Download

1 / 22

300 likes | 699 Views

The Logic of the Budget Process. A Budget is a Spending PLAN. The Size and Growth of Government Expenditure. Government purchases (stuff) Transfer payments (Social Security) Government spending (all governments) is about a third of the GDP Not too bad compared with other countries.

E N D

The Size and Growth of Government Expenditure • Government purchases (stuff) • Transfer payments (Social Security) • Government spending (all governments) is about a third of the GDP • Not too bad compared with other countries

Budget Process & Logic • Different from the private sector • No price or profit signals to go by • Public goods are difficult to sell • No profits/bottom line to measure • Limited by resource constraints • More customers is not necessarily better • Mixed, sometimes competing motives

The Parts of the Public Expenditure/Public Revenue Process • Who should pay for things? • How much should be borrowed? • The budget: • Elaborates executive-branch intentions • Provides for legislative review and approval • Provides control of implementation

Multiple Budgets • The budget year • The plan for the next budget year • The progress-report year • Current budget in execution • The final report year • The most recently fully-completed budget • Outyears • Future budgets beyond the one being requested

Fiscal Year • Pronounced “FISS-KUL” (NOT physical) • Federal FY runs from 1 Oct thru 30 Sep • Some states and cities different • Named by the year in which the FY ENDS (FY 2009 goes from Oct 2008-Sep 2009)

Functions of the Budget Process • Fiscal discipline and control • Response to strategic priorities • Efficient implementation of the budget

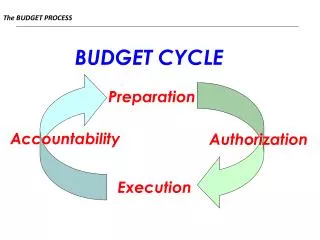

4 Phases of the Budget Cycle • Executive Preparation • Agency requests, ceilings, forecasts, justification, strategy, promises • Legislative Consideration • Subcommittees, appropriations, bi-cameral approval, conference, veto • Execution • Appropriations spent, services delivered, spend-down, carry-over, budget base • Audit and Evaluation • GAO, financial or performance audits

Authorization v Appropriation • Authorization - what the executive is allowed to spend • Appropriation – what the executive is actually given to spend

Governmental Accounting & Financial Reporting • Standards • Financial Accounting Standards Board (FASB-private) • Government Accounting Standards Board (GASB-govt)

Governmental Accounting & Financial Reporting • Elements of an accounting system • Source documents • Receipts, invoices • Journals • Chronological summary of transactions • Ledgers • Reports of revenue, expense, or balance in an account • Procedures & controls • Forms, instructions, policies

Governmental Accounting & Financial Reporting • Funds • Governmental Funds • General fund (e.g., treasury) • Special revenue funds (e.g., transportation trust fund) • Debt service funds (e.g., bond repayment) • Capital projects funds (e.g., new tunnel) • Permanent fund (e.g. a trust fund) • Proprietary Funds • Enterprise fund (e.g., water, utilities) • Internal service fund (e.g., motor vehicle maintenance, GSA) • Fiduciary Funds (e.g., pension funds)

Governmental Accounting & Financial Reporting • Accounting basis (the method of matching revenues and expenditures over time) • CASH BASIS • Records money inflow when received, expenditure when cash payment completed • FULL ACCRUAL BASIS • Revenue recorded when earned, expenses recorded when liability incurred • MODIFIED ACCRUAL • Expenditure recorded when liability incurred, revenue recorded when cash received

Governmental Accounting & Financial Reporting • Comprehensive Annual Report (CAFR) • Introductory section, financial section, statistical section

Budgets & Political Strategies • The Incremental Insight (reality) • Importance of the budget base • Politics and compromise • The Comprehensive Insight (abstract) • Bottom up review, annual analysis

Roles, Visions, and Incentives • Operating agency’s view • Chief executive’s view • Legislature’s view

Strategies • Strategies for a proposed reduction in the base • Propose a study • Cut popular programs • Dire consequences • All or nothing • You pick • We are the experts

Strategies • Strategies to continue an existing program • Round up • “if it don’t run, chrome it” • Sprinkling • Numbers game • Workload and backlog • The accounting trap

Strategies • Strategies to propose a new program • Old stuff • Foot-in-the-door financing • It pays for itself • Spend to save • Crisis • Mislabeling • What they did makes us do it • Mandates • Matching the competition • It’s so small

Politics, Representation, and Government Finance • Some people are more politically important than others • Specialists appear • Imperfect information results in bribery • Voters make uninformed choices

Conclusion • Budgets are reality…everything else is just talk! • Budgets allocate public resources • Four phases of the budget cycle (executive preparation, legislative, execution, audit and evaluation • Political and incremental