Download

1 / 61

610 likes | 621 Views

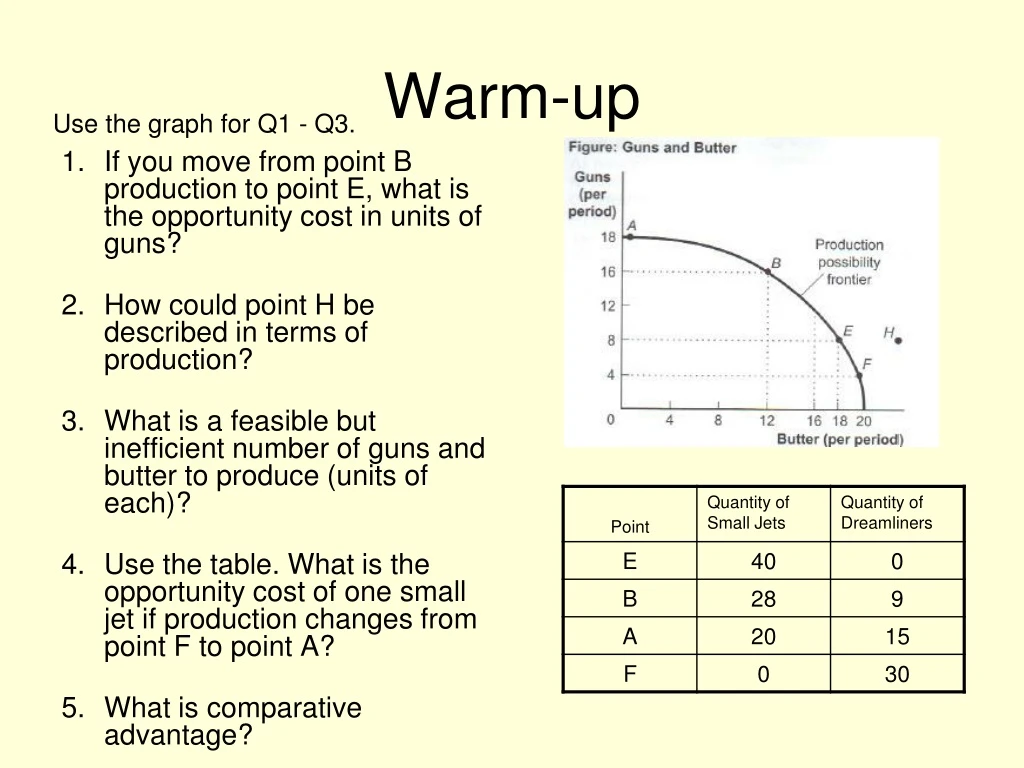

Warm-up. Use the graph for Q1 - Q3. If you move from point B production to point E, what is the opportunity cost in units of guns? How could point H be described in terms of production? What is a feasible but inefficient number of guns and butter to produce (units of each)?

E N D

Warm-up Use the graph for Q1 - Q3. • If you move from point B production to point E, what is the opportunity cost in units of guns? • How could point H be described in terms of production? • What is a feasible but inefficient number of guns and butter to produce (units of each)? • Use the table. What is the opportunity cost of one small jet if production changes from point F to point A? • What is comparative advantage?

Supply and Demand Chapter 3

Markets • Any place where goods and/or services are bought and sold • Can be a two person market or a global market (and everything in between) Competitive Markets

Competitive Markets • Many buyers and many sellers! • What are some examples of products that sell in competitive markets? • What are some examples of products that sell in markets that are NOT competitive?

Demand Schedule A schedule that shows the various amounts of a product that consumers are willing and ableto buy at various pricesat a particular time. What are the two variables in the demand schedule? The schedule shows the relationship between PRICE and QUANTITY DEMANDED.

Demand Schedule and Demand Curve Is the relationship between the two variables negative or positive?

Ceteris Paribus Assumption • All other factors remain constant.

Law of Demand • The fact that, asprices rise, quantity demanded falls, ceteris paribus. • As prices fall, quantity demanded rises, ceteris paribus. • There is an INVERSE relationship between Price and Quantity Demanded.

Sketching the Demand Curve • QUANTITY DEMANDED on the X axis. Label axis. • PRICE on the Y axis. Label axis. • Plot the points from the demand schedule.

