Download

1 / 8

80 likes | 95 Views

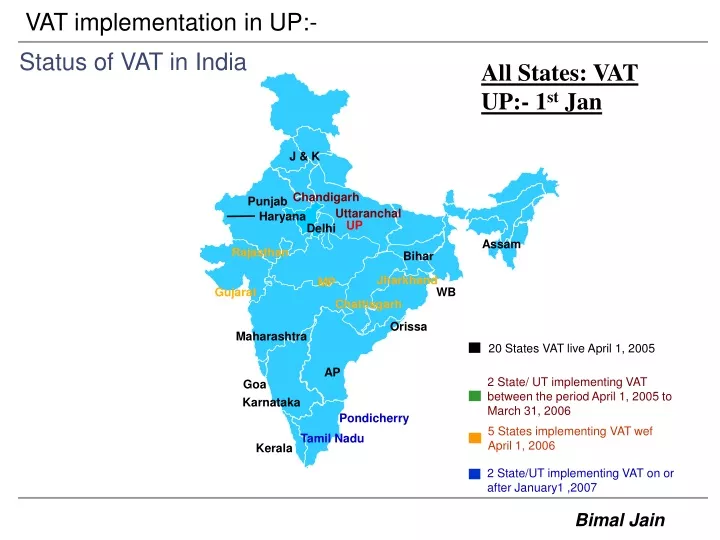

20 States VAT live April 1, 2005. 2 State/ UT implementing VAT between the period April 1, 2005 to March 31, 2006. VAT implementation in UP:-. Status of VAT in India. All States: VAT UP:- 1 st Jan. J & K. Chandigarh. Punjab. Uttaranchal. Haryana. UP. Delhi. Assam. Rajasthan. Bihar.

E N D

20 States VAT live April 1, 2005 2 State/ UT implementing VAT between the period April 1, 2005 to March 31, 2006 VAT implementation in UP:- Status of VAT in India All States: VAT UP:- 1st Jan J & K Chandigarh Punjab Uttaranchal Haryana UP Delhi Assam Rajasthan Bihar Jharkhand MP Gujarat WB Chattisgarh Orissa Maharashtra AP Goa Karnataka Pondicherry 5 States implementing VAT wef April 1, 2006 Tamil Nadu Kerala 2 State/UT implementing VAT on or after January1 ,2007

VAT implementation in UP:- • Value Added Tax (VAT) is a multistage tax, levied on value added at different stages of production and distribution of a commodity or the supply of a service • Registration • Threshold limit Rs 5 lacs. • Auto Registration for Reg Dealer – Form VII & VIII within 60 days. • Compulsory for Transporters, Carriers, Forwarding Agents, Railway Agents etc – transporting/storing goods. • Tax Payer’s Identification No (TIN):- Allotted on Form no.15 –Mandatory to quote on all Correspondences /Return/ Challan/ Tax invoice etc. • Composition Scheme:-Specified for Small Traders -5 to 50 Lakhs @ VAT 1%. • VAT Rates • Four rates have been prescribed • Schedule: I - 0% for exempted goods. • Schedule: II - 4%: for manufacturing inputs & IT Products & GSM. • Schedule: III -1%: for gold and precious stone. • Schedule: IV – 20% to 32.5% for Petrol, Diesel oil, Furnace Oil. • Schedule: V RNR - 12.5%: for goods not specified under any schedule.

VAT implementation in UP:- • Input Tax Credits:- ITC • Allowed For intra-State purchase of goods for resale or use in manufacture. • Not allowed in respect of Non-VAT goods, captive power plant and other specified capital goods like office equipment, furniture, air conditioners etc. • Input tax credits are not available for inter State (CST) procurement of goods. • Stock transfers outside the State attract a reversal of input tax credit (ITC) to the extent of 3%. • Developers, co-developers and units in SEZ eligible for ITC on taxable goods for • specified operations. • Specified goods to be notified under Schedule IV to be taxable at first point. • Provisional refund of ITC to exporters. • Refund of excess ITC to other dealers at the end of the assessment year next to the assessment year in which it falls due. • ITC on capital goods (other than non creditable capital goods): “Capital Goods” means plant, machine, machinery, equipment, apparatus, tools appliances, electrical installation used for manufacture or processing of any goods for sale by the dealer and includes components, spare parts, accessories, mould dies etc. • ITC on capital goods - in 3 annual installments. • No ITC on capital goods held in stock as on the date of commencement of the Act.

VAT implementation in UP:- • ITC on Opening Stock:- • RM & Semi FG & FG ->Available for immediately preceding 6 Months from the date of Commencement of VAT i.e July to Dec,07. ( except exempted goods &CG ) -> Intimation with in 30 days in Sp. Format to Deptt. • Utilization:- 6 Monthly/Qtrly Installments after expiry of 4 months from 1st Jan. • Other Features of VAT in UP:- • Exports are zero rated and hence eligible for input tax relief/refunds. • Other taxes such as turnover tax, surcharge, additional surcharge, special additional taxes etc. prevailing under the sales tax regime have been abolished. • Entry taxes continue for specific products (diesel, petrol etc) but have been made vatable. • No Departmental assessments - Self assessment of tax. • Purchase Tax • Leviable on purchase of goods from un-registered dealers. • Payable when such goods / goods manufactured from VAT inputs are disposed off otherwise than by way of sale

VAT implementation in UP:- • Return & Payment of Taxes:- • Works Contract:- where a contractor does not maintain separate book of accounts, a • fixed deduction of 20% on account of labour and service charges will be allowed • irrespective of the nature of works contract. • Check Posts:- Withdrawn but Mobile Squad will continue • Form no.31 ( Required for movements of goods from Any States -Continue • (New From no.XXXVIII). • 2. Form no.49 (Required for movements of imported goods) Continue (new Form • no.XXI) – Disputed. • 3. OC Stamps Withdrawn.

VAT implementation in UP:- • TAX INVOICE:- • Prepared in Triplicate -> Separate tax invoice -> Performa is not yet prescribed. • Suggested size of invoices not less than 10”x8.5” but not greater than 11”x8.5” on paper of good quality. • Include information and details about Consecutive serial no, date, Name & address of purchaser, seller, TIN, description of goods – Qty, Value, Discounts, Rate of Tax etc. • Invoice shall be accompanied by transporter memo / LR copy. • Every invoice should be pre-authenticated by Authorized person – Excise/Sales tax. • Separate Serial no for LST & CST sale. • Invoice book binding from Sr.no.1 to 50 & followed.

VAT implementation in UP:- • Negatives of UP VAT:- • Conversion of Sales tax exemption in to Deferment. • VAT ITC on exempted FG – Not available to Dealer but available for Taxable goods (CBU) – for 6 Months.(UP Mfg goods -Stock) • No ITC on CG on Transition date & used in Works Contract. • Tax Invoice as per Specified Format & Pre Authenticated by Approved Person. • Continuation of Form No.31 & Mobile Squad. • Excess VAT ITC refund after completion of P.Y. • Continuation of Entry Tax though Vatable.

VAT implementation in UP:- Thanks