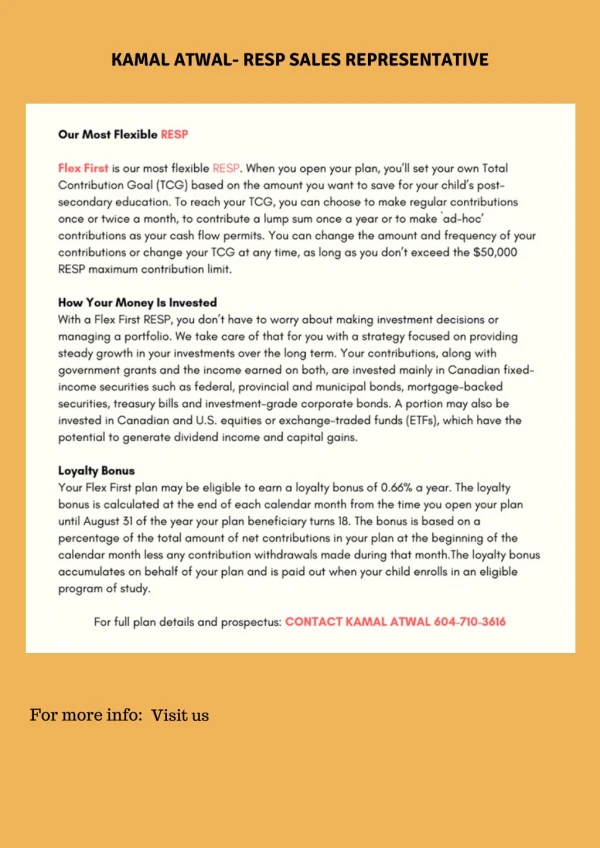

Download

1 / 8

0 likes | 10 Views

When deciding between an individual or a family RESP, however, it would be only after understanding the differences, benefits, and limitations that one would consider placing a child in an individual RESP. In this blog, the elements of both individual and family RESP are discussed to help you make a worthwhile decision.

