Download

1 / 18

180 likes | 295 Views

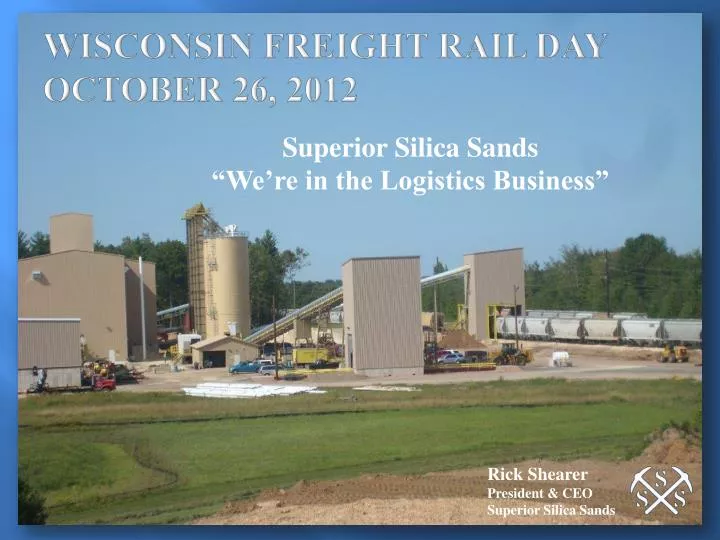

WISCONSIN FREIGHT RAIL DAY OCTOBER 26, 2012. Superior Silica Sands “We’re in the Logistics Business”. Rick Shearer President & CEO Superior Silica Sands. WELL STIMULATION AND FRACTURING. Hydraulic fracturing is a well stimulation process to optimize or restore production of oil and gas

E N D

WISCONSIN FREIGHT RAIL DAYOCTOBER 26, 2012 Superior Silica Sands “We’re in the Logistics Business” Rick Shearer President & CEO Superior Silica Sands

WELL STIMULATION AND FRACTURING • Hydraulic fracturing is a well stimulation process to optimize or restore production of oil and gas • Over 90% of the wells drilled in the U.S. now require hydraulic fracturing to produce at economic rates, according to IPAA • Fractures created along the borehole of a well increases the surface area exposed and operators are able to produce 10 times the amount of energy while drilling 1/10th the number of wells • Fractures created are kept open using a proppant – typically sieved round sand, a resin coated sand or a manufactured ceramic proppant • Proppant accounts for approximately 10 – 15% of the total cost of drilling and completing a typical horizontal well

FRAC SAND CONSUMPTION MODEL • Supply of Oil & Gas • Decline of current fields • New sources of supply • Shale gas • Oil sands • Other • Demand for Oil & Gas • GDP growth • Substitutes (renewables) • Regulation (carbon) Price of Oil & Gas Number of Drill Rigs • Regulation • Infrastructure • (water, pipelines, • labor, equipment, • sand, other) • Technology • Horizontal • drilling • Hydraulic • fracturing Wells per Rig Sand per Well Demand for Frac Sand

DRIVERS OF DEMAND FOR FRAC SAND Frac sand consumption is a product of 3 variables: NUMBER OF RIGS WELLS PER RIG SAND PER WELL • Historically, the number of rigs has been primarily driven by the price of energy • Horizontal drilling and hydraulic fracturing make it economic to drill at much lower price levels for oil and gas • 9.5% annual growth since 2002 • The number of wells drilled per rig per year has increased by 50% since 2002 • This improvement has been caused primarily by the rise of horizontal drilling and hydraulic fracturing • 3.8% annual growth since 2002 • There is a very modest amount of sand consumed for vertical drilling • The penetration of horizontal drilling and hydraulic fracturing has greatly increased the average amount of sand used per well drilled • 30.8% annual growth since 2002 • Atwood Industry Review 20070601 v2 Sources: EIA; US Geological Survey; Baker Hughes

LOCATION OF BEST FRAC SAND • The Cambrian quartz sandstone deposits (marked in red on the attached map) found in Wisconsin are a scarce resource • The Cambrian deposits in Wisconsin are unique in that the sand: • Is of unusually high quality • Can be mined in a manner that is cost efficient and environmentally friendly WHERE THE BEST FRAC SAND IS (RED) Source: Where-the-best-sand-is – Brown Presentation

SAND GEOLOGY • St. Peter’s • Jordan • Wonewoc • To date, no high quality frac sand deposits found on the globe better than Wisconsin and Eastern Minnesota

FRAC SAND PRODUCER SUCCESS IS BASEDON THE SUPPLIER’SLOGISTICSCAPABILITIES • Rail Infra-structure at Plant • Storage Track at Plant • Rail Service • Transit Time to Strategic Destinations • One-Line Haul Capabilities • Competitive Rates • Destination Storage/Transload Services By definition, “We are in the Logistics Business”

SUPERIOR SILICA SANDS COMMITMENT TOOUTSTANDING LOGISTICS FOR OUR CUSTOMERS • New Auburn Plant: Directly on Progressive Rail • Short-Line to UP Railroad @ ALTOONA • 260 Railcar Storage Capability • Clinton Plant: Directly on CN Rail • 500 Railcar Storage Capability • Providing our Customers shipment flexibility throughout • North America • Building a network of storage/transload locations • Oil & Gas Service Companies are demanding more…

SSS PARTNERED RAIL LINES Union Pacific Canadian National

FRAC SAND: LOOKING INTO THE FUTURE • Dramatic annual growth will level off to about 8% per annum • Frac Market will be cyclical, but with milder peaks and troughs • More capacity coming into the market but leaders remain • International Markets will begin to show significant frac sand demand • Sand producer base will diversify as Service Companies and E&P’s back integrate • Logistics will drive economics

WHAT IT ALL MEANS TO YOU …. THE RAILROADS • Shipping more sand to numerous new destinations • Unit train shipments more common • Managing bottlenecks and turnaround times becomes more crucial • With freight prices not dropping, service is king • Storage and Transload sites are over populated in some locales • Railroad Partnerships

CONCLUSIONS • The Frac Sand Boom is a “Once in a Lifetime” event. • Wisconsin is the Global Epicenter • Efficiency and cost Effectiveness in shipping this important proppant is critical • Rail is a major focal point to complete market success • Any successful frac sand producer is actually in the Logistics Business!