Download

1 / 29

310 likes | 709 Views

Feasibility of the Fama and French three factor model in explaining returns on the JSE . by Patrick Basiewicz and Christo Auret Paper read at the 18 th Annual SAFA Conference Cape Town 14 January 2009 University of the Witwatersrand. Contents. Introduction

E N D

Feasibility of the Fama and French three factor model in explaining returns on the JSE. by Patrick Basiewicz and Christo Auret Paper read at the 18th Annual SAFA Conference Cape Town 14 January 2009 University of the Witwatersrand

Contents • Introduction • Dataset & Portfolios Construction • Time Series Tests • Tests on Ungrouped Data • Endogeneity • Conclusions

Contents Introduction Dataset & Portfolios Construction Time Series Tests Tests on Ungrouped Data Endogeneity Conclusions

EMPIRICAL SUCCESS THEORETICAL UNDERPINNING Very Poor Strong Consumption CAPM CAPM “Statistical” APT “Macro” APT Fama-French 3 Factor Model Very Strong Very Weak Introduction Until recently, the state of asset pricing theory was uninspiring • Theoretically pure models, such as the Consumption CAPM of … have met with very poor ability to explain divergence in realized returns • CAPM’s ability to explain returns has been, mostly, weak. • Various APT models generally fail to account for the market anomalies such as the size effect, value effect, momentum effect… • The Fama and French three factor model has been largely successful in explaining the cross-section of realized returns. • Only within the last few years evidence and theory linking the Fama and French three model to plausible sources or risk has emerged.

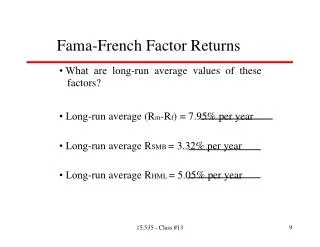

The Model (Fama & French, 1993) The Three Premia • Algebraically: • More Common (empirical) specification: Excess return of the Market Zero cost portfolio that captures excess return of value stocks over growth stocks Zero cost portfolio that captures excess return of small stocks over large stocks

Our Aim: To Build and Test the Fama and French three factor Model in the South African Market • We begin with a “base-case” where we test the CAPM and the APT model proposed by van Rensburg and Slaney (1997) • In addition to the “traditional” three factor model we test a variant that incorporates the market dichotomy of the JSE proposed by van Rensburg (2005) • We perform time-series tests on grouped data using robust statistical methods • We assess its ability to price-out the size and value effect Versions of the three factor model have been constructed with South African data before (van Rensburg and Robertson (2004), Scher and Muller (2005)), but these studies have abstracted from formal tests of the model

Contents Introduction Dataset & Portfolios Construction Time Series Tests Tests on Ungrouped Data Endogeneity Conclusions

Dataset • The sample period spans from June 1992 to July 2005, yielding 156 monthly time-seriesobservations. • The raw number of firm-month observations - where all variables are available for a given firm at a given point in time - is about 76600. • But, when we use apply our stringent data restrictions we are left with circa 45000 firm-month observations from 893 usable companies. • Data Sources • Buro of Financial Analysis/McGregor’s database (BFA) • I-Net Bridge (I-Net) • Bloomberg Professional Service (Bloomberg) • McGregor’s Who Owns Whom Manuals (McGregor’s Manuals) • JSE Monthly Bulletin (JSE bulletin) For detailed discussion look to Basiewicz and Auret (2009) or contact the authors

Test Assets • Statistical considerations require the test assets to exhibit wide dispersion in mean returns and factor loadings (inter alia Chen, Chen and Hiseh, 1986 & Cochrane 2000). • We from 12 test assets by intersecting • four market capitalisation sorted portfolios • three book-to-market ratio sorted portfolios • This closely follows Fama and French (1993, 1995) • We use book-to-market as the value-growth indicator, as Basiewicz and Auret (2009) show that it has strongest power to forecast returns • Thus we will expect wide dispersion of loadings on the size and the value factor and, given the size and persistence of the size and value effects, large disparity in returns as well.

