Download

1 / 50

520 likes | 806 Views

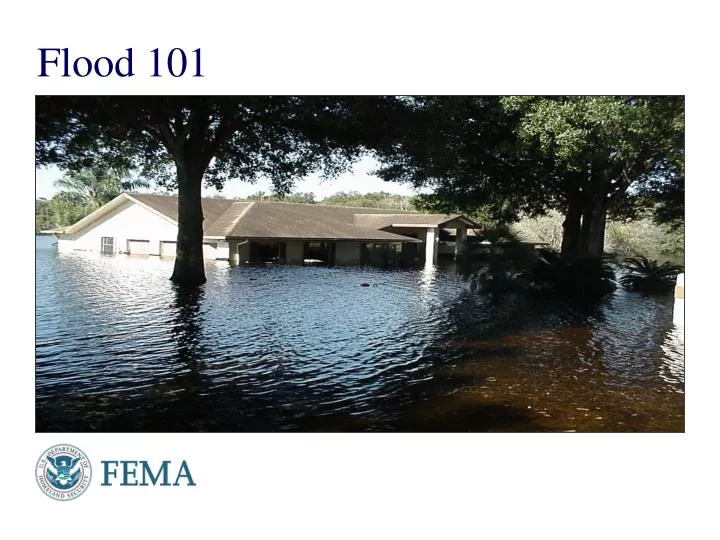

Flood 101. A Federal program enabling property owners in participating communities to purchase flood insurance protection An alternative to disaster assistance Based on an agreement between the community and the Federal Government. What is the National Flood Insurance Program?.

E N D

A Federal program enabling property owners in participating communities to purchase flood insurance protection An alternative to disaster assistance Based on an agreement between the community and the Federal Government. What is the National Flood InsuranceProgram?

History of the NFIP Section 1304 of the 1968 Act authorizes the Director of FEMA to establish and carry out “a national flood insurance program which will enable interested persons to purchase insurance against loss resulting from physical damage to or loss of real property or personal property” resulting from flood.

Benefits of the NFIP • Protects property owners from risk • Lowers the cost to taxpayers • Helps businesses re-open

Presidential declaration S.B.A loans Average Grants $2500 Loan payment on $50,000 is over $300 per month Claims are always paid No payback Losses paid up to $250,000 on building and $100,000 on contents Disaster assistance vs. Flood insurance

To educate American property owners about the risk of flood To provide flood insurance To accelerate recovery from flood To mitigate future flood losses To reduce the personal and national costs of disaster Mission of the NFIP

An agreement between FEMA and the insurance industry What is the Write Your Own (WYO) program?

Introduction to Write-Your-Own Program In 1981 the Federal Insurance Administrator (FIA) contracted : • insurance company representatives • Insurance trade organizations In July of 1983 the “model” arrangement for the WYO Program was made final.

On August 16, 1983, an invitation was extended to all licensed property insurance companies to participate in WYO for fiscal year 1984. Since 1983 the WYO Program has become the primary vehicle for the delivery and service of flood insurance.

To increase the NFIP policy base To improve service to the NFIP policyholders To encourage private insurance industry’s participation in the flood insurance program Goals of the WYO program

The number of NFIP policies in force has increased from about 95,000 before the Flood Disaster Protection Act of 1973, to 2.2 million in 1989, to approximately 5.6 million currently. As of January, 2010 - • The amount of flood insurance coverage in force is $1,218,776,526,200. • Written Premium is $3,198,025,198

Top 5 States Florida 2,146,451 Texas 682,874 Louisiana 483,326 California 275,491 New Jersey 228,982

National Flood Insurance Fund The instrument through which the Federal Government fulfills its financial responsibilities for the NFIP. Annual revenue consists mostly of premiums and a Federal Policy fee on each policy sold or renewed.

NFIP Debt Borrowing authority: $20.775 billion Outstanding Treasury borrowing: $18.75 billion as of March 2010 Most recent repayment: $250 million in December 2009

For any eligible structures A homeowner, renter, or business owner residing in a participating community There are 20,532 participating communities nationwide Who can buy flood insurance?

