Download

1 / 36

360 likes | 477 Views

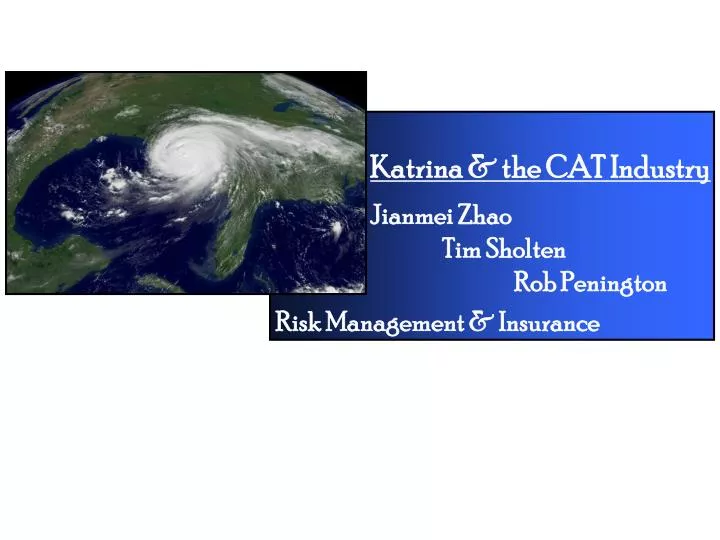

Katrina & the CAT Industry Jianmei Zhao Tim Sholten Rob Penington. Risk Management & Insurance. Overview. I. Background of Catastrophic Insurance (Tim) II. Hurricane Katrina (Jianmei) III. Case Study (Rob). Background of Catastrophic Insurance. What is Catastrophic Insurance?.

E N D

Katrina & the CAT Industry Jianmei Zhao Tim Sholten Rob Penington Risk Management & Insurance

Overview I. Background of Catastrophic Insurance (Tim) II. Hurricane Katrina (Jianmei) III. Case Study (Rob)

What is Catastrophic Insurance? • Low-Probability High-Consequence Insurance or Disaster Insurance • Manage the risk of losses that occur in an unpredictable and highly damaging event • Hurricane • Tornado • Flood • Earthquake • Terrorist Attack

Issues with Catastrophic Insurance • Difficulty in calculating and modeling magnitude of Catastrophic events • Traditional models • Reasons for creating models • Problems with the models • Problems with Privately provided Catastrophic Insurance

Traditional Catastrophic Models • Deterministic models: “Probable Maximum Loss” • Method used in the early 1990’s for catastrophic event risk • Basically analyzed possible loss scenarios from an adverse event • No probability used in the Deterministic model • Catastrophe Risk Simulation Models • Use probability in scientific models to predict the loss scenarios from a catastrophic event • Use a variety of variable to calculate probable loss

Reasons for Catastrophic Models • More accurate pricing policies • Ability to manage the amount of exposure an insurance company would be willing to accept • Accurately allocate resources to the necessary clients • Allow the insurance companies to earn an appropriate return and minimize exposure to insolvency

Problems with Catastrophic Models • Many variables in the probabilistic models • Each calculation builds off of other calculations so one wrong estimate can drastically very the result • Many of the variables are difficult to estimate • Very difficult to produce a precise model

Problems with Private Insurers • Mega-catastrophes cause a strain to insurance markets causing problems for insuring disaster-prone areas • Increased strain on the insurance market by mega-catastrophes requires increased prices but are limited by government legislation • Unable to accurately understand the cost of mega-catastrophes • No solution to diversifying catastrophic insurance risk

Hurricane Katrina Impacts on the Insurance Industry

Introduction of Hurricane Katrina • Hurricane Katrina: • Aug. 26, 2005, Hurricane Katrina made landfall as a Category 1 storm between Miami and Fort Lauderdale, Florida, the Hurricane made landfall a second time as a Category 4 storm on Aug. 29, 2005. • Katrina replaces Hurricane Andrew as the largest insurance loss from a natural disaster in U.S. history. • All insurers writing property converge in the southeastern U.S. and most reinsures across the globe will have losses stemming from Katrina.