6 5 4 3 2 1 0 Price (per bushel) 10 20 30 40 50 60 70 80 Quantity Demanded (bushels per week) Individual Demand P Individual Demand P Qd $5 4 3 2 1 10 20 35 55 80 D Q

Changes in Demand • A change in demand is reflected graphically by a new demand curve. • An increase in demand is shown by a new demand curve to the right of the original curve. • A decrease in demand is reflected by a shift to theleft of the original demand curve.

Demand Increase or Decrease An Increase in demand means a RIGHT movement of the line P 6 5 4 3 2 1 0 Individual Demand A Movement between two points on a demand curve is called a change in quantity demanded P Qd $5 4 3 2 1 10 20 35 55 80 Price (per bushel) D2 D1 A Decrease in demand means a LEFT movement of the line D3 Q 10 20 30 40 50 60 70 80 100 Quantity Demanded (bushels per week)

Shifts or Changes in Demand R – E – T – I - N • Other things are NOT equal. • Changes in: • Related goods or services (price) • Expectations • Tastes of preferences • Incomes of consumers • Number of consumers

Shifts in Demand • Related Goods and Services (Prices of) • Substitute Goods – a related good that can be used in place of another good • Coke or Pepsi • Butter or Margarine • Nikes or Reebok • Jeans or Khakis • Complementary Goods – goods usually consumed together • Peanut Butter and Jelly • Movies and Popcorn • Hot dogs and hot dog buns

Shifts in Demand: Related Goods • Substitute Goods • If the price of Coke goes up , the demand for Pepsi will go up . • Complementary Goods • If the price of Jelly declines , the demand for peanut butter will increase .

D D Shifts in Demand: Expectations • If consumers worry that they may lose their job, they will spend less now. • If consumers feel prices will rise in the near future, they will spend more now.

Shifts in Demand: Tastes/Preferences • Until World War II, men wore hats. • Greater knowledge about health has increased demand for vegetables and/or organic food.

Shifts in Demand: Incomes of Consumers • When incomes rise, the demand ofnormalgoods increases. • When incomes rise, the demand for inferior goods decreases.

Shifts in Demand: Incomes of Consumers Time-lag • In general, as consumer incomes rise there is an increase in demand for most consumer goods and services. • As incomes decline, there is a decline in demand for most goods and services.

Shifts in Demand: Number of Consumers • Increase in the number of consumers increases demand. • Decrease in the number of consumers decreases demand.

P D1 Q Demand Shift: Practice Example When the price of a substitute good rises, show on the graph what happens to the demand of the original good. D2

P D1 Q Demand: Practice Example When income falls, show on the graph what happens to the demand of a normal good. D2

Supply Schedule and Supply Curve • A schedule that shows the various amounts of product that producers are willing and ableto produce and make available at various pricesat a particular time. • What are the two variables? • The schedule shows the relationship between PRICE and QUANTITY SUPPLIED.

Supply Schedule and Supply Curve Is the relationship between the two variables negative or positive?

Ceteris Paribus Assumption • All other factors remain constant.

Law of Supply • As prices rise, the quantity supplied rises, ceteris paribus. • As prices fall, the quantity supplied falls, ceteris paribus. • There is a DIRECT relationship between Price and Quantity Supplied.

Sketching the Supply Curve • QUANTITY SUPPLIED on the X axis. Label the axis. • PRICE on the Y axis. Label the axis. • Plot the points of a supply schedule.

Individual Supply P 6 5 4 3 2 1 0 Individual Supply S1 P Qs $5 4 3 2 1 60 50 35 20 5 Price (per bushel) Q 10 20 30 40 50 60 70 Quantity Supplied (bushels per week)

Changes in Supply • A change in supply is reflected graphically by a new supply curve. • An increase in supply is shown by a new supply curve to the right of the original curve. • A decrease in supply is reflected by a shift to the left of the original supply curve.

