Download

1 / 18

180 likes | 233 Views

Learn the relationship between property and financial claims, the concept of equities in accounting, and how transactions impact the accounting equation. Explore examples and scenarios to grasp the fundamentals of financial accounting.

E N D

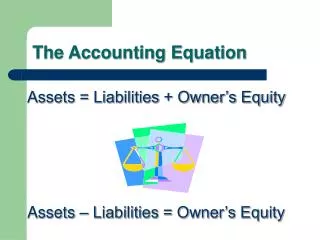

Chapter 3Business Transactions and the Accounting Equation Objectives: • Describe the relationship between property and financial claims. • Explain the meaning of the term equities as it is used in accounting. • List and define each part of the accounting equation.

Objective cont . . . • Demonstrate the effects of transactions on the accounting equation. • Check the balance of the accounting equation after a business transaction has been analyzed and recorded. • Define the accounting terms introduced in this chapter.

HARPO PRODUCTIONS, Inc. First African-American woman to become a billionaire 1986 – She created Harpo Production, Inc. Talk show generates $104 million per year. “O” Talk show videos books movies

Chapter 3 Worksheets Section 2 Transactions That Affect Owner’s Investment, Cash, and Credit

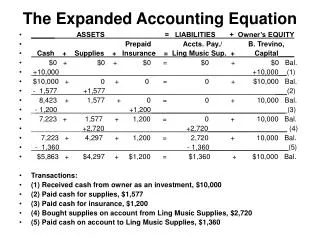

Problem 3-1 Balancing the Accounting Equation (T-page 53) $10,000 $26,000 $ 3,000 $ 26,000 $ 6,000 $13,000 $16,000 $ 8,000 $21,000 $ 20,000 $35,000 $ 4,500

Problem 3-2Determining the Effects of Transactionson the Accounting Equation (T- page 59)

Problem 3-2 Transaction #1: Jan Swift , owner, deposited $30,000 in the business checking account. +30,000 +30,000 +700 +700 #2: The owner transferred to the business a desk and chair valued at $700.

#3: WordServiceissued a check for $4,000 for the purchase of a computer. +30,000 +30,000 +700 +700 - 4,000 + 4,000 + 5,000 + 5,000 #4: The business bought office furniture on account for $5,000 from Eastern Furniture.

#5: The desk and chair previously transferred to the business by the owner were sold on account for $700. +700 -700 -2,000 -2,000 24,000 700 4,000 5,000 3,000 30,700 #6: WordService wrote a check for $2,000 in partial payment of the amount owed to Eastern Furniture Company.

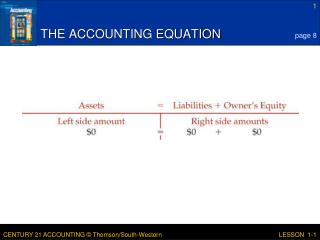

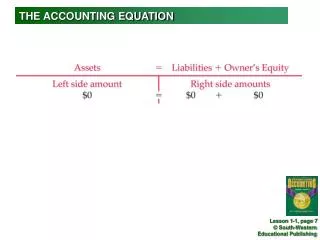

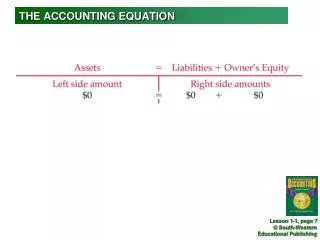

ASSETS = LIABILITIES + OWNER’S EQUITY 33,700 = 33,700

Section 3Transactions That Affect Revenue, Expenses, and Withdrawals by the Owner Financial Claims Property = Equities Assets = Liabilities Owner’s Equity Cash Decreases Assets Decreases Owner’s Equity Expenses Revenue Increases Assets Increase Owner’s Equity

Problem 3-3Determining the Effects of Transactionson the Accounting Equation (T- page 63)

Problem 3-3Transaction #1: Paid $50 for advertising in the local newspaper. -50 -50 +1,000 +1,000 -600 -600 -800 -800 +200 -200 23,750 500 3,000 30,250 4,000 5,000

Problem 3-5 Completing the Accounting Equation 1,600 10,850 1,600 9,250

Problem 3-6 Classifying Accounts Within the Accounting Equation 5,000 Cash in Bank Accounts Receivable 2,000 Camping Equipment 12,000 3,000 Office Equipment 22,000 Accounts Payable 7,000 Ronald Hicks, Capital 15,000 22,000

Problem 3-8 Determining the Effects of Transactions on the Accounting Equation +700 +700 -2,000 -2,000 +500 +500

Key Terms credit Owner’s equity Business transaction Financial claims account creditors On account property assets Accounts payable liabilities Accounting equation equities Accounts receivable investment