Download

1 / 45

450 likes | 701 Views

Bond Pricing. Riccardo Colacito. What is a bond?. A security that obligates the issuer to make specified payments to the holder over a period of time How to compute the price? Yield to maturity? Risk considerations?. Types of Bonds. Treasury Bonds Corporate Bonds Callable Convertible

E N D

Bond Pricing Riccardo Colacito

What is a bond? • A security that obligates the issuer to make specified payments to the holder over a period of time • How to compute the price? • Yield to maturity? • Risk considerations?

Types of Bonds • Treasury Bonds • Corporate Bonds • Callable • Convertible • Floating rate • International Bonds • Foreign • EuroBonds

Key terms • Face or Par Value • Premium vs Discount • Price of the Bond • Coupon Rate • Zero Coupon • Maturity • Yield to maturity

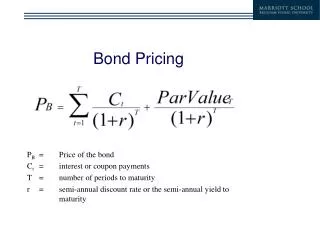

Bond Pricing PB = Price of the bond C = interest or coupon payments Par = Par or Face Value of the Bond T = number of periods to maturity r = yield to maturity T å C Par P = + B + T + ( 1 r ) t ( 1 r ) = t 1

Example • Par Value = $1,000 • Coupon = 4% of Par (i.e. $40 semiannual) • Price = $1,231.15 • Maturity = 20 years (i.e. 40 periods) • Yield = ?

Yield to Maturity • The discount rate that makes the present value of a bond’s payment equal to its price • E.g. solve for r in the previous example • Need computer or financial calculator to solve for r=3%

A simpler case A zero coupon bond • Par Value = $1,000 • Coupon = $0 • Price = $300 • Maturity = 20 years (i.e. 40 periods) • Yield = ?

A simpler case (cont’d) • From previous formulas • Use approximation:

Rule of thumb • When you want to know what is the appropriate yield on a bond of a given maturity, compute it using a Treasury zero coupon bond (it’s simple!) • Use this discount rate to compute what should be the actual price of any other bond of equal maturity that pays a coupon (it’s not too hard! See next example…) • If their current price is significantly lower, then it means that they are relatively riskier (default risk?)

Example • Par Value = $1,000 • Coupon = 4% of Par (i.e. $40 semiannual) • Price = ? • Maturity = 20 years (i.e. 40 periods) • Yield = 3%

Figure 9.3 The Inverse Relationship Between Bond Prices and Yields

Intuition • If current interest rate is 4% (on a semi-annual basis), coupon is also 4%, then the bond is not giving anything “extra”: • If current interest rate is 10% (on a semi-annual basis), coupon is 4%, then the bond is paying less in coupons than it should: the compensation must come in the form of a discount price! • If current interest rate is 1% (on a semi-annual basis), coupon is 4%, then the bond is paying more in coupons than it should: the compensation must come in the form of a premium price!

Premium and Discount Bonds (cont’d) • Premium Bond • Coupon rate exceeds yield to maturity • Bond price will decline to par over its maturity • Discount Bond • Yield to maturity exceeds coupon rate • Bond price will increase to par over its maturity

Figure 9.6 Premium and Discount Bonds over Time • As maturity approaches, the prices must converge to Par • Look at the general formula to see this!

Changing maturities • How would the relationship between prices and yields change for different maturities? • Why?

Intuition If: • maturity increases • Coupon rate is more than market rate You would be at a gain for a longer time!

Intuition (cont’d) If: • maturity increases • Coupon rate is less than market rate You would be at a loss for a longer time!

YTM and HPR • A ten year bond sells today with the following characteristics: • Par = $100 • Coupon = $3 (semi-annual) • Price = $100 • A Nine year Bond sells tomorrow with the following characteristics: • Par = $100 • Coupon = $4 (semi-annual) • Price = $100 • What should happen tomorrow to the price of the 10 year bond? • What is your return from holding the 10 year bond for 1 year?

Argument • Today the YTM on the 10 year bond is 3%. (Remember what we said before!) • Tomorrow the YTM on the 9 year bond is 4% (same argument). • Hence the 10 year bond is becoming less attractive. • For the 10 year bond to be marketable, its price must drop: how much?

How much? • Bond characteristics: • Par = $100 • Coupon = $3 (semi-annual) • Maturity = 9 years (10 years minus the one that just ended) • New YTM = 4% • Compute the new price

HPR on the 10 year bond • The HPR is

The bottom line • HPR and YTM are not the same thing!!! • Only when the discount rate does not change from year to year, the HPR is equal to (twice) the YTM

Other details • Listing conventions • Pricing between coupon rates • Yields and Prices for a callable bond

Listing conventions • Bond equivalent yield = 2 x r (financial press) • Effective annual yield = (1+r)^2 – 1 • Accounts for compounding • Current yield = annual coupon divided by bond price

Pricing between coupon dates • Must pay the seller for interests accrued Invoice Price = Listed Price + Accrued Interest where

Term Structure of Interest Rates • Relationship between yields to maturity and maturity • Yield curve - a graph of the yields on bonds relative to the number of years to maturity

Theories of Term Structure • Expectations • Long term rates are a function of expected future short term rates • Upward slope means that the market is expecting higher future short term rates • Downward slope means that the market is expecting lower future short term rates • Liquidity Preference • Upward bias over expectations • The observed long-term rate includes a risk premium

Forward Rates Implied in the Yield Curve • For example, using a 1-yr and 2-yr rates • Longer term rate, y(2) = 8.995% • Shorter term rate, y(1) = 8% • Forward rate, a one-year rate in one year = 10%

Liquidity preference theory • Investors demand a premium as a compensation for the greater risk of longer term bonds

Default Risk and Ratings • Rating companies • Moody’s Investor Service • Standard & Poor’s • Fitch • Rating Categories • Investment grade • Speculative grade

Factors Used by Rating Companies • Coverage ratios: ratio of earnings to fixed costs • Leverage ratios: debt-to-equity ratio • Liquidity ratios: current assets/current liabilities • Profitability ratios: e.g. return on asset (earnings before interest and taxes divided by total assets) • Cash flow to debt: cash received or expended as a result of the company’s core business activities to debt ratio

Protection Against Default • Bond indentures: a contract between issuer and bondholder that specifies payments and other restrictions • Indentures • Sinking funds: requires the issuer to periodically repurchase some portion of outstanding bonds prior to maturity • Subordination of future debt: restrict borrower in issuing too much additional debt in the future • Collateral: to guarantee partial repayment in case of default