Download

1 / 48

480 likes | 501 Views

Summary of operational and modification updates, credit rules review, and financial institute ratings comparison. Recommendations and conclusions included.

E N D

AGENDA 1.0 Introduction 2.0 Minutes and Actions 3.0 Operational Update 4.0 Modification Proposals 5.0 Significant Code Review Update 7.0 Presentation of Winter Operations 2011/2012 8.0 Proposed Review of Energy Balancing Credit Rules 9.0 Update Deposit Deed 10.0 Risk Register 11.0 AOB - Lehmans - EU Update - Team Update 12.0 Date of Next Meeting

What went well • Emergency EBCC convened in October/November 2011 for River Ter in accordance with Section X 1.2.3. • No Failures reported. • Pro-active engagement with at risk parties and EBCC members. • Review the Credit Framework • Early engagement with Users in relation to MOD 640 Adjustments. • Introduction of AMS Banking and the change of banking arrangements. • Introduction of Non Registrable Deposit Deed

Lessons Learnt • Be more aware of external factors when progressing change. • SCR has delayed progression of Modification 233v • Implementation of Non Registrable Deposit Deed • Give clearly definitive instructions to external stakeholders.

Contents • Background • Case for Change • Action Taken • Rating Amendment • Impact • Outlook • Deposit Deeds • Recommendations/Ways Forward • Conclusions • Appendices

Background • In order to provide security for the purposes of Energy Balancing Activities a Financial Institute was required to hold a rating of A1/A+ or above. • In 2011 the global economic climate deteriorate with the downgrading of a number of sovereign economies. • As a result of that downgrading many Financial Institutions were also subject to a downwards rating change.

Background Rating Comparison Table Prior to November 2011: Ratings below A1 and A+ have a zero aggregate limit and are unsuitable for Security.

Case for Change • 28.5% of FIs providing security were downgraded over 6 months. • 26 Users affected in total. • May 2011 - Credit Agricole is downgraded below A1/A+. • September 2011 - Bank of America and Intesa Sanpaolo are downgraded below A1/A+. • October 2011 - National Westminster and Royal Bank of Scotland are downgraded below A1/A+. • November 2011- Barclays Bank is downgraded to A+. % of impact frequency on affected Users

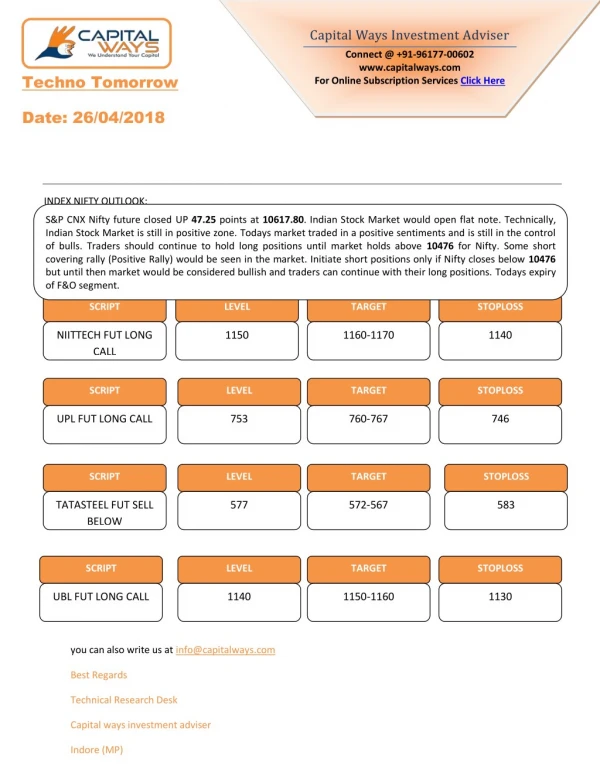

Action Taken • Energy Balancing Credit Rules amended in November 2011. • The rating boundary for the purposes of guaranteeing Security was lowered. • A £25,605,000 aggregate limit became applicable to FIs with a rating of A2/A and A3/A-. • 30 day time limit for Users to find alternative security was extended to 90 days to act as a moratorium.

Rating Amendment Rating Comparison Table Post November 2011: £25,605,000 aggregate limit now includes ratings A2, A3 and A, A-

Impact • Further 8.6%of FIs suffered downgrades from December 2011 without impact to the 3 Users with security in place totalling £7.7 Million. • Currently 26% of FIs are rated below the previous A1/A+ boundary. FI Ratings April 2012 FI Ratings April 2011 5% 26% 26% 52% 43% 48%

Outlook Moody’s Outlook 13% 87% Possible Downgrade 13% Not on Watch 87% S & P’s Outlook 61% 39% 39% Negative 61% Stable

Outlook 0 92,849,000 70,000 45,792,000 26,070,000 214,417,000 158,244,000 32,489,050 0 47,613,000 0 0 Aggregate secured credit by rating band

Outlook • Sovereign creditworthiness is expected to continue deteriorating during 2012. • A number of FIs providing security have interests in high risk areas and will be reviewed by Moody’s for potential downgrade. * Total security held as LOC is £319,376,000

Deposit Deeds • Growing use of deposit deeds. • Success in terms of offering customers an alternate method of security to a LOC. • Removes administration and associated costs involved in obtaining a LOC every year. • Assists rationalisation of accounts. • Users may not be able or wish to hold large amounts of cash.

