Download

1 / 31

310 likes | 323 Views

Discover how modern nonexpected utility theories and tools from experimental economics can revive the classical utility concept. This study challenges traditional views and offers a new perspective on utility measurement in economics.

E N D

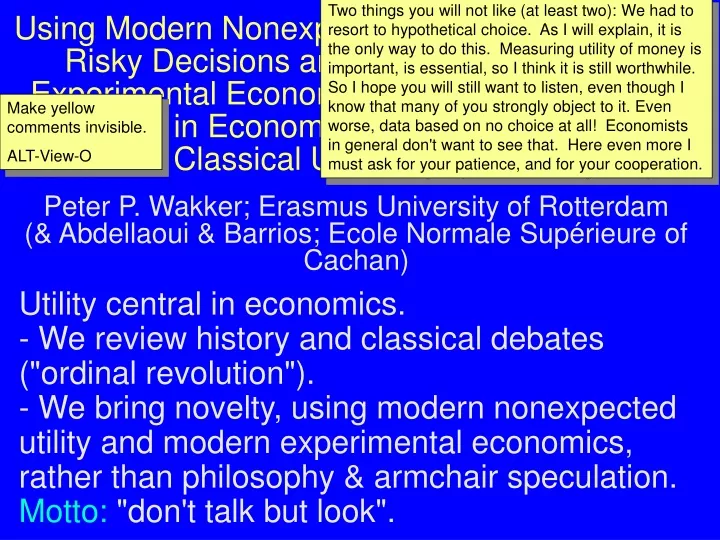

Two things you will not like (at least two): We had to resort to hypothetical choice. As I will explain, it is the only way to do this. Measuring utility of money is important, is essential, so I think it is still worthwhile. So I hope you will still want to listen, even though I know that many of you strongly object to it. Even worse, data based on no choice at all! Economists in general don't want to see that. Here even more I must ask for your patience, and for your cooperation. Using Modern Nonexpected Utility Theories for Risky Decisions and Modern Tools from Experimental Economics to Revisit Classical Debates in Economics, and to Restore the Classical Utility Concept Make yellow comments invisible. ALT-View-O Peter P. Wakker; Erasmus University of Rotterdam(& Abdellaoui & Barrios; Ecole Normale Supérieure of Cachan) Utility central in economics. - We review history and classical debates ("ordinal revolution"). - We bring novelty, using modern nonexpected utility and modern experimental economics, rather than philosophy & armchair speculation. Motto: "don't talk but look".

2 Our purpose: Show that choiceless inputs can be useful in economics; revival of old cardinal utility … Many others have pleaded for it in the past and in the present. Special aspect of our plea: Not ad hoc. Not just going back to Bentham. Rather: Link choiceless inputs to revealed preference. Build on,reinforce, revealed preference.Don't abandon it. Novelty is not in use of choiceless inputs for economic questions. That's often done by applied people, for instance in health economics. Not unfounded.

3 1. History of Utility 18th century • 1st appearance of utility:Cramer (1728), Bernoulli (1738) • 1st thorough analysis:Bentham (1789); Skip details of history and go immediately to ordinal revolution, saying only that people took utility intuitively. Utility “intuitive.”

4 19th century Samuelson (1947, p. 206), about such views: "To a man like Edgeworth, steeped as he was in the Utilitarian tradition, individual utility—nay social utility—was as real as his morning jam." • Utility still intuitive 1870: the marginal revolution (Jevons 1871, Menger 1871, Walras 1874) Resolved Smith's (1776) paradox of value-in-use versus value-in-exchange (e.g. the "water-diamond" paradox).

“Utility” is the heritage of Bentham and his theory of pleasures and pains. For us his word is the more acceptable, the less it is entangled with his theory. [Italics from original( Sect14, Chapter 1)] 5 1st half of 20th century Talk about observability. Be positive on ordinalism! Relate to logical positivism and Popper. Logical positivism: everything falsifiable. No metaphysics. In psychology: behaviorism. In economics: • Ordinal revolution:Pareto (1906), Hicks & Allen (1934) Tree: Say that we should distinguish two points, an empirical and a mathematical aspect, aspects that have been confused. First branch: Say this is empirical substantial aspect, important for us. 2nd is mathematical, not so central today. • Utility choice. al direct judgment abandonedBaumol 1958, Fisher 1892, Pareto 1906, Slutsky 1915 U ordinal in mathe-matical sense

6 • von Neumann-Morgenstern (1944) with their expected-utility model for risky decisions: • New hope for cardinal utility? • General consensus: Cardinal in mathematical sense, not empirical neoclassical; vNM-U only for risk; not for welfare evaluations etc. • Cardinal utility exists in subfields(risky, welfare, taxation, temporal)but strictly kept there. • Ordinal view dominates.(So, no meaning for utility differences.) Most economists believe that marginal utility is: 1. nonexistentand also 2. diminishing.