Factor Construction Step 1: Each June in the sample period we find 200 most liquid companies (Use of 200 most liquid stocks stops small, economically unimportant, stocks from dominating the breakpoints) Step 2: We find the size breakpoint by obtaining the median market capitalisation of this sample Step 3: We find two book to market breakpoints which split the sample into 30% of high book-to-market stocks, 30% of low book-to- market stocks and 40% neutral stocks Step 4: We perform an intersection of the two sorts Step 5: We assign every stock in the data set that is listed in the given June and meets our liquidity and price criteria into one of the six portfolios Step 6: Calculate each portfolio's return for 12 months. All returns in the portfolios are value weighted

Large firms LV LN LG SV Small firms SN SG Value firms Neutral firms Growth firms Factor Construction The Size Factor: Small Minus Large (SML) = (SV+SN+SG)/3 - (LV+LN+LG)/3 The Value Factor: Value Minus Growth (VMG) = (SV+LV)/2 - (SG+LG)/2 The Market factor is the portfolio of all shares in the database The Findi factor is a portfolio of all financial and industrial shares The Resi factor is a portfolio of all resource shares

Contents Introduction Dataset & Portfolios Construction Time Series Tests Tests on Ungrouped Data Endogeneity Conclusions

Time-series vs. Cross-section • To test: • Find portfolio which mimics factor X • Regress returns of all assets i on the factor. • Test if all α’s (intercepts) are simultaneously zero. Benefit: circumvents error-in- variables problem Cost: assumes that time- series estimates of α are unbiased and factor mimicking portfolio exists Cross-section Time-series • Calculate bi for all assets i via time-series regression • Regress the bi’s on mean returns of all assets i. • Test if all α’s (residuals) are simultaneously zero. • Benefit: no assumptions are made regarding the f actor or α • Cost: relies on noisy estimates of bi’s • requires large cross- section assets

Methodology Primer • We perform all of the time-series regressions in one step, by mapping the 12 regression SURE system into a GMM framework • The CAPM (CAPM) • The APT of van Rensburg and Slaney (1997) (RS-APT) • The Fama and French (1993) three factor model (FF3F) • The Fama and French (1993) three factor model adjusted for dichotomy of the JSE (RS-FF3F) • We test on two sets of assets: value-weighted and equal-weighted. • Use of GMM ensures that all the standard errors corrected for heteroskedasticity and autocorrelation. • In all regressions we include lagged terms of the Market, Resi and Findi factors to account for thin trading • We use the F-distributed GRS test to test for overall significance of the model • We use linear combination of the intercepts of all the test assets to ascertain the size and value effects left over after risk adjustment.

GRS test rejects both models “Traditional” Models: The base case CAPM We emphasize the importance of including the lagged term in the regressions • In CAPM tests the lag on the Market factor is significant in 21 (of 24) retrogressions • In RS-APT tests the lag on the Findi factor is significant in 18 (of 24) retrogressions • In both cases the size of the lagged term is inversely related to firm size RS-APT The size effect is persistent and large, the value effect is persist in equal-weighted assets

Large Large Small Small Value Value Growth Growth The FF3F: the size factor • All but three loadings on the size are different from zero • In all most cases the t-statistics yield very small p-values • Most of the loadings are positive. This is expected due to skewness in the distribution of market capitalizations on the JSE Value weighted Equal weighted We interpret these results as evidence of a shared covariance - a source of risk – of small firms. FIX significant at 10% level, ** significant at 5% level, *** significant at 1% level t-statistics in parenthesis Results of RS-FF3F are very similar

Large Large Small Small Value Value Growth Growth The FF3F: the value factor • Less robust than the size factor • About half of assets load significantly on the value factor; not all firms need to be value or growth • Assets that do load, do so at high levels of statistical significance • Few assets load negatively on the value factor: • Could it be a consequence of there being few truly growth firms listed on the JSE? Value weighted Equal weighted We interpret these results as evidence of a shared covariance - a source of risk – of value firms. significant at 10% level, ** significant at 5% level, *** significant at 1% level t-statistics in parenthesis Results of RS-FF3F are very similar

The three factor models GRS test does not reject both models FF3F The three factor also fails to completely account for the size and the value effects. The magnitude of the effects is smaller. The R2’sare larger when compared with the base case RS-FF3F The lagged terms on the Market and Findi factors are no longer significant in the three factor specifications Do the FF3F factors partially reflect risk associated with thin trading?

