Download

1 / 17

170 likes | 235 Views

Monitoring, data collection, determination of market averages, and outlook for CatXL covers by Swiss Re Group using CAMARES concept for efficient risk management and capacity allocation.

E N D

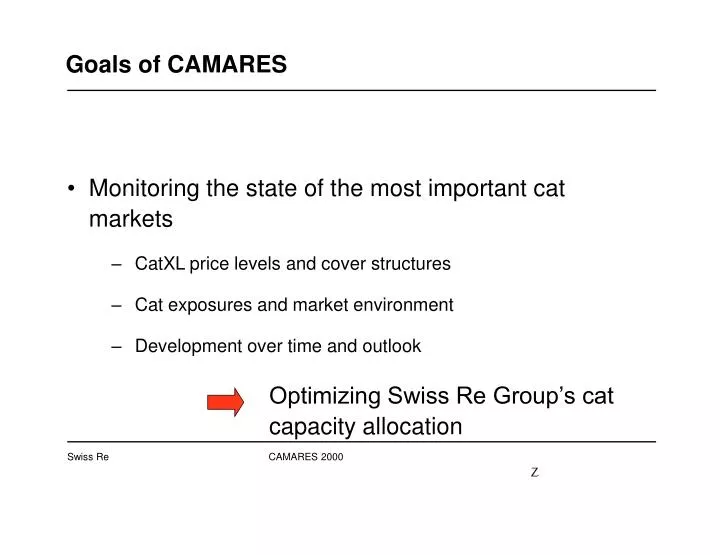

Goals of CAMARES • Monitoring the state of the most important cat markets • CatXL price levels and cover structures • Cat exposures and market environment • Development over time and outlook Optimizing Swiss Re Group’s cat capacity allocation

Concept of CAMARES • Data collection: • All Swiss Re divisions: Integrated in standard cat reporting process • Worksheets with quantifiable CatXL data for each market: GNPI, cover limits, realized rol, risk rol, cat exposure, etc. • Worksheets with mainly soft (not quantifiable) data for each market: changes in the market, estimations of market premium volume and proportional business, etc.

Concept of CAMARES (cont.) • Determination of: • Market average of price elements (realized ROL, risk ROL, loading on line LOL) • Reference loss(es) for most important cat loss potential(s) per market • Market average of cover elements (deductibles, covers, exit points) set in relation to reference loss • Return on capital per market

earthquake Market coverage in relation to reference loss

windstorm Market coverage in relation to reference loss

Evolution of price levels (CAMARES index) All markets combined

Outlook • global cat rates? • some reinsurers bankrupt, others showing high losses for 1999 • shrinking retrocession market • commitment to capacity reduction?

CAMARES 2000, main conclusions: • World-wide overall non-proportional cat covers continue to grow • Price decay has stopped and slightly reversed, albeit at widely unsatisfactory levels • Swiss Re’s own book of covers is outperforming market benchmarks and has further improved in this respect.

Risk Management and Capacity Allocation by Swiss Re • Groupwide integrated risk model (GRACE) • Overall risk measured by shortfall • “Component risk” determined via marginal contribution (Euler principle) for each peril • Required margin per peril derived from component risk