Download

1 / 35

350 likes | 550 Views

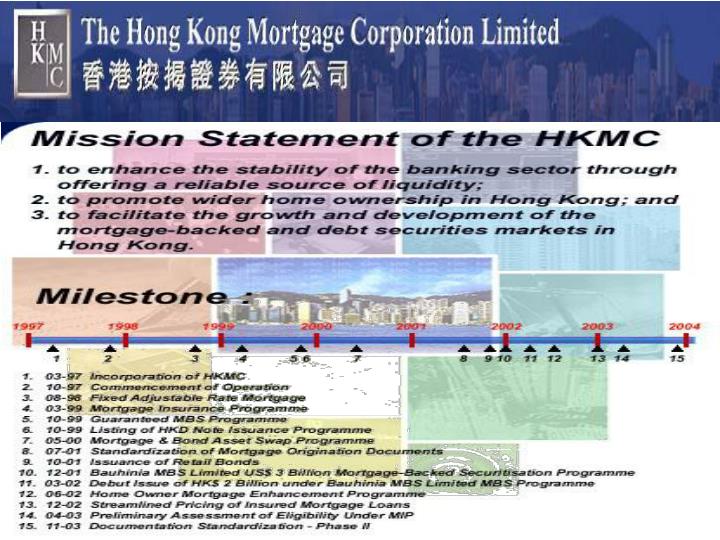

The development of Hong Kong Mortgage Corporation Limited (HKMC). Agenda. Introduction Current development Future development Conclusion MC Questions. Introduction. Background of HKMC. established in March 1997 supply of mortgage financing in Hong Kong

E N D

The development of Hong Kong Mortgage Corporation Limited (HKMC)

Agenda • Introduction • Current development • Future development • Conclusion • MC Questions

Background of HKMC • established in March 1997 • supply of mortgage financing in Hong Kong • majority of mortgage loans are in floating rate terms • not exposed to any substantial interest rate risk, but subject to other funding risks

Background of HKMC (cont.) • initial capital of HK$1 billion from the Exchange Fund • primary objective is to promote the development of the secondary mortgage market in Hong Kong • can sell their mortgage loans in the secondary market to raise liquidity

Functions of HKMC • Stability of the banking sector • Fund supply for mortgages • Promotion for the debt securities market

Mortgage-Backed Securities • 17th November 2005 • HK$1 billion MBS • Under the US$3 billion Bauhinia Mortgage-Backed Securitization Programme • Target : institutional investors • Mortgage loans : from HKHA

Mortgage-Backed Securities (cont.) • The price of the MBS issue is at par • Two classes of notes - Class A-1 notes (HK$400 million) - Class A-2 notes (HK$600 million)

Mortgage-Backed Securities (cont.) • Class A-1 notes - coupon rate : 4.73% (Fixed rate) - maturity : three years - stable return

Mortgage-Backed Securities (cont.) • Class A-2 notes - coupon rate : 1-month HIBOR+0.18% (Floating rate) - unstable investment yield

Mortgage-Backed Securities (cont.) • Both classes of notes - repay principal and interest on time • Notes rating - Standard & Poor's : AA-minus - Moody's Investors Service : Aa3

10-Year Fixed Rate Mortgage Scheme • 3rd November 2005 • Under the Corporation’s Fixed Adjustable Rate Mortgage (FARM) Programme • Mortgage loans : - fixed-rate period from 1 year to 10 years • Six participating banks

10-Year Fixed Rate Mortgage Scheme (cont.) • Extend the loan tenor - from 5 years to 10 years • Fixed-rate period: - 1, 2, 3, 5, 7 and 10 years • LTV : 95%

10-Year Fixed Rate Mortgage Scheme (cont.) • Mortgage Rate : Fixed during the period protect borrowers against any future volatility in interest rates during the entire period • End of the fixed-rate period • 2 choices: - re-fixing the mortgage rate - floating rate of Prime - 2.25% per annum

10-Year Fixed Rate Mortgage Scheme (cont.) • Long-term mortgage rates are attractive - e.g. - prime rate 7.5% - floating mortgage rate of Prime-2.25% 5.25% • Higher than the fixed mortgage rate up to 3 years offered under the special scheme

10-Year Fixed Rate Mortgage Scheme (cont.) • Triple-win situation - Homebuyers : additional choice of mortgage financing - Participating banks : procuring new mortgage businesses - HKMC : diversify the mortgage portfolio

HK$20 Billion Retail Bond Issuance Programme • Issued date: 1 August, 2005 • The issuer’s credit rating: - Moody’s: Aa3/A1 - S&P: AA-/A+ • Four series of notes issued • 17 Placing Banks to distribute the Issue to retail investors

HK$20 Billion Retail Bond Issuance Programme (cont.) • The followings are the coupons of the four series of notes:

HK$20 Billion Retail Bond Issuance Programme (cont.) • Series A and B: - Denomination: HK$50,000 - Application Price: 102% of the principal amount of the notes • Series C and D: - Denomination: US$5,000 - Application Price: 100% of the principal amount of the notes • Interest for all four series were payable semi-annually

HK$20 Billion Retail Bond Issuance Programme (cont.) • Benefits: - Provided investors to achieve a balanced investment portfolio and stable interest income - Wide distribution network to reach out effectively to retail investors

HK$20 Billion Retail Bond Issuance Programme (cont.) • Benefits: - Variety in currency, tenor and return to provide investment choices to retail investors - Established market making arrangement to facilitate transactions in the secondary market

HK$20 Billion Retail Bond IssuanceProgramme (cont.) • The issue obtained a satisfactory subscription result with a total application amount of HK$625 million

Reverse Mortgage Scheme • Home equity conversion mortgages • Instead of making regular for the loan • Receives a regular monthly installment • When dies, repossess and sell the property • Surplus → return to the homeowner's estate

Reverse Mortgage Scheme (cont.) • The feasibility is quite low • Monthly payout is relatively low ∴ not too attractive • Not too many HK people are familiar • May be launched if matures

Future Business • Continue to launch 10-year Fixed Rate Mortgage Scheme • Launch Retail Bonds Issuance Programme • Provide a better network and market-making mechanism for the retail bonds • Further develop MBS, MIP and retail bonds • Develop mortgage-based and debt securities market

Conclusion • Aim: Mortgage financing market in HK grows healthily • Continue to meet its business targets • Meet the needs of banking sectors and homeowners • Promote the development of the debt market

What is(are) the function(s) of HKMC? • Stability of the banking sector • Fund supply for mortgages • Promotion the debt securities market • All of the above

If the investors want to have a stable return, which class of note do they buy under the new issued MBS? • Class A-1 notes (fixed rate) • Class A-2 notes (floating rate) • (A) & (B) • None of the above

What is(are) the triple-win situation(s) of the 10 years Fixed-rate Mortgage Scheme? • provides an additional choice of mortgage financing • provides an effective avenue for procuring new mortgage businesses • diversify the mortgage portfolio • All of the above