Katrina and Insurance Market • The estimated loss is between $40 and $55 billion. • The primary insurance market will harden-but selectively. • ---The marine and energy markets will be particular problematic, insurance price in this market will rise; • ---The price for homeowners and commercial property in catastrophe-prone area will increase; • ---There will be little movement in automobile and liability rates. • The reinsurance markets will also be affected. Katrina will create pressure for stronger capitalization. • Insurers and whole society need to reconsider the potential for mage-catastrophes.

Perspectives on Katrina • Insured loss from Katrina: • Direct damage: privately insured, publicly insured, self-insured or uninsured, and privately insured loss is $40-$55 billion. • Hurricanes Andrew and Katrina • Hurricane Katrina will replace Hurricane Andrew as the largest insurance loss from a natural disaster, the insurance industry suffers largest loss compare to Andrew in 1992 which is roughly $20 billion. • Planning for Catastrophes • In addition to Hurricanes, the insurance industry is exposed to catastrophic loss from other perils (less frequent).

The Insurance Market - Financial • Rating Agency Activity • The estimated loss of capital that company will suffer relative to indicated capital required for their current rating. • The level of loss the individual loss compare to their peer group o f company. • The availability of new capital to replace the losses. • Company’s ability to take advantage of any potential price increase going forward. • For example: S& Poor’s downgrades Alea, PXRE and the Advent Syndicate 780. A.M. Best downgrades Alea and Olympus Re to Below the “A” category, it also downgrades PXRE.

The Insurance Market - Financial • Stock Prices • Katrina impacts specific companies and segments of the industry differently, so industry stock reacts differently. • Stock price negatively move directly right after Katrina, and then experience a modest rise in stock price. • Insurance broker stocks all moved higher since 8/29/2005. • Will Katrina Trigger New Market Entrants? • Andrew (1992) and “911” (2001) led a number of new insurers and reinsures entering the market. • Katrina will more be of an income statement than a balance sheet event. Significant capital loss, net income and ROE will greatly reduced.

Risk Management • 1. Exposure Management • Since Andrew, the insurance industry has significantly improved its ability to monitor geographic exposure accumulations (database, geographic mapping system). • Property reinsures require detailed extracts from the exposure database of their customers, thus having a clear picture of their accumulated exposure. • Working with various catastrophe modeling firms or their own property models, insures and reinsures can use exposure databases to estimate losses that might arise from various types of hypothetical catastrophes.

Risk Management • 2. Volatility Management • Catastrophe risk is not well spread across the insurance industry and the sufficiency of risk spreading is an important financial management issue. • The ability of the property and casualty insurance industry to spread catastrophe risk in total is limited. • The private market mechanism to reduce volatility arising from catastrophes are via securitization of catastrophe risk. • --- Catastrophe bonds and Industry loss warranties. • Federal reinsurance pool is need to cover the loss or Federal government could provide similar assistance by revising tax code to allow insurers to retain funds for catastrophe loss.

Risk Management • 3. Catastrophe Response Management • After Andrew, most states require insurers to have a written catastrophe response plan on file with their department of insurance. • Mobile catastrophe response units are a major innovation, which can easily sent to bases information (portable generator, fax machine, GPS to assist the policyholders). • Katrina creates logistical and coverage problems which lead to indemnity and expense costs well above prior catastrophes. • -the extensive flooding challenged insurer’s response plan • -wind vs flood question, and new flooding by Rita is particularly difficult to resolve in cases where the adjusters have not been able to inspect the original loss.

Public Policy Questions • Issue 1: We need a robust national dialogue on natural disaster risk management and financing. • Issue 2: Many of those hardest hit by Katrina, particularly in the New Orleans flood, are poor and under- or uninsured, either because they did not appreciate the need for insurance or could not afford it. • Issue 3: What is the role (if any) of the federal government in supplementing the insurance industry against very large losses?

AIG Insurer Est. Loss: $1.1 billion

Allstate Insurer Est. Loss: $3-4 billion

Chubb Insurer Est. Loss: $511 million

Selective Insurer Est. Loss: $0.3 million

St. Paul Travelers Insurer Est. Loss: $800 million

The Hartford Insurer Est. Loss: ???

Max RE Capital Reinsurer Est. Loss: $60–90 million

Montpelier RE Reinsurer Est. Loss: $450-675 million

Partner RE Reinsurer Est. Loss: $350 million

PXRE Group Ltd. Reinsurer Est. Loss: $235-300 million

Renaissance RE Reinsurer Est. Loss: ???