Individual Supply Supply Can Increase or Decrease P An Decrease in Supply Means a Shift of Line to the Left 6 5 4 3 2 1 0 Individual Supply S3 S1 S2 P Qs $5 4 3 2 1 60 50 35 20 5 Price (per bushel) An Increase in Supply Means a Shift of Line to The Right A Movement Between Two Points on Supply Curve is Called a Change in Quantity Supplied Q 2 4 6 8 10 12 14 Quantity Supplied (bushels per week)

Shifts or Changes in Supply T-O-N-E-R • Other things NOT equal. • Changes in: • Technology • Other goods firm produces (price of) • Number of sellers • Expectations of firms • Resource (input) prices

Shifts in Supply: Technology • Technological improvements lead to lower costs and increased supply. • Technology is not always “high” technology—methods people use to turn inputs into useful goods and services. Spend less on inputs

Shifts in Supply: Other Goods • Other goods and services the firm produce (prices of) • A rise in the price of soccer balls may lead to an athletic company producing less baseballs.

Shifts in Supply: Number of Sellers • As more firms enter a market, the supply curve shifts to the right.

Shifts in Supply: Expectations • In general, if businesses are expecting future profits, they will increase supply. • Theopposite is true if businesses are pessimistic about future profits. Summer demand for gasoline increases

Shifts in Supply: Resource Price • A decrease in resource (input) prices leads to an increase in supply. • An increase in resource (input) prices leads to a decrease in supply. Airline Fuel Cost

P Q Supply: Practice Example When the price of a substitute input falls, show on the graph what happens to the supply of the original good. S1 S2

P Q Supply: Practice Example When the price of an input rises, show on the graph what happens to the supply of the good. S2 S1

Supply Curve Shift or Movement on Supply Curve • More homeowners put their houses up for sale during a real estate boom that causes house prices to rise. • Many strawberry farmers open temporary roadside stands during harvest season, even though prices are usually low at that time. • Immediately after the school year begins, fast-food chains must raise wages, which represent the price of labor, to attract workers. • Many construction workers temporarily move to areas that have suffered hurricane damage, lured by higher wages. • Since new technologies have made it possible to build larger cruise ships (which are cheaper to run per passenger), Caribbean cruise lines offer more cabins, at lower prices, than before.

Competitive Market Equilibrium • Markets move toward equilibrium. • Market equilibrium is when the price has moved to a level at which the quantity of goods demanded equals the quantity of goods supplied. • The market clearing price and quantity where quantity supplied equals quantity demanded.

Sketching Market Equilibrium • QUANTITYon the X axis. Label the axis. • PRICEon the Y axis. Label the axis. • Plot the points of a demand schedule. • Plot the points of a supply schedule.

Market Equilibrium 200 Buyers & 200 Sellers Market Supply 200 Sellers Market Demand 200 Buyers 6 5 4 3 2 1 0 S P Qs P Qd $5 4 3 2 1 12,000 10,000 7,000 4,000 1,000 $5 4 3 2 1 2,000 4,000 7,000 11,000 16,000 Price (per bushel) Market Equilibrium Equilibrium price 3 D Equilibrium quantity 2 4 6 8 10 12 14 16 18 7 Bushels of Corn (thousands per week)

Market Disequilibrium • Sometimes markets are temporarily in disequilibrium but move toward equilibrium. • Record crops • Weather events: hurricanes, snow, flooding • Government intervention • A surplus of a good/service is when the quantity supplied exceed the quantity demanded. • A shortage (excess demand) of a good/service is when the quantity supplied is less than the quantity demanded.

Market Demand 200 Buyers Market Supply 200 Sellers 6 5 4 3 2 1 0 S Qs P Qd P 2,000 4,000 7,000 11,000 16,000 $5 4 3 2 1 12,000 10,000 7,000 4,000 1,000 $5 4 3 2 1 Price (per bushel) D 2 4 6 8 10 12 14 16 18 Bushels of Corn (thousands per week) Market Equilibrium 200 Buyers & 200 Sellers 6,000 Bushel Surplus 3 7,000 Bushel Shortage 7 Surplus Shortage

Shift in Demand Curve • Shift in demand curve happens when changes occur in: • Related goods or service (price) • Expectations • Tastes or preferences • Incomes of Consumers • Number of Customers • What happens when the demand curve shifts? • Price? • Quantity?

Shifts in Demand • Other things are NOT equal. • Changes in: • Related goods or services (price) • Expectations • Tastes of preferences • Incomes of consumers • Number of consumers