Download

1 / 32

320 likes | 406 Views

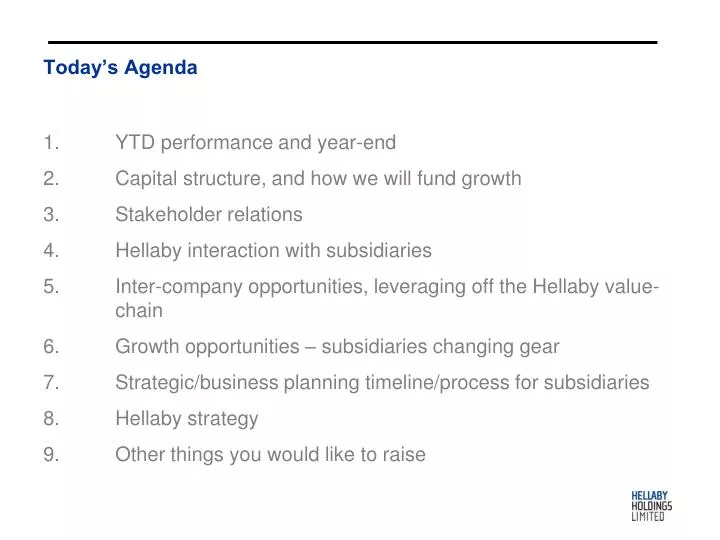

Today’s Agenda . YTD performance and year-end Capital structure, and how we will fund growth Stakeholder relations Hellaby interaction with subsidiaries Inter-company opportunities, leveraging off the Hellaby value- chain Growth opportunities – subsidiaries changing gear

E N D

Today’s Agenda • YTD performance and year-end • Capital structure, and how we will fund growth • Stakeholder relations • Hellaby interaction with subsidiaries • Inter-company opportunities, leveraging off the Hellaby value- chain • Growth opportunities – subsidiaries changing gear • Strategic/business planning timeline/process for subsidiaries • Hellaby strategy 9. Other things you would like to raise

Westpac Debt Hellaby – stated maximum gearing ratio 45% (Debt : Debt + Equity)

Westpac Banking Covenants ICC target > 2.5 (EBIT : Funding Costs) Debt cover target < 3.0 (Total Debt : EBITDA)

Project Acorn • 3 : 7 pro-rata renounceable rights issue • $1.30 issue price • Interest expense saving in FY2011 $950k • Underwriting - Castle • - Forsyth Barr • - Sub-underwriters • Outcome • Raised $28.4 million (less costs) • Rights traded at 50 cents • Oversubscriptions facility • 3,570 (46.4%) of 7,700 shareholders took up entitlement • 19.1 million (87.3%) of 21.8 million rights were taken up (prior to oversubscriptions)

Capital Notes 5 year subordinated capital notes created 18 May 2006, maturing 15 June 2011 8.50% coupon rate, paid quarterly in arrears Funded BBQ Factory ! 1,300 note holders Advised market did not intend converting to shares 7 July 2010 Rationale for redeeming / options Interest expense saving in FY 2011 $950k

Capital structure and how we will fund growth • Working capital – still the cheapest option • Bank debt – have significant headroom in existing facilities and covenants • Equity raising - Project Acorn very successful - could raise $20m -$25m any time in next 6-24 months • Alternatives include placement, rights issue, SDP, combination • Senior bonds or other instrument – capital notes repaid on 15 December 2010

Stakeholder relations Significant management focus Rebuilding investor confidence share price and funding flexibility More proactive communication of ‘Hellaby story’, performance and strategy Total shareholder return (TSR) superior to NZX50 TSR up 39.5% last year; up 40% YTD

Spread of Hellaby Shareholders • Average shareholding 9,441 (excluding Castle average is 6,566) • Minimum holding per NZX is 200 shares • 279 shareholders holding 30,660 shares - minimum holding

Dividends • Previous approach to paying dividends • Current policy to pay 50% of NPAT, imputed where able • 5 cps dividend payable 12 November 2010 • Interim dividends Dividend History

Dividend Reinvestment Plan Introduced March 2006 Strike price = VWAP – dividend – 5% discount 30 – 35% uptake Castle pro-rata participation

Hellaby interaction with subsidiaries Statement of Intent good reference point Respective Hellaby roles Effectiveness of monthly reviews Growth now a key agenda item What can Hellaby do better or differently with subsidiaries? Talent development programme

Intercompany opportunities, leveraging off the Hellaby value-chain

Intercompany opportunities How do I organically grow my business? - Customer clusters How do I grow Hellaby business ? - Opportunities identified Think services as well as customers !

Executing profitable growth – ‘changing gear’ Hellaby very serious about profitable growth Arguably bigger challenge for CEOs than turnaround Subsidiaries must compete for capital, justify projects and expenditures, obtain buy-in for strategy and direction Is your business committed to driving profitable growth? will revenues therefore exceed budget? Do you each have a clear plan?

Strategic / business planning timeline / process for subsidiaries

Business Planning Review • New process in Hellaby – moving from “panel beating” to “growth” • Part of strategic framework agreed with Board • Timing • Info request / topics for discussion to CEO’s by mid December • Workshop with each CEO and relevant senior team members first half of February • Market assessment in put into early budgeting process • Strategic options (as relevant) into budgeting process by late April • Resourcing • Lead by Greg • Support from John, Neil and Richard • Looking for growth Subsidiary EBITDA $50m in FY2012

Business Planning Review • Overview of process • Start with assessment of market environment • Build assessment of each subsidiary’s: • Environment • Competitive forces • Industry structure • Opportunities and threats • Capability Strategic position • Identify and evaluate options • Implementation • Review and repeat update 12 monthly • Deliberate strategy and superb execution = superior returns

Hellaby strategy – ‘buy build harvest’ • Strategic framework development – two distinct investment portfolios • Core investment portfolio specialised ‘core’ sectors / divisions sectors may migrate over time ultimately trans-Tasman • Generator Fund • Expansion capital portfolio • Co-investor partnerships in strong SMEs • Agnostic about investment sectors • Portfolio will change over next 3-5 years

Risk Framework Stage 1 D Lucas Exercise (Complete 2009/10) • Identify risks • Assess the risk value • Matrix Stage 2 Quantate (Start Oct 10) • Set up Quantate from the D Lucas exercise • Handover with basic definitions and training given (Nov & Dec 10) • Subsidiaries to complete their set up and to review risks uploaded into Quantate • Board report limited to matrix and a description of the top risks (with the first report due 14th February 2011 & the second on the 13th May 2011) Stage 3 Expand Risk Management (Start at the Finance Workshop) • Add mitigating controls • New Board report developed (due with July 10th day reporting, and quarterly thereafter)