Download

1 / 41

410 likes | 423 Views

This chapter covers topics such as calculating percent of change, simple and compound interest, and consumer loans. It includes examples and practice problems.

E N D

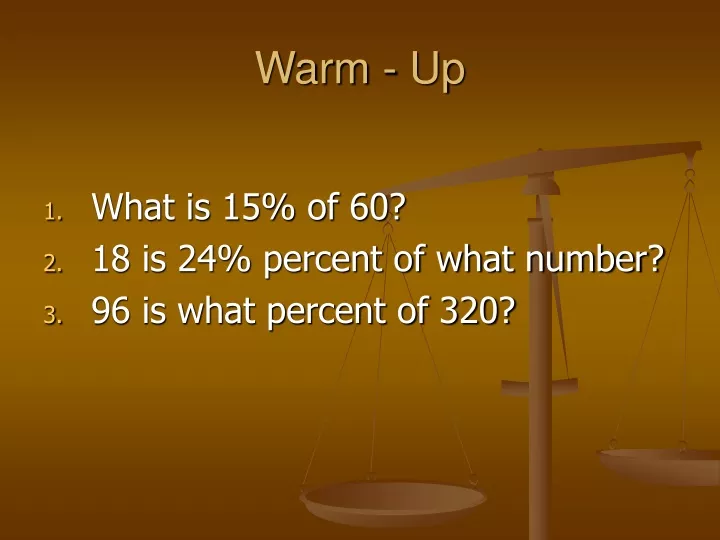

Warm - Up • What is 15% of 60? • 18 is 24% percent of what number? • 96 is what percent of 320?

Consumer MathematicsChapter 11 Percent of Change Simple Interest Compound Interest Consumer Loans

Lesson 11.1: Percent • The school district receives funds from several sources. The 2008 – 2009 budget is $442,300,000. The federal government contributes $33,500,000 of that amount. What percent does the federal government contribute to the school district’s budget?

Percent of Change • A+ University has decided to raise tuition from $7,965 to $8,435 for next year. What is the percent of increase in the tuition?

Honest Abe’s Auto • Abe’s auto is having a blow-out sell. Abe advertises that all cars are sold at 5% markup over the dealer’s cost. Abe has a new pinto for sale for $18,970. On the internet you find out that the dealer cost on this model is $17,500. Is Abe being honest in his advertising?

Music sales • Jamin’ Jude Records reported that music downloads increased 28.24% from 2005 to 2006. If the number of downloads for 2006 were 524,785 how many downloads were there in 2005?

Lesson 11.2: Interest • Simple Interest: I = Prt I – interest earned, P – principal, r – interest rate, t – time (years) • Future value: A = P(1 + rt) A – future value, P – principal, r – annual interest rate, t – time in years

Solve. • If you deposit $200 in a savings account paying 6% annual interest, how much interest will be earned if you leave it there for 5 years? • If you deposit $500 paying 4.5% annual interest, how much money will you have in 3 years?

Solve. • Assume that you plan to save $1000 over 2 years to put down on a car. Your bank offers a certificate of deposit (CD) that pays 3% annual interest computed using simple interest. How much must you put in this CD now in order to have the desired $1000 in 2 years?

Warm-Up • Due to a slump in the economy, Anna’s mutual fund has dropped by 12% from last quarter to this quarter. If her fund is now worth $11,264, how much was her fund worth last quarter? • How much must you deposit in an account paying 8% annual interest computed using the simple interest formula if you earn $800 in 2 years?

You plan to take a trip to the Grand Canyon in 2 years. You wish to buy a certificate of deposit for $1,200 that you will cash in for your trip. What annual interest rate must you obtain on the certificate if you need $1,500 for your trip?

Compound Interest • Let’s say you get $250 for your birthday and you decide to deposit the money in a savings account that earns 6% interest compounded annually. How much money would you have in 3 years? End of year 1: 250(1 + .06(1)) = $265 End of year 2: 265(1.06) = $280.90 End of year 3: 280.90(1.06) = $297.75

What if you left the money in for 15 years? A = 250(1.06)15 = $599.14 • So what if the bank compounded the interest quarterly instead of annually?

Compound Interest Formula n – n time periods per year Compounded quarterly for 3 years: Compounded quarterly for 15 years:

Selecting the best choice: • Your rich Auntie Clause has passed away and bequeathed you $20,000. Because you are cautious with your investments, you decide to buy a 5-yr CD to save for the future. Prudent Savings & Loan has a CD with a yearly interest rate of 5% compounded quarterly, whereas First Friendly National Bank has a CD with a rate of 4.8% compounded monthly. Which institution gives you the best return on your money?

