Download

1 / 38

400 likes | 467 Views

Explore the emerging commercial opportunities in Nigeria's oil and gas industry, key enablers, and interventions for growth, shared by Engnr. Funsho Kupolukun at OTC 2007 in Houston.

E N D

Commercial Opportunities in Nigerian Oil and Gas Sector Engnr. Funsho Kupolukun Group Managing Director Nigeria National Petroleum Corporation Gulf of Guinea Breakfast Session OTC 2007, Houston May 2, 2007

CONTENT • Global Oil and the Gulf of Guinea • Overview of Nigerian Oil and Gas Industry • The Growth Agenda • Emerging Commercial Opportunities • Key Enablers and Interventions • Concluding Remarks

GLOBAL OIL AND THE GULF OF GUINEAPrice Shifts In both oil and gas, there has been a band shift in prices occasioned by supply tightness and growing demand. Secure supplies is therefore a major agenda issue for the global oil and gas industry as well as governments alike

GLOBAL OIL AND THE GULF OF GUINEAGrowing Importance of Gulf of Guinea Whilst OPEC remains the primary point of call for global capacity additions, the Gulf of Guinea countries, particularly Nigeria and Angola, are evolving as geo-strategically important suppliers to the global market, particularly to the USA

GLOBAL OIL AND THE GULF OF GUINEAGulf of Guinea Prospectivity Deepwater Comparative Reserves Deepwater Discoveries The Gulf of Guinea’s growing importance is supported by a high level of prospectivity. Almost 40% (14 bn bbls) of global deepwater discoveries have come from this region. About half of this is from Nigeria. Recent discoveries have brought the region to the forefront of deepwater technologies

THE GULF OF GUINEA Projected West African Crude Oil Output World Average 3% From this robust base, a significant contribution is expected from this region to global capacity. An estimated 7mmb/d or 9% of worlds total daily production is expected to come from this region in 2007. Relative to the world average of 3%, production capacity growth in Africa (specifically Gulf of Guinea) is forecast to be highest at about 7% annually

CONTENT • Global Oil and the Gulf of Guinea • Overview of Nigerian Oil and Gas Industry • The Growth Agenda • Emerging Commercial Opportunities • Key Enablers and Interventions • Concluding Remarks

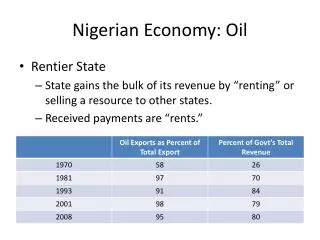

THE NIGERIAN OIL AND GAS INDUSTRY Nigeria In the Gulf of Guinea Reserves Production Nigeria is a key component of the Gulf of Guinea. It represents 70% of total Gulf of Guinea reserves and is the anchor country for the region in terms of supply

THE NIGERIAN OIL AND GAS INDUSTRYNational Aspiration for Oil and Gas Recent Presidential Mandate Core Sector Aspirations • Grow • Crude oil reserves to 40bn barrels by 2010 • Production capacity to 4.5mmb/d by 2010 • Gas revenues to match crude oil revenues • Domestic gas market and address environmental issues • Maximize sector value to the Nigerian economy • Improve Nigerian capacity and content in industry • Enhance multiplier effect on economy • Transit oil to an integrated oil and gas economy … Attain a GDP growth rate of 10% Nigeria’s aspirations for its oil and gas industry are anchored on 2 key elements – capacity growth and economic integration of the industry with the macro-economy. The nation aspires to grow GDP at a 10% rate. The strategic thrust is therefore that of alignment between global and domestic objectives.

THE NIGERIAN OIL AND GAS INDUSTRY7Industry Focus Areas • Crude Oil Capacity Growth • Aggressive exploration and development to arrest production decline and grow capacity to 4mmb/d by 2010 • Enable / Sustain Linkage of Industry to Economic Growth • Aggressive development of the National Content Agenda to facilitate manufacturing and industrial capacity growth • The Renewable Energy Initiative to stimulate agriculture sector growth • The Marginal Fields Initiative to stimulate local participation • Stimulating Gas Sector Growth • Aggressive growth of export sector to leverage evolving opportunities in global growth in gas • Stimulate domestic sector gas growth to underpin economic growth To deliver the aspirations, between 1999-2007, the industry has refocused strategically on 7 key areas vital to coping with the rapidly evolving global and local industry landscape. These 7 areas have anchored industry operational focus and the achievements to date

THE NIGERIAN OIL AND GAS INDUSTRY7 Industry Focus Areas • Stimulate Downstream Product Availability and Growth • Refinery performance improvement • Retail outlet growth • Private sector participation in product marketing • Develop Sustainable Financing Solutions for the Industry Activity • Developing Legal and Fiscal Environment to Support Sector Aspirations • Develop Organisational Capacity in NNPC to Manage and Exploit Evolving Industry Challenges and Opportunities Respectively

