Download

1 / 19

200 likes | 348 Views

Quadratic Portfolio Management Variance - Covariance Analysis. EMIS 8381 Prepared by Carlos V Caceres SID: 27957167. Agenda. Objectives Portfolio Management Investment I n Action The Return The Volume Weighted Average Price (VWAP) The Risk Variance and Covariance

E N D

Quadratic Portfolio ManagementVariance - Covariance Analysis EMIS 8381 Prepared by Carlos V Caceres SID: 27957167

Agenda • Objectives • Portfolio Management • Investment In Action • The Return • The Volume Weighted Average Price (VWAP) • The Risk • Variance and Covariance • Optimization Of The Portfolio: Quadratic Programming

Objectives • To buy and invest in stocks efficiently by maximizing the return • To maximize the expected return of a stock portfolio • To minimize the risk with investing in different stocks • To use Excel Solver and the variance-covariance procedure to resolve Markowitz quadratic model

Portfolio Management • Portfolio management optimization is often called mean-variance (MV) optimization. • The mathematical problem can be formulated in many ways. The principal problems can be summarized as follows: • Minimize risk for a specified expected return • Maximize the expected return for a specified risk • Minimize the risk and maximize the expected return using a specified risk aversion factor • Minimize the risk regardless of the expected return • Maximize the expected return regardless of the risk • Minimize the expected return regardless of the risk

Investment in Action – The Return The return is calculated by the following components: Where: Pt – Pt-1 is the price variance of the stock in the P t-1market Pt = Price at time t Pt-1 = Price at t-1 Dt= Dividends for each stock Ct = Premium The Return: Rt = Pt - Pt- 1 + Dt + Ct Pt - 1

Investment in Action – VWAP The Volume Weighted Average Price

Expected Return VARVWAP for Portfolio We first calculate the variances of the prices Where: • VWAPt is price of current week • VWAPt-1 price of prior week Expected Return = VARPRICEAverage

The Risk of A Stock To determine the risk of a stock we apply the variance/covariance method • * Wherei is the number of observations STDDEV =

Probability Of Losing A Stock The Z-Value =

The Portfolio Expected Return is the weighted sum of the expected returns for all the stocks Rp = ΣRj * Aj where Rp: Expected return of portfolio Rj: Expected return of stock j Aj : Percent of investment in stock j The Risk of the portfolio is equal to Risk =

Optimization of the Portfolio Maximize Return = Σ Ai * VARVWAPi subject to: Where: - Ai is the percent of investment in stock I - VARVWAP is the volume weighted average price of the stock - COVARij is the covariance between each pair of stock - B is the desired risk level

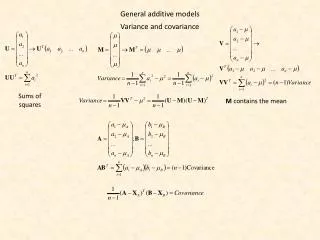

Covariance It shows how two stock prices behave between one another with respect to the expected return of each stock Covariance (A1,A2) = (1/(n-1))*Σ(A1i-U1)(A2i-U2) Where: - A1i = Variance in price of Stock 1 - A2i = Variance in price of Stock 2 - A1 = Stock 1 - A2 = Stock 2 - U1 = Expected Return of Stock 1 - U2 = Expected Return of Stock 2

Correlation Coefficient ( r ) Where: r = -1 the correlation is perfect and inverse r = 1 the correlation is perfect and direct r = 0 means that the two stocks are not correlated

The Efficient Frontier How to balance maximum return and minimum risk?