Recommendations/Ways Forward • Alert customers when FIs are subject to a possible downgrade. • Amend Energy Balancing Credit Rules to include specific conditions on a sliding 90 day time limit for providing alternative security. • Consider further possibilities for Deposit Deeds. • Increase awareness of FIs able to provide security within the new boundary change. • Make customers more aware of alternative security measures.

Conclusions • 28.5% of FIs exceeded their aggregate limit from April 2011 to November 2011 due to downgrades. • Further downgrades are expected during 2012. • Although the economic atmosphere is generally negative the support of central banks makes failures less likely. • Change to rating requirements has maintained a stable risk position and assisted increasing overall spread of risk. • Increasing the aggregate limit is not necessary. • A proactive approach with Users should be explored. • Sliding timescale for providing alternative security necessary

Appendix 2 Currently a majority of customers rely on a LOC from a FI, although there has been a rise in Deposit Deed registration.

Background • The EBCR have been subject to ongoing amendment, however the document has not been reviewed in its entirety for a year. • The appearance and performance of the EBCR is not at full potential. • Users are not making use of the EBCR as intended.

Summary of Findings • Complaints received from potential New Users/Users that calculations are not explained with sufficient clarity. • Formatting is irregular. • Dense text and paragraphs is off-putting to readers. • Difficult to search document/ locate areas of interest. • Key information is not up to date. • Notices overly detailed/unclear.

Case for Change • Text heavy pages are not User friendly. • Individual requirements are not listed in a manner that makes them easy to identify. • Information is repeated unnecessarily.

Case for Change Cont. Information has not been updated Formatting/grammatical errors.

Case for Change Cont. • Explanations of calculations are not clear, particularly to New Users. • No references provided to enable Users to find the information necessary to perform their own calculations.

Case for Change Cont. • Notices are very lengthy. • Level/type of information included can be misunderstood.

Conclusion • EBCR document requires streamlining. • Should be updated in line with Xoserve’s current branding. • Text requires review for amendment/simplification. • Notices should be reviewed for clarification. • Request User Feedback.

Conclusion • Security is a moving target • Total number of Users 193 • Total Security in place £349,064,500 • Number of Deposit Deeds in place 55 ( £17,845,000) • Number of Letter of Credits in place 112 (£322,162,000) • Cash Deposits still in progress 26 (£9,057,500)

Register Part 1 Risk Register as at 26/4/12 :

Register Part 2 Risk Register as at 26/4/12 :

Update • Court Order in the US to reduce and allow claim for the discounted amount of $15,874,398.73 held on 22nd March 2012. Time for appeal has elapsed. • Xoserve are working with NG Legal and Skaddens to finalise a Termination Agreement – This is no longer required. • Working in conjunction with National Grid’s Treasury department to sell the claim.

Background • Collection of three European Regulations and two European Directives. • Aims to create a harmonised market for gas and electricity within the European Union. • Creates a new institutional framework: • Agency for the Cooperation of Energy Regulators (ACER); • the European Transmission System Operators for Gas (ENTSOG); and • the European Transmission System Operators for Electricity (ENTSO-E).

Developing European Network Codes • Development of binding Network Codes across 12 areas is required: • Capacity Allocation Management • Energy Balancing • Tariffs • Interoperability Rules • Trading Rules • Third Party Access • Security and Reliability • Network Connection • Data exchange and Settlement • Operational Procedures in an Emergency • Energy Efficiency • Transparency Rules

Current Position • Draft Network Code for Capacity Allocation Mechanisms was delivered on 06 March 2012 and submitted for review and comitology. • Initial draft Network Code for Balancing submitted for consultation on 13 April 2012. • Scoping documents for Tariffs FG development issued on 08 February 2012, ACER to produce FG based on responses by June 2012. • Draft FG for Interoperability issued for consultation on 16 March 2012, consultation is due to close mid May 2012.

Potential Change • CAM Network Code redefines the Gas Day. • Requirement for capacity to be allocated as ‘Bundled Capacity’ at interconnection points. • Nominations at interconnection points will be a single transaction to nominate for both sides of the connection. • Draft Balancing Code redefines current UNC definitions. • Invoicing methodologies and tariffs possibly amended. • Overriding requirement that national contracts cannot pose undue burdens on New Users.

Potential Impact Areas • Implications for Gemini and invoicing. • Change in Gas Day affects all reliant time periods ie submission of data, scheduling files etc. • External pressures to change existing Credit arrangements.

Way Forward • Ongoing analysis to take place. • EU monitoring to continue. • Maintenance of a Watching Brief.

AOB • AOB • QUESTIONS?