Download

1 / 23

240 likes | 498 Views

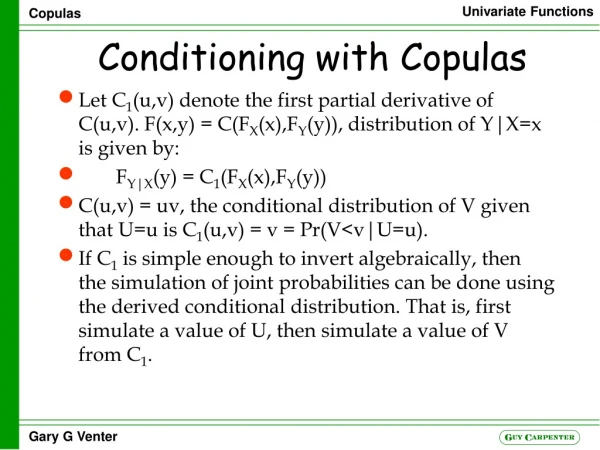

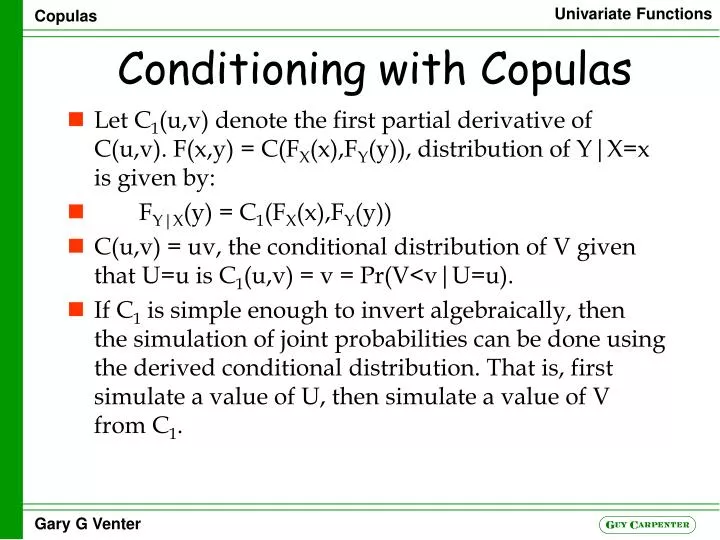

Conditioning with Copulas. Let C 1 (u,v) denote the first partial derivative of C(u,v). F(x,y) = C(F X (x),F Y (y)), distribution of Y|X=x is given by: F Y|X (y) = C 1 (F X (x),F Y (y)) C(u,v) = uv, the conditional distribution of V given that U=u is C 1 (u,v) = v = Pr(V<v|U=u).

E N D

Conditioningwith Copulas • Let C1(u,v) denote the first partial derivative of C(u,v). F(x,y) = C(FX(x),FY(y)), distribution of Y|X=x is given by: • FY|X(y) = C1(FX(x),FY(y)) • C(u,v) = uv, the conditional distribution of V given that U=u is C1(u,v) = v = Pr(V<v|U=u). • If C1 is simple enough to invert algebraically, then the simulation of joint probabilities can be done using the derived conditional distribution. That is, first simulate a value of U, then simulate a value of V from C1.

Tails of Copulas ASTIN 2001

Kendall correlation • t is a constant of the copula • t = 4E[C(u,v)] – 1 • t = 2dE[C(u1, . . .,ud)] – 1 2d – 1 – 1

Frank’s Copula • Define gz = e-az – 1 • Frank’s copula with parameter a 0 can be expressed as: • C(u,v) = -a-1ln[1 + gugv/g1] • C1(u,v) = [gugv+gv]/[gugv+g1] • c(u,v) = -ag1(1+gu+v)/(gugv+g1)2 • t(a) = 1 – 4/a + 4/a20a t/(et-1) dt • For a<0 this will give negative values of t. • v = C1-1(p|u) = -a-1ln{1+pg1/[1+gu(1–p)]}

