Download

1 / 11

160 likes | 469 Views

Variance Analysis. Raw Material Variances. When working through this PowerPoint slide show, make sure you have a copy of the Budget Worked Example Question and Answer to refer to. These were handed out in class and can also be found on the unit web site.

E N D

Variance Analysis Raw Material Variances

When working through this PowerPoint slide show, make sure you have a copy of the Budget Worked Example Question and Answer to refer to. These were handed out in class and can also be found on the unit web site.

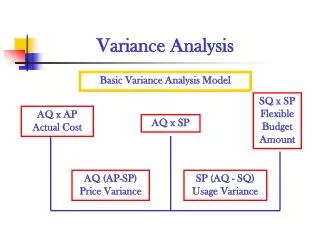

The raw material variance on the example was £6700 Favourable • This means that the company spent £6700 less on raw materials than was budgeted • We need to say WHY this might have happened • Remember – raw material cost is calculated by: • Kgs of material x price per kg (this information is found on the question) • SO, the reason for the variance is to do with either: • Amount of material used being different than planned • Or price of material being different than planned • We therefore need to calculate raw material Usage and Price variances so that we can see what caused the total £6700 F variance

Raw Material Usage Variance • This is the difference between the amount of material that SHOULD have been used to make the items, and the amount of material that WAS used • This is valued at the budgeted cost of material (in the question)

Usage Variance in the Worked Example The 1600 units produced SHOULD each have used 5 kg of raw material SO The total amount of raw material that SHOULD have been used is 1600 x 5 = 8000 kg The total amount of raw material that WAS used was 7300 kg (from the question) The difference between what SHOULD have been used and what WAS used is 8000 – 7300 = 700 kg 700 kg x £20 (the budgeted price per kg) = £14000 So the raw material usage variance is £14000 Favourable

Raw Material Usage Variance • So the usage variance is £14000 favourable • Reasons for this might be: • A better quality of material is being used • Better processes might produce less wastage • Better trained staff • Better/newer equipment • The original standard for the budget may have been incorrect

Raw Material Price Variance • This is the difference between what the amount of raw material used SHOULD have cost, and what it DID cost

Price Variance in the Worked Example The production of 1600 units used 7300 kg of raw material 7300 kg SHOULD have cost £20 per kg – 7300 x 20 = £146000 7300 Kg DID cost £153300 The difference between what 7300 kg SHOULD have cost and what it DID cost is 146000 – 153300 = 7300 Adverse So the raw material price variance is £7300 Adverse

Raw Material Price Variance • So the price variance is £7300 Adverse • Reasons for this might be: • New suppliers • Problem with supplies, price increase • Fuel costs increase price • Loss of discounts • Company might have sourced a higher quality material

Total Raw Material Variance We know that the total raw material variance is £6700 Favourable We now know that this splits into: Raw material usage variance - £14000 F Raw material price variance - £7300 A Note that you can cross check your figures: 14000 – 7300 = 6700

Practice Calculate raw material usage and price variances for all exercises completed so far, making sure that they add up to the total raw material variance that you have already calculated.