7 First there were positive results and hope for ordinalism: • Hicks & Allen (1934): Market phenomena only need ordinal utility. • Samuelson (1938), Houthakker (1950): Preference revealed from market demand. • de Finetti (1937), Savage (1954): Choice-basis of subjective beliefs. • Debreu (1959): Existence of market equilibrium. Behalve regel 1 alles overslaan.

8 History of utility after 1950: No account of it known to us. There are several accounts of history up to and including ordinal revolution (Stigler 1950, Blaug 1962 & 1997). Yet, many changes occurred since 1950. Time for an update! We think that new things are happening!

History of utility after 1950: Allais (1953) & Ellsberg (1961): > < EU 9 First-generation models didn't yet question ordinal position: nonEU. However … Arrow (1951): No good social procedure when only ordinal information. Simon (1955): Bounded rationality; satisficing. Most serious blow for ordinalism: Preference reversals (Lichtenstein & Slovic '71, Grether & Plott '79). Skip most except serious blow. Of serious blow say that this morning, Starmer gave us hope that prospect theory can still model it.

10 A new, recent, blow. Kahneman (1994, & al.) for intertemporal choice. Big irrationalities: People seemingly prefer prolongation of pain. Shows that: Often, human species cannot integrate over time. Then: No revealed preference. Better resort back to Bentham's "experienced utility."

Skip most; purpose is to show that we don't want to discuss these things! 11 Typical Questions for cardinal utility (not discussed here): • Is utility - a property of the commodity? - a property of the consumer? • - ultimate index of goodness? • index for other good things • (expected offspring …). • Is utility • If child reveals clear preference for candy over medicine, then how about utility thereof? • If two persons have different utilities, must it be due to different background/circumstances of an objective kind?

12 Experimental Economics and Utility; Plan of Paper For questions:"Do cardinal and/or ordinal utility exist?""Are they the same?" experimental economics' answer is: (Try to) measure them, and see! No philosophical contemplations here. A table organizing some utility-related phenomena, and positioning our contribution: Don't talk but look.

13 Market equilibria Risk Experienced (Kahneman) Welfare Strength of preferences Intertemporal : Relation obtained in this paper. choice-based choiceless Say on 1st appearance that choice-based in a column and ordinal utility a row. ordinal utility cardinal utility just noticeable differences; minimally perceptible thresholds Utilities within rectangles are commonly restricted to their domains. We hope to get Machina and others back to using the concept of utility. Mark Machina, Jun'02: “The word utility has too many meanings. I avoid using the word utility.” We: not more concepts, but fewer. Relate them.

They also had data where reference dependence plays a role. So where you get straight preference reversals, and by applying the CPT parameters of T&K'92, and plausible reference points, you can reconcile the inconsistencies. They also give a precise elaborated quantitative model for it; but, had no state-dependence of the reference point. 14 3. Plan of paper First, measure utility through risky decisions(choice-based). - Empirical problems for traditional EU; have frustrated utility measurements. - Can be fixed using prospect theory (Bleichrodt, Pinto, & Wakker 2001, Management Science). Next, measure utility through strength of preference; direct judgments (choiceless). Finally, compare these utilities.

15 4. The Experiment 1st utility measurement: Tradeoff (TO) method (Wakker & Deneffe 1996) Completely choice-based.

t1 200,000 ~ _ _ 2/3 2/3 (U(2000)-U(1000)) (U(2000)-U(1000)) ~ 2000 2000 1000 1000 1/3 1/3 ~ = . . . = 18, 1 curve 16 Tradeoff (TO) method (U(t1)-U(t0)) = (U(2000) - U(1000)) U(1000) + U(t1) = U(2000) + U(t0); EU 2000 1000 _ 2/3 U(t1)-U(t0)= (U(2000)-U(1000)) 1/3 6,000 5000 (=t0) = U(t2)-U(t1)= t1 t2 . . . U(t6)-U(t5)= t5 t6

t1 200,000 EU 2000 1000 _ d1 d1 d1 2/3 U(t1)-U(t0)= (U(2000)-U(1000)) ~ 1/3 12,000 5000 (=t0) = ! ? _ _ 2/3 2/3 (U(2000)-U(1000)) (U(2000)-U(1000)) U(t2)-U(t1)= ~ 2000 2000 1000 1000 d2 d2 d2 1/3 1/3 ~ t1 t2 = ? ! . . . . . . = ! ? U(t6)-U(t5)= t5 t6 21, curves; then 23, CE1/3 17 Tradeoff (TO) method Prospect theory: weighted probs (even unknown probs)

1 U 5/6 4/6 3/6 2/6 1/6 0 t3 t4 t5 $ Consequently:U(tj) = j/6. 18 Normalize:U(t0) = 0; U(t6) = 1. If I teach students, I let them draw their own utility curves in this manner. t1 t2 t0 t6