Saving for college • Jack and Jill just gave birth to Jackill, their son. They decide to make a deposit into a taxfree account to use later for Jackill’s college education. The account has an annual interest rate of 8% compoundedquarterly. How much must they invest now so that Jackill will have $50,000 at age eighteen?

Warm-Up • Cameron finds herself in a bind and is willing to make a deal. She found the perfect prom dress but it costs $550!!! Mr. Ike is willing to loan her the money with the condition that she pay it back in 6 months at payments of $100. What interest rate would Mr. Ike be earning on his money? 18.2%

Decide which is the better investment: • 7% compounded yearly or • 6.8% compounded monthly B • If you invested $500 earning 4.5% interest compounded quarterly, how much money would you have after 20 years? $1,223.64

Using the log function to solve for nt • Exponent Property of the Log Function: William wants to buy his partners’ half of their game business, Pawnisher’s. Laney and Erica have agreed to sell for $3,000. William presently has $2,700 and found an investment that will pay him 9% annual interest compounded monthly. In how many months will William be able to buy his partners out?

William will have the money he needs at the end of the 15th month.

Finding the interest rate • A foundation wants to create a scholarship for a deserving student in which the scholarship amount of $500 would come from the interest earned on a scholarshipfund. The foundation has $1,200 in the fund and want to find an annual interest rate that is compounded monthly. What rate of interest would they need in order to have the $500 for the scholarship in 4 years?

p.633 #’s 1-3, 7, 11, 15-16, 20, 30, 40, 43, 51, 79

11.3 Consumer Loans • Closed-ended credit/ installment loans – loans having a fixed number of equal payments. (furniture, appliances) • Open-ended credit – loans where even though you are making payments you may also be increasing the loan by making further purchases. No set number of payments. (Department Store charge accounts, Credit cards)

Installment Loan • Often called the add-on interest method

Ben buys $2800 worth of furniture. He pays $400 down and agrees to pay the balance at 6% add-on interest for 2 years. Find a) the total amount to be repaid and b) the monthly payment. Solution Amount to be repaid = P(1 + rt) = $2400(1 + (.06)2) = $2688

b) Monthly payment = $2688/24 = $112 24 payments • Even though the simple interest is easy to compute with the add-on interest method, the actual interest you are paying on the outstanding balance is higher than the stated interest rate. Think about it.

Warm-Up/Classwork • p.635 #’s 55, 56, 59, 60, 63 • p.643 # 9

Credit cards & Open-ended credit • The unpaid balance method computes finance charges (interest) on the balance at the end of the previous month. • This method also uses the simple interest formula I=Prt, however, P=previous month’s balance + finance charge + purchases made – returns – payments R is the annual interest rate and t = 1/12

Example: Unpaid Balance Method • The table shows a VISA account activity for a 2-month period. If the bank charges an apr of 18% annually with the interest calculated on the unpaid balance each month, find the missing quantities in the table.

Solution Unpaid balance times (.18)(1/12) or .015

Your Turn • p.644 # 17

Finance Charge/Unpaid Balance Method • Most open-end lenders use a method of calculating finance charges called the average daily balance method. It considers balances on all days of the billing period and comes closer to charging card holders for credit they actually utilize.

The Average Daily Balance Method • Add the outstanding balance for your account for each day of the previous month. • Divide the total in step 1 by the number of days in the previous month to find the average daily balance. • To find the finance charge, use I = Prt, where P is the avg. daily balance, r is the annual interest rate, and t is the number of days in the previous month divided by 365.

Example: Average Daily Balance The activity on a credit card account for one billing period is given on the next slide. If the previous balance was $320.75, and the bank charges 16.8% annually, find the average daily balance for the next billing (April 3) and the finance charge for the April 3 billing using the average daily balance method.

Example: Average Daily Balance • March 3 Billing date • March 12 Payment $250.00 • March 17 Car repairs $422.85 • March 20 Food $124.80 • April 1 Clothes $64.32

Solution • First we make a table of the running balance

Find the sum of the daily balances by adding the last column = $13507.54. Finance charge = ($435.73)(.168)(31/365) = $6.22.

Your Turn • p.644 # 23

Lesson 11.3 p.643 #’s 3, 6, 10, 13, 14, 20, 21, 25