Download

1 / 9

90 likes | 108 Views

Explore various investment strategies to optimize returns, considering reinvestment rates and payment timings. Learn how to calculate fund amounts and yield rates effectively.

E N D

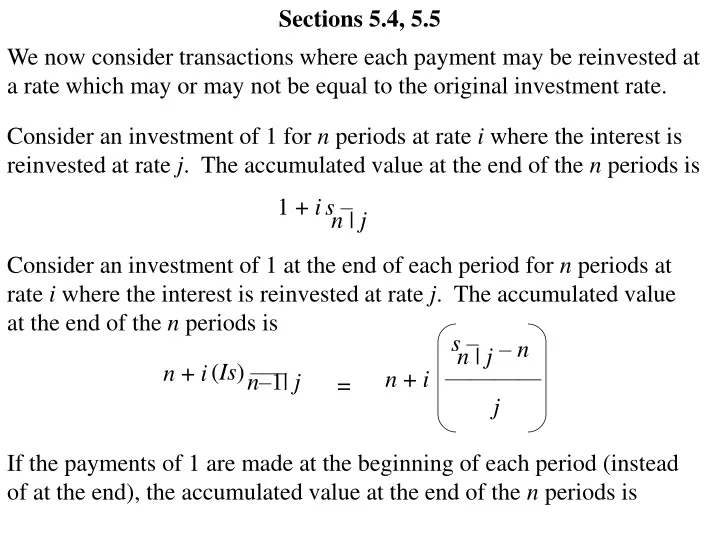

Sections 5.4, 5.5 We now consider transactions where each payment may be reinvested at a rate which may or may not be equal to the original investment rate. Consider an investment of 1 for n periods at rate i where the interest is reinvested at rate j. The accumulated value at the end of the n periods is 1 + i s– n | j Consider an investment of 1 at the end of each period for n periods at rate i where the interest is reinvested at rate j. The accumulated value at the end of the n periods is s– n | j – n ———— j (Is) ––– n–1| j n + i n + i = If the payments of 1 are made at the beginning of each period (instead of at the end), the accumulated value at the end of the n periods is

s––– n+1| j – (n + 1) ——————— j (Is) – n| j n + i = n + i Payments of $1000 are invested at the end of each year for 10 years. The payments earn interest at 7% effective, and the interest is reinvested at 5% effective. Find the (a) amount in the fund at the end of 10 years, (b) purchase price an investor must pay for a yield rate of 8% effective. – 10 —————— = 0.05 s –– 10 | 0.05 1000 10 + 0.07 12.5779 – 10 —————— = 0.05 1000 10 + 0.07 $13,609.06 $13,609.06(1.08)–10 = $6303.63

Three loan repayment plans are described for a $3000 loan over a 6-year period with an effective rate of interest of 7.5%. If the repayments to the lender can be reinvested at an effective rate of 6%, find the yield rates. (Total interest paid with each plan was found in a previous example.) (a) (b) The entire loan plus accumulated interest is paid in one lump sum at the end of 6 years. This lump sum is 3000(1.075)6 = $4629.90. Since there is no repayment to reinvest during the 6-year period, the yield rate is obviously 7.5%. Interest is paid each at the end of each year as accrued, and the principal is repaid at the end of 6 years. Each year during the 6-year period, the payment is 3000(0.075) = $225. The accumulated value of all payments at the end of the 6-year period is 3000 + 225 = 3000 + 225(6.9753) = $4569.44. s – 6 | 0.06 To find the yield rate, we solve 3000(1 + i)6 = 4569.44. The yield rate is 0.07265 = 7.265%.

(c) The loan is repaid with level payments at the end of each year over the 6-year period. Each year during the 6-year period, the payment is R where . 3000 = R R = $639.13 a –– 6 | 0.075 The accumulated value of all payments at the end of the 6-year period is 639.13 = s – 6 | 0.06 639.13(6.9753) = $4458.12. To find the yield rate, we solve 3000(1 + i)6 = 4458.12. The yield rate is 0.06825 = 6.825%.

In practice, it is common for a fund to be incremented with new principal deposits, decremented with principal withdrawals, and incremented with interest earnings many times throughout a period. Since these occurrences are often at irregular intervals, we devise notation for the purpose of obtaining an effective rate of interest: A = B = I = Ct = C = aib = the amount in the fund at the beginning of the period the amount in the fund at the end of the period the amount of interest earned during the period the net amount of principal (positive or negative) contributed at time t, where 0 t 1 t = total net amount of principal contributed during the period Ct the amount of interest earned by investing 1 from time b to time b + a, where a 0, b 0 , and b + a 1

Observe that we must have B = A + C + I. Understanding that I is received at the end of the period (consistent with the definition of effective rate of interest), we have t I = iA + Ct1 – t it With compound interest, 1 – t it = (1 + i)1–t– 1. t We then have I = iA + Ct [(1 + i)1–t– 1] which can be solved for i by iteration, and i is guaranteed to be unique as long as the balance never becomes negative (from previous results). Alternatively, an approximate value for i can be obtained by using the “simple interest” approximation 1 – t it (1 –t)i . This approximate solution is i (This approximation is very good as long as the Cts are small in relation to A.) I ———————— t A + Ct(1 –t) This denominator is often called the exposure associated withi.

One useful special case is when we might assume that net principal contributions occur at time t = 1/2, in which case we have i I ———— = A + 0.5C I ——————— = A + 0.5(B – A – I) 2I ———— A + B – I I ———————— = t A + Ct(1 –t) If we assume that net principal contributions occur at time t= k (where of course 0 < k < 1), then i I ————— = A + (1 – k)C I ————————— = A + (1 – k)(B – A – I) I ———————— = t A + Ct(1 –t) I —————————— kA + (1 – k)B – (1 – k)I Consider again the “simple interest” approximation 1 – t it (1 –t)i on which these approximate formulas are based. (Observe that t is not playing the same role that it plays when defining the accumulation function a(t) = 1 + ti for simple interest.) Let us consider writing an expression for t i0 when we assume 1 – t it= (1 –t)i .

If 1 is invested for one period, then 1 + i is the value of the investment at the end of the period. This investment should yield the same amount as first investing 1 from time 0 to time t, and then investing the amount from the first investment from time t to time 1. Under the assumption that 1 – t it= (1 –t)i , we can write 1 + t i0 + (1 + t i0) 1 – t it = 1 + i 1 + t i0 + (1 + t i0)(1 –t)i = 1 + i Solving for t i0 is what you need to do in Exercise 5-17(a). Formulas (5.18), (5.19), and (5.20) in the textbook assume payments and contributions are made continuously (but this situation does not often occur in practice).

At the beginning of a year, an investment fund was established with an initial deposit of $3000. At the end of six months, a new deposit of $1500 was made. Withdrawals of $500 and $800 were made at the end of four months and eight months respectively. The amount in the fund at the end of the year is $3876. Using the formula which results from the approximation 1 – t it (1 –t)i , find the approximate effective rate of interest earned by the fund during the year. First, we find I = B– A – C = 3876 – 3000 – (1500 – 500 – 800) = 676 I i ———————— = t A + Ct(1 –t) 676 ———————————————————————— = 3000 + (–500)(1 – 1/3) + (1500)(1 – 1/2) + (–800)(1 – 2/3) 676 —— = 3150 0.2146 or 21.46% Look at Example 5.8 on page 144 in the textbook.