Download

1 / 21

210 likes | 220 Views

This report outlines the background, legal requirements, and process of the In-Year Management, Monitoring, and Reporting System. It includes practical examples and discusses the purpose and benefits of the system.

E N D

IN-YEAR MANAGEMENT, MONITORING AND REPORTING SYSTEM (SECTION 32 REPORTS) Provincial Budget Analysis Intergovernmental Relations National Treasury 08 August 2006

Outline • Background • Legal requirements • In-year monitoring process • Reports generated • Practical examples

Background • Sparked by 1997/98 financial crisis in provinces • Provinces overspent by R5,8 billion in aggregate • Monitoring system (EWS) approved by Cabinet • Change in the Budget Process • IYM to constitute: • Expenditure management • Revenue management • Cash flow management • Movements in bank balances • Suspense accounts

Legal Requirements • Section 32 of PFMA • Publishing reports on state of budgets • Section 40(4) of PFMA • Sections 24 to 27 and 29(4) of the Division of Revenue Act, 2006 (CGs) • Acts require monthly expenditure and revenue reporting to the provincial treasuries and National Treasury

In-year Management, Monitoring and Reporting • Accountability Cycle: • Strategic and Performance Plans • Budget • In-year monitoring (IYM) (Inform SP targets) • Quarterly Performance Reports (piloting) • Annual Reports • Purpose: • Focus on performance against budget • Alert managers where remedial action is required • Reports serve as management tool • Feed the Budget Process • Feed into publications such as the Annual Intergovernmental Fiscal Review • Political level to make decisions

In-year Management, Monitoring and Reporting • Monthly reports facilitate: • Flow of information • Internal control measures to deal with problems timeously (Early Warning System) • AO is more proactive • Use data to make decisions • Compilation of annual reports and financial statements which completes the accountability cycle • Assist the external auditor • Reduced timeframe for audit - strengthen accountability to legislatures • Reports consolidated and published in Government Gazette

Monthly Reporting Process (1) • Accounting officer must submit reports to relevant treasuries and executive authorities within 15 days of the end of each month • To improve accountability, AOs are required to sign-off on the monthly reports before submitting to relevant treasury or executive authority • Contents of reports – legal requirement (S40): • Actual revenue and expenditure • Projections for remainder of financial year • Information on conditional grants • Any material variances • Format determined by the National Treasury in terms of PFMA and annual DoRA • Revised annually

Monthly Reporting Process (2) • Formats – • Require variances between the actual result for the period and that budgeted • Projections to the end of the financial year • Reasons for deviations • What has happened so far? • What will happen for the rest of the year? • What actions to be taken to achieve agreed plan?

Monthly Reporting Process (3) • Number of steps in the process to convert the millions of individual transactions that occur as a result of government activities into the information to be published monthly • Undertake reconciliations • Check allocation of transactions • Clear errors and suspense items • Balance various type of accounts • Return date 15th of each month to provincial treasuries and 22nd of each month to National Treasury • System resources: BAS, PERSAL and Vulindlela • From 1 April 2004: • New Economic Reporting Format • Migration to BAS • Standard Chart of Account (SCOA) • Single version of the truth

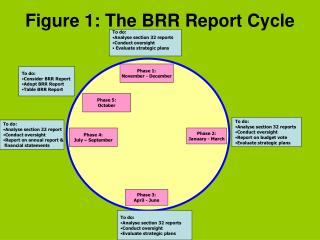

The In-Year Monitoring Process Dept IYM Data file + Dept IYM report signed by HOD Provincial Treasury Collates and imports all departmental IYM data file into treasury IYM Model (built in function) to generate provincial IYM report • Provincial Treasury updates IYM Model with all Dept IYM data files and generates IYM data file National Treasury • Imports IYM Data file into IYM Model also receives all dept signed IYM summary reports via post before 25th of month + prov treasury spending / variance report

Reports Generated • Section 32 Publication • Press Release • Technical Committee for Finance (TCF) • Budget Council • President’s Co-ordinating Council (PCC) • Select Committee for Finance

Interpretation of Reports (1) • 1st Quarter report (practical examples): • 1st Q 2005/06 to 1st Q 2006/07 spending growth • Why low growth in Education (2,2%), in particular Personnel (1,4%)? • Why drop in expenditure from 4th Quarter in 2005/06 (R59,9bn) to 1st Quarter in 2006/07 (R38,4bn)? • Are projections a reasonable reflection of likely expenditure outcomes for the financial year? • Spending on Social Welfare Services (Social Development) at 17,7% - why lower than aggregated average?

Movement from 1st Quarter 2005/06 to 1st Quarter 2006/07

Interpretation of Reports (2) • It should be noted that one cannot necessarily draw meaningful conclusions by only looking at the first quarter financial results given the fact that it is relatively early in the financial year • Provinces are projecting to overspent by R2,1 billion • Once anticipated provincial roll-overs, which will be reflected in the provincial adjustments budgets,are taken into account on the budget side, the overall outcome would change • The adjustments budgets are reflected in the 3rd quarter and 4th quarter publications