E N D

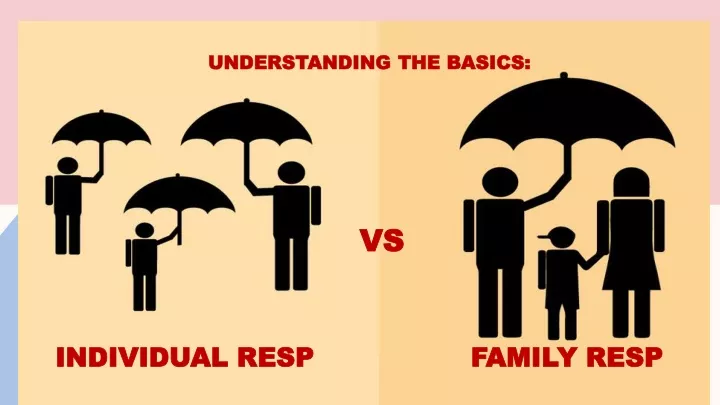

Understanding the Basics: vs Individual RESP Family RESP

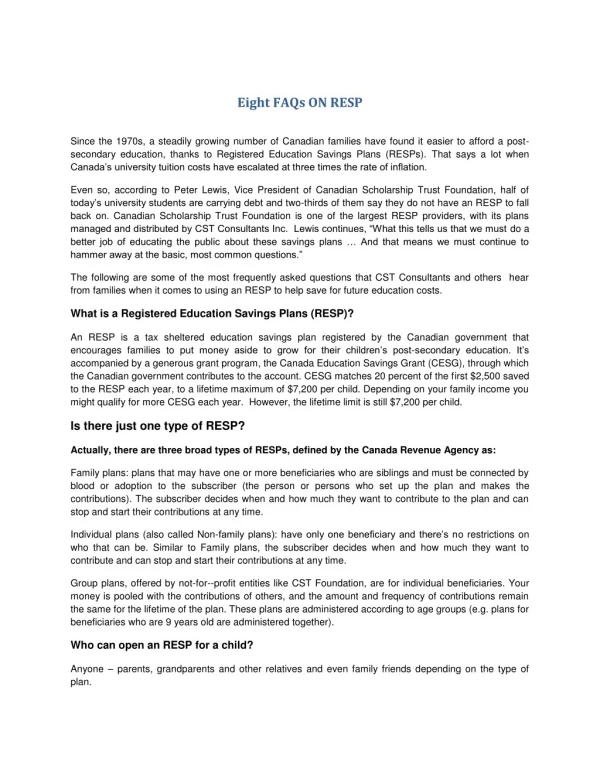

What is a Registered Education Savings Plan? Establishing a Registered Education Savings Plan is a smart way to save and make it financially easier for you when sending your child to college. When deciding between an individual or a family RESP, however, it would be only after understanding the differences, benefits, and limitations that one would consider placing a child in an individual RESP. In this blog, the elements of both individual and family RESP are discussed to help you make a worthwhile decision. An RESP is a tax-advance savings plan that allows parents, relatives, or friends to save money toward the post-secondary education of a child. The Canadian government helps these savings efforts through grants and bonds that will let a Registered Education Savings Plan grow, therefore making this a very good option for funding education in the future.

Individual RESP Definition and Eligibility: An individual RESP is an account set up for one beneficiary. Anybody may open an individual RESP for any child, irrespective of the relationship. This makes it very popular with those people who would want to contribute to a child's education but are not related, like godparents or family friends. Contributions and Limits: As with every other RESP, the contributions that are made to an individual plan are not tax-deductible, but the investment growth is tax-deferred until it is withdrawn. The lifetime contribution limit per beneficiary is $50,000, and such contribution qualifies for the CESG of the government, under which it adds 20% to the initial $2,500 contribution annually.

Individual RESP PROs & COns Advantages: • Flexibility: Individual RESPs are incredibly flexible when it comes to who can open one and for whom. • Simple Management: Managing an individual RESP is straightforward since it involves only one beneficiary. Disadvantages: • Limited to One Beneficiary:If the beneficiary decides not to pursue higher education, reallocating the funds to another child involves opening a new RESP or undergoing a transfer process, which might complicate the grant allocation.

Family RESP Definition and Eligibility: A family RESP allows subscribers to save for multiple children within one plan. However, all beneficiaries in a family RESP must be related to the subscriber by blood or adoption, and they must be under 21 years old when they are named as beneficiaries. Contributions and Limits: The contribution limits and rules for a family RESP are similar to those of an individual RESP, including the $50,000 lifetime limit per child and eligibility for the CESG. However, the total contribution is shared among all beneficiaries, which can be an efficient way to manage savings if you have more than one child.

Family RESP PROs & COns Advantages: • Cost-Effective: A family plan is cost-effective and easier to manage with one set of fees and one account for multiple children. • Flexibility in Allocation: Funds can be allocated as needed among the beneficiaries, which is particularly beneficial if one child does not use the full amount for their education. Disadvantages: • Restricted Eligibility: Only siblings can share a family RESP, limiting its utility for those looking to save for children who are not siblings. • Complex Withdrawals: Withdrawals must be carefully managed to ensure they are distributed fairly among the beneficiaries, according to their educational needs.

Choosing Between Individual and Family RESPs When deciding between an individual and a family RESP, consider the following factors: • Number of Children: If you have more than one child and they are siblings, then you can instead consider the family RESP to be more advantageous; otherwise, for non-siblings, separate individual RESPs should be made. • Relationship to the Beneficiaries: Family RESPs are restricted to siblings related by blood or adoption, while individual RESPs have no such restriction. • Future Uncertainties: Not every child may go on to post-secondary education. The family RESP allows the money to be reallocated to siblings; individual RESPs are not as flexible when one beneficiary decides not to pursue an education.

Final Thoughts Individual and family RESPs are the two most valuable instruments for saving for a child's education in Canada. Knowing what each type of plan is about better orients you toward the ideal way to save according to your family situation and finances. Whichever path is chosen, opening an RESP is the smart movethat will help lessen those financial burdens brought on by higher education. You can definitely see a financial advisor who can give you specific tips on how to maximize your education savings and get specific advice and the best possible RESP quotes for your situation. Be it a family plan that will cover all your children or individual plans catering to specific needs, a Registered Education Savings Plan in Canada is one of the ways that offers peace of mind about your child's academic future.