Contents Introduction Dataset & Portfolios Construction Time Series Tests Tests on Ungrouped Data Endogeneity Conclusions

Rationale Cochrane (2001), among many others, notes that a correctly specified asset pricing model needs to explain all predictable variations in asset returns We use their approachadvocated by Brennan, Chordia and Subrahmanyam (1998) and van Rensburg and Robertson (2003a). Evaluation of an asset pricing model requires a test that will show its ability to price out the predictive power of assets’ characteristics Do stock characteristics that have predictive power of stock returns (e.g. firm size or BE/ME ratio) retain their ability to forecast returns? Yes No Irrationality is present in the market, model is misspecified, microstructure effects persist Model is correctly specified

Methodology Primer • Step 1: For each firm in the sample we regress its returns onto candidate model’s factors. We use full listing period. • Step 2: We calculate firm-month pricing errors with • Step 3: Each month in the sample period we regress the lead of the pricing errors on firm characteristics such as market capitalisation and the book-to-market ratio. We apply liquidity and price restrictions on this sample. Result is a time-series of coefficients. An average of those would yield the standard Fama-McBeth estimator. • Step 4: In order to ensure that the coefficients are i.i.d we adjust the coefficients by regressing them onto the pricing factors and use Newey-West (1987) to adjust for autocorrelation. The intercept is the coefficient of interest Firm-month pricing error

Tests on Ungrouped Data CAPM RS-APT After risk adjustment with the CAPM and the APT, the size and the value effect clearly persists FF3F RS-FF3F The risk adjustment with the FF3F and the RS-FF3F explains much of the value effect and goes in the right direction to explain the size effect.

Contents Introduction Dataset & Portfolios Construction Time Series Tests Tests on Ungrouped Data Endogeneity Conclusions

Endogeneity • We do recognise the argument that results which show that a set of factors constructed in a similar manner to the test assets should be able to price these assets easy • We do recognise the some of the loadings on the VMG and the SML may be biased do to this problem of endogeneity • However, we believe that our results show valid evidence of shared variance of small firm and shared variance in value firms • … and that endogeneity is not the sole reason for the model’s successes • We see a robust test of the endogeneity as a direction for future papers

Large Large Large Large Small Small Small Small Value Value Value Value Growth Growth Growth Growth Endogeneity (cont…) 1. Assets that are not used as building blocks of the three factors Loadings on VMG (Value-weighted) Loadings on VMG (Equal-weighted) Since the VMG factor does not include neutral firms, these firms were not included in the factor, but load significantly onto the factor 2. Assets with low weight in the factors yield highest loadings Loadings on SML (Value-weighted) Loadings on SML (Equal-weighted) Since the SML is value weighted, the smallest firms receive very low weights in the factors but exhibit very high loadings on the SML.

Large Small Value Growth Endogeneity (cont…) 3. Some firms load on the positively on the size factor, but are more likely included in the “Large” part of the SML Loadings on SML (Equal-weighted) The relatively smaller firms in these (equally-weighted) portfolios receive a relatively large weight, but would receive relatively low weight in (value-weighted) “Large” part of the SML. But, these relatively smaller firms “behave” like the small firms thus they load positively on the SML, but are likely to be included “Large” part of the SML 4. A test on a alternative set of test assets confirms our results • Friedman (2006) (a WBS MBA dissertation) uses our three factor model to adjust for risk a portfolio of right issuing firms. He finds: • Statistically significant loadings on the SML and VMG • Higher R2 when compared with the CAPM • Pricing errors closer to zero

Contents Introduction Dataset & Portfolios Construction Time Series Tests Tests on Ungrouped Data Endogeneity Conclusions

Conclusions • We constructed and tested the three factor model of Fama and French (1993) • Tests have provided support for these models for returns on the JSE. • The GRS tests have not rejected the model. • Many assets exhibit significant, in both economic and statistics sense, loadings on the SML and the VMG factors • We interpret these findings as evidence of shared covariance of small firms and shared covariance of value firms • In tests on grouped and ungrouped data, the value effect is mostly explained by the three factor model, but the size effect persist