Download

1 / 0

0 likes | 109 Views

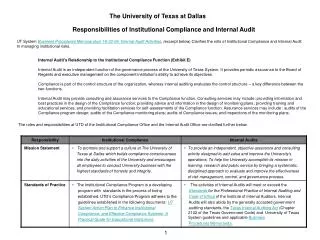

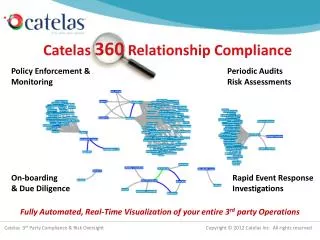

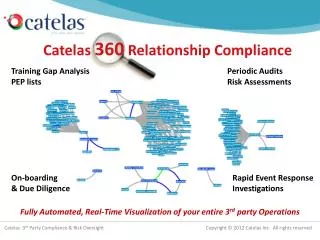

Policy Enforcement & Monitoring . Periodic Audits Risk Assessments. Catelas 360 Relationship Compliance. On-boarding & Due Diligence. Rapid Event Response Investigations. Fully Automated, Real-Time Visualization of your entire 3 rd party Operations.

E N D