THE NIGERIAN OIL AND GAS INDUSTRYPerformance Update - Reserves Growth 59% increase Reserves have continued to grow steadily in Nigeria. Over 7bn bbls have been discovered in the deepwater acreages bringing the total national crude oil reserves to about 35bn bbls from about 22bn bbls pre 1999. Significant scope for reserves growth still exists

THE NIGERIAN OIL AND GAS INDUSTRYPerformance Update – Production Capacity Growth Similarly, production capacity has grown steadily to an installed capacity of about 3mmb/d in 2007. More recently in 2005/2006, an additional 790mmboed was added to the nations supply capacity. In essence despite major disruptions to production, the industry has been able to sustain production at within quota limits in view of the robust and diverse supply base

THE NIGERIAN OIL AND GAS INDUSTRYPerformance Update - Gas Sector Steady drop in % gas flared % Flared Gas flares have reduced significantly to about 32% by end 2006. Significant growth in domestic and export gas utilisation will end flares by 2008.

NLNG 22 Mtpa LNG, 3.5 Mtpa NGLs BGT L N G 24 dedicated LNG tankers THE NIGERIAN OIL AND GAS INDUSTRYPerformance Update - Gas Sector Highlights Total Investment - $11.4 bn • T12 started 10/99 • T45 FID 03/02 • T3 started 12/02 • T6 FID 07/04 • T4 started 07/05 • T5 started 12/05 • T6 RFSU 2008 • ~$1.5 bn 3rd Party financed • USD 569million dividend • Over 500 cargoes delivered NLNG was commissioned in 1999 with 2 Trains at startup. It has since expanded rapidly to 5 trains by 2005 and the 6th is planned for commissioning in 2008. To date, the NLNG project has delivered over $3.6bn in revenues to Nigeria, part of which has been reinvested for further growth.

CONTENT • Global Oil and the Gulf of Guinea • Overview of Nigerian Oil and Gas Industry • The Growth Agenda • Emerging Commercial Opportunities • Key Enablers and Interventions • Concluding Remarks

THE GROWTH AGENDACrude Oil Capacity - Future Capacity Growth To deliver the GDP aspiration as well as contribute to global economy growth, Nigeria needs to grow capacity significantly. The sector has assembled and is progressing a robust portfolio of projects planned to grow capacity to about 4mmb/d by 2010. The portfolio comprises a mix of deepwater and conventional terrain projects

THE GROWTH AGENDAOverview of Key Projects – Conventional Terrain Over 2.0mmb/d additional capacity is planned from the shallow offshore concessions between 2006 - 2011.

THE GROWTH AGENDAOverview of Key Projects – Deepwater Terrain Over 1.0mmb/d of additional capacity is anticipated from about 7 major deepwater projects.

THE GROWTH AGENDAGas Sector Growth In gas, there is a major transformation in forecast utilisation for both the domestic and export sector. Domestic demand will grow to about 1000mmscf/d by 2006 and forecast to grow to over 10,000mmscf/d by 2010. LNG capacity has equally grown from zero to 22MTPA in 2006 and forecast to grow to 50MTPA by 2011 – second fastest growth in the world. Nigeria’s forecast gas growth is one of world’s most aggressive

THE GROWTH AGENDAGas Sector Growth – Diverse Portfolio Opportunities Underpinning the gas demand growth is a robust portfolio of projects. The portfolio comprises Methanol, GTL, Power and Fertilizer projects

THE GROWTH AGENDA Major Export Projects - LNG Projects NLNG • NLNG capacity forecast 30MTPA by 2012, fastest growing LNG plant in the world • Total Investment - $11.4bn; Project has delivered over $3.6bn in revenue to date • 22MTPA LNG, 3.5 MTPA NGLs • T1-5 on production; T6 FID 07/04; • Over 500 cargoes delivered OKLNG • OKLNG project will boost Nigeria LNG capacity by 22MTPA from 2011 • 22 million tonnes/year LNG Project ; 4 LNG trains of 5.5 million tonnes/yr • Trains 1 & 2 produce 100kb/d NGLs • Launch Project – trains 1 & 2 ; trains 3 & 4 to be added thereafter • FEED Commenced Feb 2006 BRASS LNG • Project sponsors – NNPC, NAOC, ConocoPhillips • Two LNG trains of 5MTPA capacity each • All agreements including shareholders’ agreement have been concluded • FEED for the plant and facilities nearing completion • FID targeted for December 2007

THE GROWTH AGENDAMajor Export Projects – Other Pipeline Projects WAGP • 630 km pipeline to deliver gas to Benin, Ghana and Togo by Q1 2007 • Initial capacity is 200 mmscf/d but will grow to 580 mmscf/d • Position Nigeria to effectively capture the emerging markets of West Africa • Construction commenced in 2005, commissioned April 2007 Other Regional Gas Pipeline Projects • 2 Key Projects • Equatorial Guinea Gas Supply • Trans-Sahara Gas Pipeline • About 650mmscf/d to Equatorial Guinea and 2bcf/d thro the TSGP • Strengthen regional cooperation and economic stability • Anchors Nigeria as regional supply hub

UPSTREAM PERFORMANCE 1999-2007Crude Oil Capacity Growth – Funding Capacity Additions NB:- 2006 investment includes IPP The crude oil capacity growth has translated into major investment inflow in the industry. For instance between 2000 and 2006, FGN funding levels more than doubled from about $2.5bn to over $6bn.

