Download

1 / 11

110 likes | 128 Views

Learn how to adjust work sheet entries to update general ledger accounts at the end of a fiscal period for accurate financial statements. Understand concepts like expenses matching revenue and adjustments for accounts such as Prepaid Insurance and Supplies. Follow step-by-step tutorials with examples.

E N D

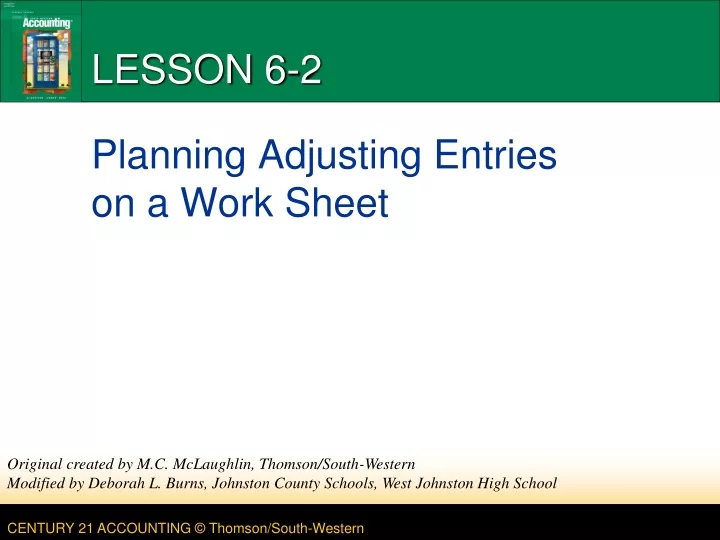

LESSON 6-2 Planning Adjusting Entries on a Work Sheet Original created by M.C. McLaughlin, Thomson/South-Western Modified by Deborah L. Burns, Johnston County Schools, West Johnston High School

Planning Adjusting Entries on a Work Sheet • Changes recorded on a work sheet to update general ledger accounts at the end of a fiscal period are called adjustments • In order to give accurate information on financial statements, some general ledger accounts must be brought up to date at the end of a fiscal period. • The accounting concept matching expenses with revenue is applied when revenue from business activities and expenses associated with earning that revenue are recorded in the same accounting period. LESSON 6-2

Planning Adjusting Entries on a Work Sheet • In order to give accurate information on financial statement, some general ledger accounts must be brought up to date at the end of a fiscal period. • Adjustments are made in the adjustments column of the worksheet. • Examples of accounts that might need to be adjusted at the end of a fiscal period: • Prepaid Insurance • Supplies • Depreciation LESSON 6-2

3 SUPPLIES ADJUSTMENT ON A WORK SHEET page 158 On August 31, Ms. Park counted the supplies on hand & found that the value of supplies still unused on that date was $310.00. The balance of the Supplies account in the General Ledger is $1,025.00. 2 1 1. Write the debit amount. 3. Label the two parts of this adjustment. 2. Write the credit amount. LESSON 6-2

3 PREPAID INSURANCE ADJUSTMENT ON A WORK SHEET page 159 On August 31, Ms. Park checked the insurance records & found that the value of insurance coverage remaining was $1,100.00. The balance of the Prepaid Insurance account in the General Ledger is $1,200.00. 2 1 1. Write the debit amount. 3. Label the two parts of this adjustment. 2. Write the credit amount. LESSON 6-2

1 2 3 PROVING THE ADJUSTMENTS COLUMNS OF A WORK SHEET page 160 After all adjustments are recorded in a worksheet’s Adjustments columns, the equality of debits & credits for the two columns is proved by totaling & ruling the two columns 1. Rule a single line. 2. Add both the Adjustments Debit and Credit columns. Write each column’s total. 3. Rule double lines. LESSON 6-2

PREPARING A WORK SHEET page 160 C 1. Write the heading. 2. Record the trial balance. 3. Record the supplies adjustment. 4. Record the prepaid insurance adjustment. 5. Prove the Adjustments columns. 6. Extend all balance sheet account balances. 7. Extend all income statement account balances. 8. Calculate and record the net income (or net loss). 9. Total and rule the Income Statement and Balance Sheet columns. LESSON 6-2

1 LESSON 6-2

496400 10000 15000 496400 10000 15000 6 10000 102500 120000 10000 31000 110000 (a) 71500 (b) 10000 20000 5000 500000 20000 5000 500000 3 62500 4 62500 356500 356500 21300 21300 (b) 10000 10000 2800 30000 7 2800 30000 (a) 71500 5 71500 11000 11000 8 9 1 2 881500 881500 81500 81500 146600 356500 734900 525000 Net Income 209900 209900 356500 356500 734900 734900 LESSON 6-2

TERM REVIEW page 161 • adjustments LESSON 6-2