of Form 24 (B). • Maternity benefit rate is 100% of average daily wages.

Disablement Benefit • Temporary disablement benefit : From day one of entering insurable employment & irrespective of having paid any contribution in case of employment injury. Temporary Disablement Benefit at the rate of 90% of wage is payable so long as disability continues. • Permanent disablement benefit : The benefit is paid at the rate of 90% of wage in the form of monthly payment depending upon the extent of loss of earning capacity as certified by a Medical Board

Dependent Benefit (DB) • DB paid at the rate of 90% of wage in the form of monthly payment to the dependants of a deceased Insured person in cases where death occurs due to employment injury or occupational hazards.

Other expenses • Funeral Expenses : An amount of Rs.10,000/- is payable to the dependents or to the person who performs last rites from day one of entering insurable employment. • Confinement Expenses : An Insured Women or an I.P.in respect of his wife in case confinement occurs at a place where necessary medical facilities under ESI Scheme are not available. 2500 per confinement

In addition, the scheme also provides some other need based benefits to insured workers.

Vocational Rehabilitation :To permanently disabled Insured Person for undergoing VR Training at VRS. • Physical Rehabilitation : In case of physical disablement due to employment injury. • Old Age Medical Care :For Insured Person retiring on attaining the age of superannuation or under VRS/ERS and person having to leave service due to permanent disability insured person & spouse on payment of Rs. 120/- per annum.

Rajiv Gandhi ShramikKalyanYojana • This scheme of Unemployment allowance was introduced w.e.f. 01-04-2005. An Insured Person who become unemployed after being insured three or more years, due to closure of factory/establishment, retrenchment or permanent invalidity are entitled to :- Unemployment Allowance equal to 50% of wage for a maximum period of upto one year. • Medical care for self and family from ESI Hospitals/Dispensaries during the period IP receives unemployment allowance. • Vocational Training provided for upgrading skills - Expenditure on fee/travelling allowance borne by ESIC.

Incentive to employers in the Private Sector for providing regular employment to the persons with disability : Minimum wage limit for Physically Disabled Persons for availing ESIC Benefits is 25,000/-. • Employers' contribution is paid by the Central Government for 3 years.