Based on direct judgment, not choice-based. 19 2nd utility measurement: Strength of Preference (SP)

20 This U just comes out of the blue. We're even using the same symbol U … Strength of Preference (SP) We assume: For which s2 is ? s2 t1 t1t0 U(s2) – U(t1) = U(t1) – U(t0) ~* For which s3 is ? s3 s2 t1t0 U(s3) – U(s2) = U(t1) – U(t0) ~* . . . . . . For which s6 is s6s5 ~* t1t0? U(s6) – U(s5) = U(t1) – U(t0)

CE2/3(PT) SP CE2/3(EU) CE1/3 TO t0= FF5,000 t6= FF26,068 26, which th? PT! (then TO)) 23, CE1/3 25, CE2/3 22, nonTO ,nonEU 24, power? 28,concl Questions of statistical power etc., don't discuss them at this page but go to the powerpoint slides that have them. 21 7/6 1 U 5/6 Real incentives discussed after first two curves. 4/6 3/6 2/6 FF 5,000: € 1000 = $ 1300 1/6 0 FF Utility functions (group averages) TO(PT) = TO(EU) CE1/3(PT) = CE1/3 (EU) (gr.av.) CE2/3(PT) corrects CE2/3 (EU)

22 Question: Could this identity have resulted becausethe TO method does not properly measurechoice-based risky utility? (And, after answering this, what about nonEU?) Reassure them that analyses will remain valid under nonEU.

For which c2: ? t0 c1 For which c1: ~ ? c2 c2 c3 For which c3: ~ ? t6 21, curves 21, curves 23 If lack of time: skip all algebra. Only discuss choice of w. 3d utility measurement: At PT: Discuss that no individual w's were known. Certainty equivalent CE1/3 (with good-outcome probability 1/3) EU & RDU & PT (for gr.av.) t0 c2 U(c2) = 1/3 ~ (Chris Starmer, June 24, 2005) on inverse-S: "It is not universal. But if I had to bet, I would bet on this one.". t6 U(c1) = 1/9 U(c3) = 5/9

24 • Questions • Could this identity have resulted because our experiment is noisy(cannot distinguish anything)? • How about violations of EU?

For which d2: ? d1 For which d1: ~ ? d3 For which d3: ~ ? 21, curves 21, curves 25 4th utility measurement: If lack of time: skip all algebra. 2/3 Certainty equivalent CE (with good-outcome probability 2/3) CE2/3(EU): CE2/3(PT) (gr.av): t0 d2 U(d2) = 2/3 U(d2) = .51 ~ t6 t0 U(d1) = 4/9 U(d1) = .26 d2 d2 U(d3) = 8/9 U(d3) = .76 t6

26 So, our experiment does have the statistical power to distinguish. And, EU is violated. Which alternative theory to use? Prospect theory.

.51 1/3 2/3 16,TOmethod 27 1 w 1 0 1/3 p Figure.The common weighting fuction w(1/3) = 1/3; w(2/3) = .51 We re-analyze preceding measurements in terms of prospect theory; first TO.

Underone risky utility, UCE2/3= UCE1/3 = UTO = USP However: RDU : PT At one risky utility, say that we reconfirm BP&W. They also had preference reversals and reference dependence. 28 5. Conclusions Under EU:usual discrepancies for risky ut., UCE2/3 UCE1/3 , UTO Risky choice-based U = riskless choiceless U??

Interest in choiceless inputs in economics: 29 • Gilboa & Schmeidler (2001), "A Cognitive Model of Individual Well-Being," Social Choice and Welfare 18, 269–288. • Fox, Craig R. & Amos Tversky (1998), "A Belief-Based Account of Decision under Uncertainty," Management Science 44, 879895. • Kahneman (1994), "New Challenges to the Rationality Assumption," Journal of Instit. & Theor. Ecs 150,18-36. • Tinbergen, Jan (1991), “On the Measurement of Welfare,” Journal of Econometrics 50, 713. • van Praag, Bernard M.S. (1968),"Individual Welfare Functions and Consumer Behavior.”North-Holland, Amsterdam, 1968. Especially useful if choice anomalies are prominent. We: relate choiceless inputs to revealed preference. Show how choiceless inputs can reinforcerevealed preference!

30 Experimental economics has shed new light on classical debates about utility: Don't talk but look.

31 Appendix on Analysis of Data All analyses with ANOVA (so, correcting for individual variation). We tested on raw data, and on parametric fittings. Parametric fittings of utility of: Power (CRRA); Exponential (CARA); We developed a one-parametric subfamily of Saha's expo-power satisfying economic desiderata; first presented in ESA-Amsterdam, October 2000. Later used by Holt & Laury (2002).