Download

1 / 6

70 likes | 208 Views

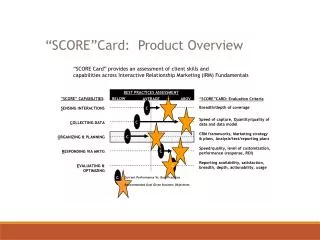

chfa risk information score card (chfa risc). Presented by: Karen Harkin 303.297.7327. purpose of chfa risc. Allow CHFA to continue to serve applicants from 580 through 619 and loans that have to be manually underwritten

E N D

chfa risk information score card (chfa risc) Presented by: Karen Harkin303.297.7327

purpose of chfarisc • Allow CHFA to continue to serve applicants from580 through 619 and loans that have to bemanually underwritten • Allow CHFA to serve applicants from 620 through 659 with DTI’s in excess of 43.0% • Help applicants, who do not meet CHFA requirements at this time, understand the issuesthey need to address to improve their readiness to purchase a home

use chfarisc for any loan where you have • An applicant who has a credit score of 580 through 619 • To manually underwrite the loan • An applicant who has a credit score of 620 through 659 with a DTI in excess of 43.0%

stops - applicants who • Have credit scores from 580 through 619and a DTI in excess of 43.0% • Have a manual underwritten loan DTI in excess of 43.0% • Have credit scores from 620 through 659, a DTI in excess of 43.0% and can’t pass RISC • Late payments on Mortgage or Rentin last 12 months • Non-medical collections within most recent 12 months(unless totaling less than $100) • Non-medical collections in excess of $2,000 totalin 13-24 months – even if paid