Download

1 / 27

270 likes | 367 Views

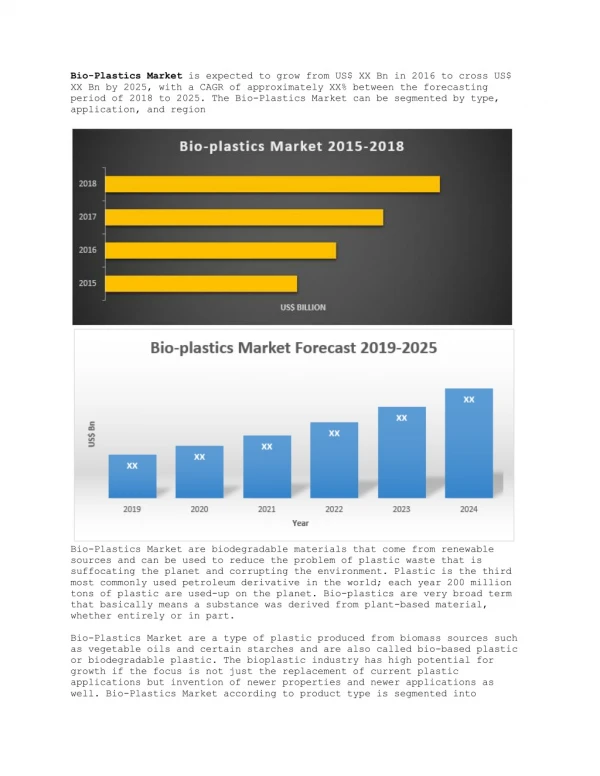

Developing Markets for Bio-based Plastics Opportunities and Challenges. Dr Adrian Higson NEPIC Innovation Day 15 th November 2011 Ramside Hall, Durham. Today’s Presentation. About the NNFCC Bioenergy development Process options Land for Chemicals Closing thoughts.

E N D

Developing Markets for Bio-based PlasticsOpportunities and Challenges Dr Adrian Higson NEPIC Innovation Day 15th November 2011 Ramside Hall, Durham

Today’s Presentation • About the NNFCC • Bioenergy development • Process options • Land for Chemicals • Closing thoughts

The UK’s National Centre for Biorenewable Energy, Fuels and Materials An Independent ‘not for profit’ company Mission The NNFCC is committed to the sustainable development of markets for biorenewable products. We promotes the benefits of biorenewable energy, liquid fuels and materials for enhancement of the bioeconomy, environment and society.

Renewable Energy Policy Mandatory EU target of 20% renewable energy in overall energy consumption by 2020

The importance of bioenergy In 2009, bioenergy accounted for 81% of all renewable energy utilization. Biomass will be the dominate renewable energy source in 2020 Source DECC ‘UK Renewable Energy Roadmap’

A role for Biomass (Energy) Crops? A wide range of scenarios from many models give very different supply estimates because of differing assumptions Source: Slade, Gross and Bauen 2010: Estimating bio-energy potentials to 2050

Complexity of biorenewables Adapted from Dornburg 2008, in Bioenergy – a sustainable and reliable energy source (IEA Energy, 2009)

Biomass Value Proposition Increasing value Decreasing volume

Market Dynamics Climate change Mandates/Support Brand owner focus Environment Functionality Volatility Hedging Future proofing Industrial Biotechnology

Biorenewable Chemicals and Polymers Market size ~ 50 million tones Fermentation Products

Specification Driven Renewable Resources Industrial Biotechnology Low volume, High price High volume, Low value Renewable Resources Function Driven

Plastics market UK Household Waste (2002)

Reduce, Reuse, Recycle EU Waste Framework Directive 2008/98/EC

Fuel and chemical platforms Ethanol production ~ 60 million tonnes Ethylene production ~ 110 million tonnes Source: NexantChemSystems

Bio-based chemicals – growth potential Source: NNFCC

Defining questions • What’s the value proposition in bioplastics? • Function vs renewable content • What does the environmental footprint look like? • greenhouse gas emissions, water impacts • How big is the potential market opportunity/impact? • niche or mainstream • true rate of development • What do the resource requirements look like? • Availability, price, impact on other markets • How will technology develop? • Synthetic biology, perennial crops etc Time horizons 2020 2030 2050

Land availability and use • Global land area - 13.5 billion hectares • Agricultural area - 5 billion hectare • Arable area (crop land) - 1.5 billion hectares • Technically, additional 2 billion hectares available for rain fed crop cultivation. • However, what is the limit of sustainable expansion? • What are the environmental and societal implications of expansion and land use change? Global land by use Source FAO statistics

‘Scenario’ 2030 land requirements (no residue use) Plastic demand – 428 million tonnes Land availability – 250-800 million ha (Source FAO)

Production regions Biomass crops in development Sustainable agriculture Established agri supply chains Strong technology base Limited political support Expensive to operate Sustainable agriculture Established agri supply chains High residue availability Strong technology base Strong political support Agricultural sustainability? Land availability? Strong political support Access to growing markets Established cultivation and processing Agricultural sustainability? Available arable land High crop yields (sugar cane) Good residue availability (bagasse) Good access to growing markets Large arable land potential Limited access to skills Limited access to markets

Sustainability through supply chain controlRound table for sustainable biofuel 12 Principles for sustainable production • Legality • Planning, Monitoring and Continuous Improvement • Greenhouse Gas Emissions • Human and Labour Rights • Rural and Social Development • Local Food Security • Conservation • Soil • Water • Air • Use of Technology, Inputs and Management of Wastes • Land Rights

Closing thoughts • There is insufficient land globally, to sustainably co-produce projected future demand for energy, liquid/gaseous fuel and bio-based plastics. • Therefore, in the near and long term there will be competition for renewable raw materials. • However all sectors will benefit from the market development, e.g. cultivation, logistical and technology developments. • Sustainable production is a function of supply chain control not of feedstock or cultivation region. • Efficiency requires integration - biorefineries

Bioplastics- Closing thoughts • Assuming the energy potential of sustainable available land is used for fuel and chemicals then 20% of plastic substitution in 2050 is feasible. • Carbon efficient production routes minimise land requirements e.g. carbon efficient fermentations such as succinic and lactic acids preferred over ethanol platforms. • Market development will be slow, bioplastics are not biofuels. • Dependent on technology breakthrough • Dependent on financing • Supply chain development (producers, compounders, converters) • Not politically mandated • Slow market development allows time for supply chain to develop and sustainable practices to be implemented.

Energy & Material Synergy Maximise value of biomass through carbon use in mateials Maximise the use of material at the end of life, recycle, recover etc Integrate production (material, heat and energy) where possible CO2 Energy Cycle MaterialCycle End of life/Raw material Cultivation

Thank you for listening Any questions? Join the NNFCC @ www.nnfcc.co.uk Follow us on Twitter @NNFCC