Download

1 / 34

340 likes | 432 Views

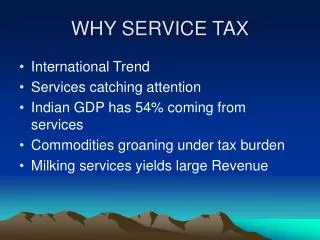

WHY SERVICE TAX. International Trend Services catching attention Indian GDP has 54% coming from services Commodities groaning under tax burden Milking services yields large Revenue. SERVICE TAX & CONSTITUTION. Service not defined Article 246 read with Union List Residual entry no 97

E N D

WHY SERVICE TAX • International Trend • Services catching attention • Indian GDP has 54% coming from services • Commodities groaning under tax burden • Milking services yields large Revenue

SERVICE TAX & CONSTITUTION • Service not defined • Article 246 read with Union List • Residual entry no 97 • New entry no 92 – C covers taxes on services • Constitution amendment in 2003

SOME UNIQUE ASPECTS OF SERVICE TAX • Tax payable only on payments received • Self adjustment of excess tax • Centralized Registration • Cenvat Credit across goods and services • Bi – Annual Returns

SERVICE TAX LEGAL FRAMEWORK • Finance Act 1994 as amended • Service Tax Rules 1994 • Service Tax Valuation Rules 2006 • Cenvat Credit Rules 2004 • Export of Services Rules 2005

CONTD. • Import of Services Rules 2006 • Service Tax Advance Rulings Rules 2003 • Registration of special category of persons Rules 2005 • The Works Contract Rules 2007

REGISTRATION • Threshold limit of Rs 10 lacs • Tax not payable till payments received cross 9 lacs , with reference to previous year • Single Registration for all services • Centralized Registration

IMPORTANT FORMS • ST – I application for Regn • ST – 2 Regn certificate • ST – 3 Return • ST-3A Provisional assessment • ST – 4 Appeal to commissioner ( Appeals)

CONTD. • ST 5 Appeal to CESTAT • ST 6 Memorandum of Cross Objection

RULES OF CLASSIFICATION • Specific definition preferred • Test of essential character for composite services • Service brought into the tax net earlier than the other

VALUATION • New section 67 • Value should be fullest consideration • Otherwise Valuation Rules to apply • Comparison with similar service • Finding out cost of provision of service

CONTD. • Provision for rejection of value by Departmental Officers • SCN & PH necessary • Speaking order • Rule 5 and the concept of pure agent • Expenditure of pure agent excluded

CONDITIONS FOR PURE AGENT • Service provider as the pure agent • Of the recipient of the service • Payments to third party by agent • Recipient to receive and use the goods and services procured by the agent • Recipient to be liable to pay third party

CONTD. • Recipient authorizes service provider to make payment to third party • Recipient has knowledge of transactions with third party – supply and payment • Agent’s payments to be invoiced separately on recipient

CONTD. • Invoicing of recipient in this should be at actual • Service provided as agent should be in addition to own services being provided • Agency contract essential • Agent not to use the goods and services procured and provided

CONTD. • Agent should not hold any title to the goods and services so provided • Should receive only actual payments to the extent of costs incurred

Problem areas in service tax valuation • Deduction of cost of reimbursable expenses • Exclusion of the cost of value of materials consumed in providing service • Interpretation of the notification no 12/2003 dated 20-6-2003 • Case studies : • Photography service and Tyre retreading

Continued----- • Cum – Tax Value • Commissioner of service tax, Bangalore Vs Prompt and Smart security – 2008 ( 9 ) STR ( Tribunal- Bangalore ) • Malabar Management services Vs Commissioner of service tax, chennai -2008 ( 9 ) STR ( Tri- Chennai )

Continued---- • Excludability of the cost of materials in the assessable value in the operation of power plants • CMS ( India ) Operations & Maintenance co pvt ltd Vs Commissioner – 2007 ( 7 ) STR 369 ( TRI) • Covanta Samalpatti operating co pvt Ltd- 2008 ( 10 ) STR 133 ( Tri )

Case studies on certain problem services • Consulting Engineer service : • Technology transfer and royalty payments • Indivisible contracts • Ratio of the Daelim case • Goods Transport Agency service • Works contract service

Continued----- • Management , maintenance and repair service: • Maintenance of computer software • Renting out of immovable property service • Residential construction service

Service tax credit • Capital goods used for providing output service • It includes motor vehicles registered in the name of service provider, namely: • Courier agency • Tour operator • Rent a Cab scheme operator • Cargo handling agency

continued • Goods transport agency • Outdoor caterer • Pandal and shamiyana contractor ( caterer )

continued • INPUTS: • All goods except light diesel oil, HSD and petrol, used for providing output service • Or used in or in relation to the manufacture of final products or any other purpose, within the factory of production

continued • INPUT SERVICE • Any service -------- • Used by a provider of taxable service for providing an output service, or • Used by a manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products upto the place of removal

continued • And includes services used in relation to--- • Setting up • Modernization • Renovation • Repairs --- • Of a factory, • Premises of service provider

continued • Or an office relating to such factory or premises, • Advertisement • Sales promotion • Market research • Storage upto the place of removal • Procurement of inputs

continued • Activities relating to business such as ---- • Accounting • Auditing • Financing • Recruitment and quality control • Coaching and training • Computer networking

continued • Credit rating • Share registry • Security • Inward transportation of inputs or capital goods • Outward transportation upto the place of removal

Export of services • Exempt , subject to conditions • Services in relation to immovable property • Services partly performed in India and partly abroad • Services in relation to business or commerce abroad, where the recipient of the services is located abroad and in case

continued • Such recipient has commercial establishment or an office in India, the order for such service is made from any of his office or commercial establishment abroad. • All services are to be provided from India and used outside India • Payment in convertible foreign exchange

Import of services • Services criteria same as for export of services • Reverse charge • Imported services not to be treated as output services • Implications of the above

Service tax refund/ rebate • Self adjustment • Section 11B cash refund • Refund under Rule 5 of CCR 2004 • Rebate under form ASTR 1 • Rebate under form ASTR 2 • Bar of unjust enrichment

continued • Refund claim through credit notes • Case laws: • Mafatlal Industries Vs union of India • L&T sargeant Lundy Ltd vs CCE, Vadodara

Important procedures in service tax law • Provisional assessment and interest liability • Input service distributor • Advance payment and self adjustment • Payment of amount in lieu of service tax in works contract service