What buildings cannot be insured for flood? • Buildings in violation of floodplain management ordinances • New construction located in coastal barrier resource areas (CBRA Zones)

Goal is to reduce flood losses Provides incentives for carrying out activities above the minimum requirements Each insured gets a 5% to 45% discount on their flood policy What is the CommunityRating System?

National Flood Disaster Protection Act (1973) Mandates the purchase of flood insurance under certain conditions if a property is in a Special Flood Hazard Area (SFHA). National Flood Insurance Reform Act (1994) Increases participation in the NFIP Is flood insurance mandatory?

The Standard Flood Insurance Policy (SFIP) • Three forms • Dwelling Form • General Property Form • Residential Condominium Building • Association Policy (RCBAP) Effective 08/01/2004

Waiting Period • NFIP cannot “bind” coverage • Must wait 30 days from the date of application and premium presented before policy becomes effective • Does not apply when a new flood policy is required.

Program Limits • Residential Building (1-4 family) $250,000 • Contents $100,000 • Other Residential (more than 4) $250,000 • Contents $100,000 • Non Residential Building $500,000 • Contents $500,000

Grow number of flood insurance policies in force by 5% annually Lessen financial consequences of flooding for homeowners and small businesses Increase understanding of the risks and consequences of flooding NFIP Marketing Goals

FloodSmart Marketing Campaign Overview: Informs the public about flood risks and the availability of flood insurance Combats misconceptions Engages partners and influencers Connects consumers to agents Provides useful tools for insurance agents FloodSmart Marketing Campaign

Audiences Consumers Homeowners, renters and businesses Prospects, current policyholders and former policyholders Agents/Industry Influencers Federal/Regional/State/Local Partners FloodSmart Marketing Campaign

Sources of Flooding • Testimonials of real life floods that occur from a number of sources

Sources of Flooding • Fact Sheets provided to local influencers and media outlets help outline localized messaging about flood risks

Combating Misconceptions • Combating Misconceptions • Messaging around misconceptions such as: • Flood Insurance is too expensive • Homeowners insurance does cover flooding • How much damage a couple of inches of floodwater can cause in terms of cost • I don’t qualify/can’t get flood insurance • I don’t live near the water • Tools such as: • Premium Estimator • Co-op ads for agents to help combat misconception • Commercials that speak directly to the misconceptions most people have

Consequence Messaging Consequences • Messages such as: • Two inches of water can leave you knee deep in debt • A flood can cost more than you think • Tools such as: • Online Cost of Flooding tool • Ads showcasing the real life cost of a flood • Receipt samples of repair costs to accompany mailers

Consequence Messaging • “Use innovative ways to get people talking about preparedness actions with others” - Dennis S. Mileti

Relevant Triggers • Seasonality: Hurricane Season Outreach • Hurricane Season IS Flood Season messaging to urge consumers to protect themselves from flooding during hurricane season • Created a "hurricane season countdown clock" widget tool for agent and stakeholder websites which reminds their visitors just how much time they have to get ready for the upcoming Hurricane Season.

What is the application process for becoming a certified Adjuster? The application form and information about the process and requirements are located on FEMA's Adjuster Participation in the NFIP page. For additional details regarding application submission and processing, please refer to the NFIP iServices page.

How can I get a current year ID card? For assistance with your ID card or certification application, contact NFIP iServices at iService_Claims@ostglobal.com or (301)386-6356. I have forgotten my FCN (Flood Certification Number). Contact the NFIP iServices help desk at iService_Claims@ostglobal.com or (301)386-6356.

WWW.FEMA.GOV NFIP Regional Offices FEMA Regional Offices NFIP Web site Tele-registration Disaster Hotline Where to get help?

FEMA is engaged in a comprehensive effort to address the concerns of the wide array of stakeholders involved in an ongoing dialog about the National Flood Insurance Program (NFIP). The initiative is a multi-staged process designed to engage stakeholders and consider the largest breadth of public policy options. FEMA believes this important process will ensure the program can efficiently and effectively meet the needs of the public. The results of this analysis will inform decisions regarding the future of the NFIP.

What process will FEMA use in this analysis?

Will FEMA engage stakeholders through this process?

NFIP Listening Session Available from FEMA website at: http://www.fema.gov/business/nfip/nfip_listening_session.shtm

Congress What’s next for the NFIP? Stay tuned.