Download

1 / 1

10 likes | 26 Views

Learn between Endowment vs Term Insurance to make an informed decision on the right coverage for you. Compare and choose the best option.<br><br>

E N D

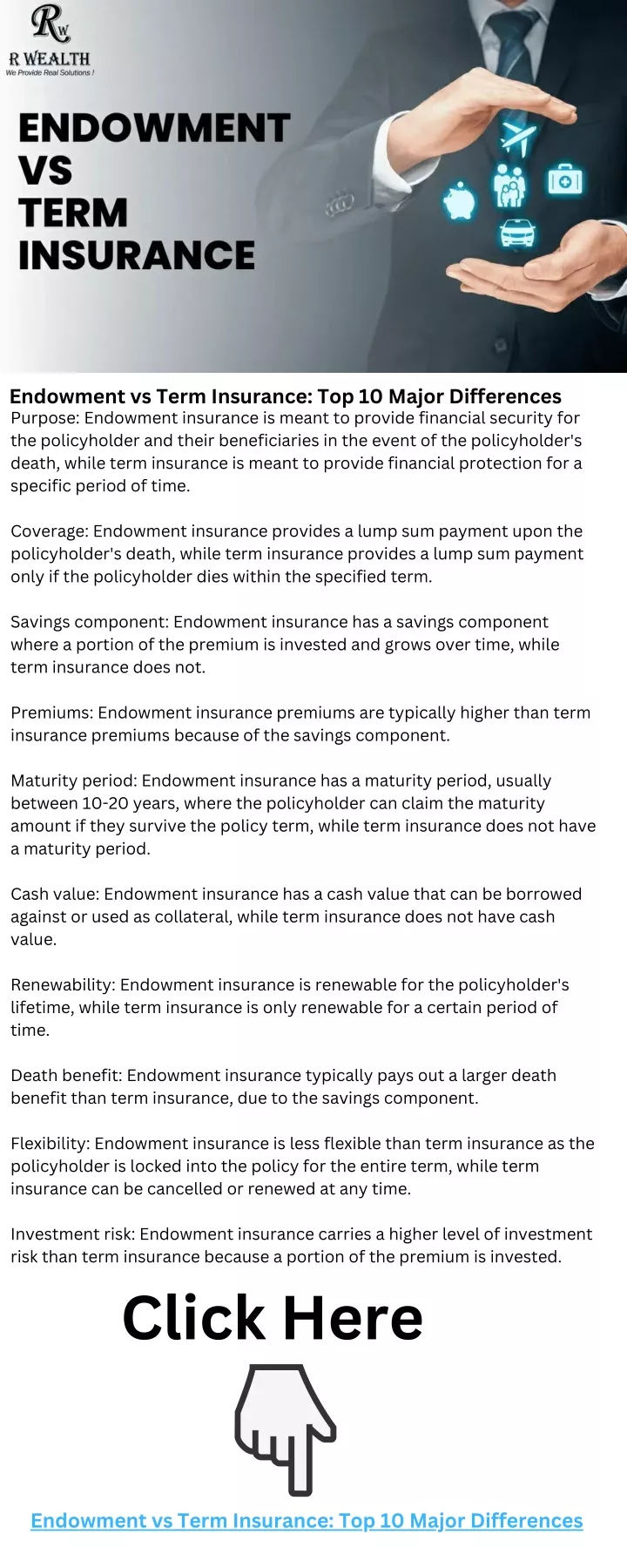

Endowment vs Term Insurance: Top 10 Major Differences Purpose: Endowment insurance is meant to provide financial security for the policyholder and their beneficiaries in the event of the policyholder's death, while term insurance is meant to provide financial protection for a specific period of time. Coverage: Endowment insurance provides a lump sum payment upon the policyholder's death, while term insurance provides a lump sum payment only if the policyholder dies within the specified term. Savings component: Endowment insurance has a savings component where a portion of the premium is invested and grows over time, while term insurance does not. Premiums: Endowment insurance premiums are typically higher than term insurance premiums because of the savings component. Maturity period: Endowment insurance has a maturity period, usually between 10-20 years, where the policyholder can claim the maturity amount if they survive the policy term, while term insurance does not have a maturity period. Cash value: Endowment insurance has a cash value that can be borrowed against or used as collateral, while term insurance does not have cash value. Renewability: Endowment insurance is renewable for the policyholder's lifetime, while term insurance is only renewable for a certain period of time. Death benefit: Endowment insurance typically pays out a larger death benefit than term insurance, due to the savings component. Flexibility: Endowment insurance is less flexible than term insurance as the policyholder is locked into the policy for the entire term, while term insurance can be cancelled or renewed at any time. Investment risk: Endowment insurance carries a higher level of investment risk than term insurance because a portion of the premium is invested. Click Here Endowment vs Term Insurance: Top 10 Major Differences