Download

1 / 8

0 likes | 6 Views

Itu2019s a beautiful thing to look forward to the childrenu2019s future, and education planning can become increasingly important. In Canada, we have the Registered Education Savings Plan (RESP), which provides incentives for saving towards education through government grants, as well as special tax benefits that complement this program.

E N D

How are RESP Withdrawals Taxed? Sit Dolor Amet How are RESP Withdrawals Taxed?

Introduction It’s a beautiful thing to look forward to the children’s future, and education planning can become increasingly important. Knowledge of available savings tools is how you get ahead. In Canada, we have the Registered Education Savings Plan (RESP), which provides incentives for saving towards education through government grants, as well as special tax benefits that complement this program. However, it is crucial to understand how withdrawals from those plans are taxed because you shouldn’t let it surprise you during tax time.

Introduction to RESP The RESP (Registered Education Savings Plan) is a special type of savings account that’s designed to help Canadian parents, grandparents, etc., save money for their children’s post-secondary education. The attractive part about this plan is that the government helps you with the expenses by adding grants and bond payments, providing an additional cash flow into your RESP account. Before I tell you about tax on withdrawals from RESP, it’s important to know some of the basic “RESP Rules and Contribution Limits “because these will impact on your taxes.

RESP Rules and Contribution Limits RESPs come with their own set of rules for contributions and how interest or income is accumulated within the account. For example, the lifetime contribution limit for an RESP is $50,000 per beneficiary. There is no annual limit on RESP contributions; however, the Canada Education Savings Grant (CESG) will only be paid for the first $2,500 contributed annually per beneficiary. These limits come into play when you withdraw funds from an RESP and are subject to individual and CESG repayment rules.

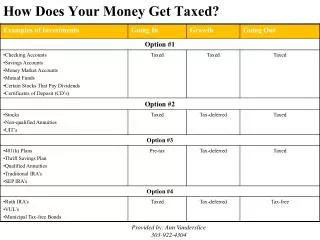

Taxation of RESP Withdrawals Withdrawals from an RESP can be categorized into two types: Post-Secondary Education (PSE) withdrawals and Educational Assistance Payments (EAPs). Both types of withdrawals have different tax implications, which are crucial for savers to understand. • Post-Secondary Education (PSE) Withdrawals: PSE withdrawals refer to the portion of the RESP that consists of the principal amount contributed by the subscribers. These funds are not subject to tax when withdrawn, regardless of whether the subscriber or the beneficiary receives them. This is because these contributions were made with after-tax dollars, meaning they were already taxed prior to being deposited into the RESP. • Educational Assistance Payments (EAPs): EAPs include the growth of the investments within the RESP as well as any government grants and bonds — namely the CESG, Canada Learning Bond (CLB), and any provincial grants. EAPs are taxable upon withdrawal but are included in the income of the student (the beneficiary of the RESP) for tax purposes. This is where the tax efficiency of RESPs truly comes to light, as most students typically have lower incomes and can benefit from various tax credits, thus often paying little to no tax on these withdrawals.

Managing RESP Withdrawals Strategically Understanding the taxation rules of RESP withdrawals can lead to more strategic decision-making when it comes time to use these funds. Here are some strategies to consider: • Timing of Withdrawals: Since EAPs are taxed in the year they are withdrawn, consider the student’s expected income each year to minimize taxes. If a student expects a higher income in certain years, it might be advantageous to withdraw less during those years. • Maximize Free Money: Always aim to maximize government contributions through the CESG by contributing at least $2,500 annually to the RESP.

RESP Quotes and Advice Getting advice that’s specific and personalized is important, though. Getting a “RESP Quote” from financial advisors, or institutions can provide you with information about the best strategies for putting money into RESP accounts and taking it out again and give you some ideas about what kinds of investments could be best for your particular economic circumstances and level of risk tolerance.

The Final Verdict The tax rules for RESP withdrawals in Canada are set up to benefit the beneficiary, a student who usually has little or no income while studying. By planning your withdrawals and understanding the impact of both PSE withdrawals and EAPs, families can ensure they receive the maximum benefits from a RESP Langley BC. Of course, contact Navalta Protection Personal Corporation’s financial advisor to help you decide what amounts to withdraw depending on your individual financial situation.