Gumbel Copula • C(u,v) = exp{- [(- ln u)a + (- ln v)a]1/a}, a 1. • C1(u,v) = C(u,v)[(- ln u)a + (- ln v)a]-1+1/a(-ln u)a-1/u • c(u,v) = C(u,v)u-1v-1[(-ln u)a +(-ln v)a]-2+2/a[(ln u)(ln v)]a-1 {1+(a-1)[(-ln u)a +(-ln v)a]-1/a} • t(a) = 1 – 1/a • Simulate two independent uniform deviates u and v • Solve numerically for s>0 with ues = 1 + as • The pair [exp(-sva), exp(-s(1-v)a)] will have the Gumbel copula distribution

Heavy Right Tail Copula • C(u,v) = u + v – 1 + [(1 – u)-1/a + (1 – v)-1/a – 1]-a a>0 • C1(u,v) = 1 – [(1 – u)-1/a + (1 – v)-1/a – 1] -a-1(1 – u)-1-1/a • c(u,v) = (1+1/a)[(1–u)-1/a +(1– v)-1/a –1] -a-2[(1–u)(1–v)]-1-1/a • t(a) = 1/(2a + 1) • Can solve conditional distribution for v

Joint Burr • F(x) = 1 – (1 + (x/b)p)-a and G(y) = 1 – (1 + (y/d)q)-a • F(x,y) = 1 – (1 + (x/b)p)-a – (1 + (y/d)q)-a + [1 + (x/b)p + (y/d)q]-a • The conditional distribution of y|X=x is also Burr: • FY|X(y|x) = 1 – [1 + (y/dx)q]-(a+1), where dx =d[1 + (x/b)p/q]

Partial Perfect Correlation Copula Generator • Assume logical values 0 and 1 are arithmetic also • h : unit square unit interval • H(x) = 0xh(t)dt • C(u,v) = uv – H(u)H(v) + H(1)H(min(u,v)) • C1(u,v) = v – h(u)H(v) + H(1)h(u)(v>u) • c(u,v) = 1 – h(u)h(v) + H(1)h(u)(u=v)

h(u) = (u>a) • H(u) = (u – a)(u>a) • t(a) = (1 – a)4

h(u) = ua • H(u) = ua+1/(a+1) • t(a) = 1/[3(a+1)4] + 8/[(a+1)(a+2)2(a+3)]

The Normal Copula • N(x) = N(x;0,1) • B(x,y;a) = bivariate normal distribution function, = a • Let p(u) be the percentile function for the standard normal: • N(p(u)) = u, dN(p(u))/du = N’(p(u))p’(u) = 1 • C(u,v) = B(p(u),p(v);a) • C1(u,v) = N(p(v);ap(u),1-a2) • c(u,v) = 1/{(1-a2)0.5exp([a2p(u)2-2ap(u)p(v)+a2p(v)2]/[2(1-a2)])} • t(a) = 2arcsin(a)/p • a: 0.15643 0.38268 0.70711 0.92388 0.98769 • t: 0.10000 0.25000 0.50000 0.75000 0.90000

Tail Concentration Functions • L(z) = Pr(U<z,V<z)/z2 • R(z) = Pr(U>z,V>z)/(1 – z)2 • L(z) = C(z,z)/z2 • 1 - Pr(U>z,V>z) = Pr(U<z) + Pr(V<z) - Pr(U<z,V<z) • = z + z – C(z,z). • Then R(z) = [1 – 2z +C(z,z)]/(1 – z)2 • Generalizes to multi-variate case

Cumulative Tau • t = –1+40101 C(u,v)c(u,v)dvdu • J(z) = –1+40z0z C(u,v)c(u,v)dvdu/C(z,z)2 • Generalizes to multi-variate case

Cumulative Conditional Mean • M(z) = E(V|U<z) = z-10z01 vc(u,v)dvdu • M(1) = ½ • A pairwise concept Copula Distribution Function • K(z) = Pr(C(u,v)<z) • Generalizes to multi-variate case

HRT Gumbel Frank Normal Parameter 0.968 1.67 4.92 0.624 Ln Likelihood 124 157 183 176 Tau 0.34 0.40 0.45 0.43