Download

1 / 17

170 likes | 275 Views

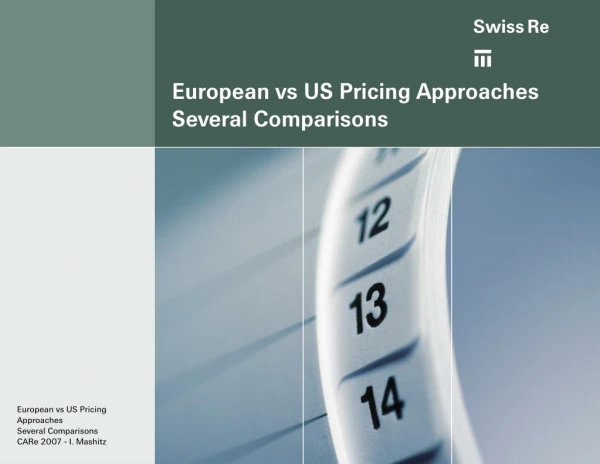

7 May 2007. European Pricing Approaches CARe Philadelphia, PA. Timothy Aman, FCAS MAAA Managing Director, Guy Carpenter Miami. Introductions. Isaac Mashitz, Chief Pricing Actuary, Swiss Re (Armonk, NY) Bryan Ware, Director, Navigant Consulting (Philadelphia, PA)

E N D

7 May 2007 European Pricing ApproachesCARePhiladelphia, PA Timothy Aman, FCAS MAAA Managing Director, Guy Carpenter Miami

Introductions • Isaac Mashitz, Chief Pricing Actuary, Swiss Re (Armonk, NY) • Bryan Ware, Director, Navigant Consulting (Philadelphia, PA) • Steve White, Managing Director, Guy Carpenter (Seattle, WA) • Tim Aman, Managing Director, Guy Carpenter (Miami, FL)

Perspective • Numbers • Education • Roles • Perspective • Competitive Environment • Financials • Regulation • Data

Numbers Source: www.actuaries.org

Numbers • Insurance premium • Europe $1,241 billion • North America $1,222 billion • Life insurance premium • Europe $ 759 billion • North America $ 552 billion • Non-Life insurance premium • Europe $ 482 billion • North America $ 670 billion Source: www.swissre.com

Numbers Source: www.actuaries.org, www.swissre.com

Education • Europe • In general, university education in actuarial science • Some countries require graduate studies and/or additional examinations • Combined Life / Non-Life curriculum • North America • Examination system • Separate Life (SOA) and Non-Life (CAS) societies

Roles • How many actuaries are working in P/C actuarial roles? • Europe • Research focus • Non-actuarial positions • North America • Applied (pricing, reserving) focus

PerspectiveInsurance • Insurance business mix EuropeUS / Can • Property 24% 27% • Motor 38% 41% • Liability 10% 14% • WC 0% 11% • A&H 17% 2% • Other 11% 5% Source: Axco

PerspectiveReinsurance • Reinsurance business mix1EuropeUS / Can • Property 46% 34% • Motor 21% 8% • Liability & WC 20% 35% • Other 3% 23% • Reinsurance type2 • Proportional 70% 50% • Non-Proportional 30% 50% • P & C Reinsurance Demand3 $ 51 b $ 65 b Source: 1 Axco, 2 Estimated, 3 A M Best Co

PerspectiveCY Combined Ratios of major non-life markets Source: Swiss Re Economic Research $ Consulting

PerspectiveMarket Concentration • Insurers • Europe 30% market share for top four • North America 18% market share for top four Market share for top ten non-life insurers Sources: Canadian Insurance, A M Best, Swiss Re Economic Research & Consulting

PerspectiveMarket Concentration • Reinsurers • Europe > 40% market share for top two • North America < 20% market share for top two Source: Estimated

Competitive Environment • Europe • Open insurance rating • Market price “communication” between competitors • Insurance • Reinsurance • North America • Insurance rate regulation varies by state • Insurance rating bureaus • Strict antitrust regulation • Open reinsurance rating

Financials • Europe • International Accounting Standards • “Embedded value” reporting • Calendar Year Quota Share treaties • Solvency focus • North America • GAAP accounting • More working-layer XL treaties • Earnings stability focus

Regulation • Europe • Pan-European regulation • Solvency II • Market-value liabilities • North America • State regulation • Appointed actuary • Statutory liabilities

Data • Europe • Little industry data • Reinsurer data access • North America • Data filing requirements • Industry statistical databases • Industry trend factors, increased limits factors, loss costs