Download

1 / 32

320 likes | 460 Views

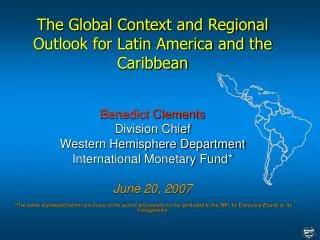

Latin America Risks and Opportunities in the New Global Context. Carlos G. Fernández Valdovinos Central Bank of Paraguay. April, 2014. Roadmap. The “new” international context Latin America: recent policies and new challenges Brief highlights on Paraguay Summary. Roadmap.

E N D

Latin America Risks and Opportunities in the New Global Context Carlos G. Fernández Valdovinos Central Bank of Paraguay April, 2014

Roadmap • The “new” international context • Latin America: recent policies and new challenges • Brief highlights on Paraguay • Summary

Roadmap • The “new” international context • Latin America: recent policies and new challenges • Brief highlights on Paraguay • Summary

International context • Almost 6 years after the beginning of the largest crisis in the past 80 years, the global economy is still in transition. • But there are finally some signs (green shoots) suggesting that the worst is over; at least for developed economies. • Latest projections suggest a more positive outlook, with recovery continuing in the US and, albeit at a somewhat lower pace, Europe. • Overall, 2014 growth projections are now higher than in the previous year (but with some regional differences).

International context • The new “normal” poses both positive and negative risks to baseline projections, especially for emerging markets. • On the upside, the US recovery might be stronger than expected, which could have a significant positive impact on growth rates in LA countries. • However, faster than expected pace of monetary tightening may lead to abrupt falls in asset prices and, in some cases, capital outflows and currency depreciations.

Recovery is underway… Widespread economic recovery, but with some regional differences. Source: IMF-WEO update January-2014.

… but emerging markets will face some challenges… Deceleration in China China has become an important trade partner for LAC countries, however high growth rates for the Chinese economy may not be sustainable. In addition, rapid credit growth to finance high investment rates has raised concerns over the robustness of the financial system. Lower commodity prices The expected deceleration in China had led to a revision in the prices of main commodities. A price moderation for soy and copper is expected in the medium-term. Oil, however, would remain at current levels. Index (Jan-10=100 Source: Bloomberg, IMF-WEO update October-2013. .

… including more difficult external financing conditions… US Treasury bond yields May 21, 2013 Bernanke announces a possible reduction in the FED’s asset-purchase program The FED normalization of monetary policy will remain a key issue in the short term, driving periods of high volatility in emerging markets. Dec 18, 13 Bernanke announces the withdrawal of the stimulus will begin in early 2014. Emerging Markets Bond s Index (EMBI) In spite of resilient capital flows, financial conditions have remained tighter after Bernanke’s surprised announcement of an imminent tapering. Source: Bloomberg.

… capital outflows and pressures in domestic currencies Bernanke’s speech May 21, 2013 Source: Haver Analytics Source: Bloomberg, IADB.

Roadmap • The “new” international context • Latin America: recent policies and new challenges • Brief highlights on Paraguay • Summary

LAC: improving conditions but some deterioration a the margin • Financial tensions are bound to arise in emerging economies after the FED´s announcement. Changing external conditions will have real effects in the economies. • Overall, U.S. recovery is a positive event, but in the short term increased financial market and capital flow volatility is a concern for emerging markets. • When combined with domestic weaknesses, the result could be sharper-than-expected capital outflows and exchange rate adjustments. • Recent “mini-stress” test: the rise in U.S. interest rates since May triggered large changes in exchange rates, sovereign spreads, stock markets, and gross portfolio inflows.

LAC: improving conditions but some deterioration a the margin • Nevertheless, the impact was not homogenous across countries: fundamentals matter. • The region, in general, has buffers to cope with these kinds of shocks thanks to relatively moderate levels of external debt, sizable official reserves, sound banking systems, and flexible exchange rates. • However, fundamentalshave deteriorated in some countries since 2008, following the implementation of counter-cyclical policies. • Still, the economies remain in better position than in the 1990s.

Changing external conditions will have an effect in LAC economies … Source:CBP.

… but the overall result over GDP growthshould be positive LAC6 GDP GROWTH Source:CBP.