THE GROWTH AGENDAIndustry Investment Levels Over $60bn is anticipated to be spent through to 2008 alone and significantly more in future years. Relative to competing OPEC countries, Nigeria is experiencing one of the highest investment inflows in the industry creating opportunities

CONTENT • Global Oil and the Gulf of Guinea • Overview of Nigerian Oil and Gas Industry • The Growth Agenda • Emerging Commercial Opportunities • Key Enablers and Interventions • Concluding Remarks

EMERGING OPPORTUNITIESGas Pipeline Infrastructure Proposed Gas Pipeline Network • Pipeline Capacity Growth and Extensions: • Expand existing ELPS throughput capacity • New pipeline linkages from South to North • Interconnector between East and Western grid • Connectors between domestic and export To support the growth in gas utilisation, a major growth in gas pipeline infrastructure is planned. An infrastructure blueprint is currently being developed which will triple the gas transmission capacity in the next few years

EMERGING OPPORTUNITIESGas Processing Plants • Central Processing Facilities • About 3-4 gas processing plants are required to support growth • Plants will be able to strip NGLs • Plants may be tolling / merchant plants or owned by the equity owners of the gas • The CPFs need to be in place by 2009/2010 when gas demand peaks About 3-4 gas processing plants with capability to strip NGLs is required by 2009/2010. These could be merchant plants

EMERGING OPPORTUNITIESOtherGas Support Services • Metering, monitoring and Control Systems • Pipeline integrity systems • Gas specification management systems • Other maintenance and support systems In addition, there will be numerous opportunities in the support services for gas to cope with the massive growth in gas delivery systems

EMERGING OPPORTUNITIESENGINEERING & FABRICATION With over $85bn spend in the next 5 years and Policy requirements to domicile Engineering Design and over 50% of fabrication works in country, international EPC companies, Investors & engineering companies are welcome to set up in Nigeria

EMERGING OPPORTUNITIESCONSTRUCTION & INSTALLATION KEY INDICATORS FOR INVESTMENT OPPORTUNITIES • Over 4000 km of med/ large dia pipeline to be installed • Installation of jackets, decks, platforms, etc(1250k MT) • Integration, hook-up & commissioning of all future FPSOs & Platforms MC Dermott Lay barge Identified gaps Marine construction equipment & support bases Inspection services & project Mgt support Pipe-lay & Crane Barges Pipe Spooling facilities Support clusters & skilled Maintenance crew The Nigerian Content Policy is strongly linked to the cabotage act which requires Nigerian Flagging of vessels operating in Nigerian waters. Coupled with the spike in work load, opportunities abound for new entrants to buy into this emerging segment.

EMERGING OPPORTUNITIESSHIPPING & MARINE SERVICES The Nigerian Oil and Gas industry is open to investors who are keen to partner with Nigerian companies in the provision of Tankers and coastal vessels to service the operations. This will offer additional opportunity in the areas of Ship Management expertise and training of seafarers

CONTENT • Global Oil and the Gulf of Guinea • Overview of Nigerian Oil and Gas Industry • The Growth Agenda • Emerging Commercial Opportunities • Key Enablers and Interventions • Concluding Remarks

ENABLING INITIATIVES Targeted Incentives for Investors Effort is ongoing to secure a targeted set of incentives for would-be investors who need to install major capacity in Nigeria. The incentives include some guaranteed work to justify investment

ENABLING INITIATIVES Free Trade Zones 4 Free Trade Zones • Calabar • Lekki • Olokola • Onne • No corporate income tax • No customs & excise duty on imports • Centralised approval process for permits – one stop shop • Excise duty on exports only Key Incentives Free trade zones will provide significant incentives for oil and gas investors by lowering investment barriers and enhancing project profitability

ENABLING INITIATIVES Niger Delta Interventions Despite investment by successive governments and corporations, the level of success of many of the past initiatives have been largely low and unsustained

CONTENT • Global Oil and the Gulf of Guinea • Overview of Nigerian Oil and Gas Industry • Emerging Commercial Opportunities • Key Enablers and Interventions • Concluding Remarks

CONCLUDING REMARKS A New Dawn The Nigerian Oil and Gas industry is set for a second phase of growth. Rapid Capacity Growth The opportunities are immense at over $60bn and the landscape is being prepared for willing investors to participate. Please join us. Huge Opportunities