In the short run, better policies will be crucial to dampen volatility

May announcement showed that fundamentals matter! Current Account and Exchange Rate Variation Exchange Rate Variation and Inflation Source: Bloomberg. .

GDP recovery was relatively faster in LAC …. International Financial Crisis Index (2007=100) Source: CBP, CBCH

…thanks to improved macroeconomic fundamentals. GovernmentDebt International Debt % of GDP % of GDP Inflation % % of GDP Source: IMF e-Library

However, some vulnerability factors recently increased in the region CurrentAccount Balances in LA General GovermmentStructural Balance* Source: IMF *Argentina, Brazil, Chile, Colombia, Dominican Republic, Ecuador, Guyana, Mexico, Panama, Paraguay, Peru, Venezuela

…rising the likelihood of a “sudden stop” episode. The expected cost of a sudden capital stoppage has increased since the pre Lehman period Source: IADB- Andrew Powell-March 2014

Roadmap • The “new” international context • Latin America: recent policies and new challenges • Brief highlights on Paraguay • Summary

Paraguay: sound macro-foundations to face headwinds • Over the past decade, policy frameworks and economic fundamentals have been strengthened. • Macro-Policies: government finances are sound, inflation low, banks are strong, buffers are large, the country is not excessively dependent on portfolio inflows, and a flexible exchange rate regime which makes a huge difference • Structural Reforms:tax reforms in 1993 and 2013, passage of a fiscal responsibility law, approval of a PPP law to tackle infrastructure bottlenecks. • The Fed exit from unconventional monetary policy will be a bumpy ride, but Paraguay is in a good position to weather more challenging times.

Strong economic growth for a decade Paraguay economic growth 1992-2014* Paraguay experienced a solid growth in the last decade supported by production and export of raw materials. Still, on top of agriculture, construction and services were also key growth-drivers. Sound policies and structural reforms increased potential growth rate. Paraguay average economic growth in the last decade is among the highest in the region. Source: IMF-WEO Oct-2013, Update Jan-2014 and CBP.

A central bank committed to low and stable inflation… A history of stable prices Paraguay has never experienced high rates of inflation and its currency (the Guarani) recently celebrated its seventieth anniversary. Monetary Regimes in Paraguay Inflation Targeting (Experimental Stage) Inflation Targeting Monetary Aggregates The CBP started the implementation of an IT regime in 2011. The explicit public commitment to control inflation as the primary objective is crucial for greater investor confidence and a more predictable business environment. Source: CBP.

…with large buffers to dampen excessive volatility… International Reserves International Reserves (% of GDP) Source: CBP and IMF-IFS. Year 2013, last data available.

…supported by soundfiscal and external balances Gen GovtGross Debt (% of GDP) Paraguay experienced eight consecutive years of fiscal surpluses. This had allowed the country to decrease its public external debt from close to 60 percent of GDP to less than 10 percent, the lowest percentage among economies with the same credit ranking. Continued fiscal surpluses (which reduced overtime the level of public indebtedness) compounded by a sharp accumulation of foreign assets has changed the country’s net debtor position vis-à-vis the world. Source: IMF-WEO Oct-2013 and CBP. Countries with BB- credit rating by Standard and Poors.

KEY RESULT: a steady improvement in credit rating Source: Bloomberg

Roadmap • The “new” international context • Latin America: recent policies and new challenges • Brief highlights on Paraguay • Summary

Summary • A normalization on monetary conditions in the US is not necessarily a negative event: economic and financial effects will depend on robustness of economic policies. • In LAC, fundamentals have improved over the past decades and most economies are well prepared to face external shocks. • However, some countries in the region appear somewhat more vulnerable to certain shocks: those economies experienced a recent deterioration in fiscal and external positions.

Summary • Growth in the region is projected to remain in low gear, reflecting a less supportive external environment and, in some cases, domestic supply-side constraints. • In countries with low inflation and anchored inflation expectations, monetary policy should be the first line of defense if downside risks materialize. • Rebuilding fiscal buffers is a key priority, especially in countries with tight capacity constraints or limited fiscal space; it will also help constrain the continued widening of current account deficits.

Summary • History teaches that exits from extremely low U.S. interest rates may be smooth or bumpy depending critically on expectations, fundamentals and countries’ capacity to respond. • Since monetary normalization is a chronicle foretold, authorities should implement policy actions today to minimize potential deleterious effects. This way countries will gain more from the global recovery.