Download

1 / 20

• 230 likes • 457 Views

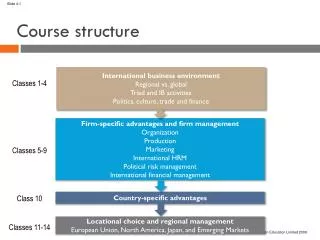

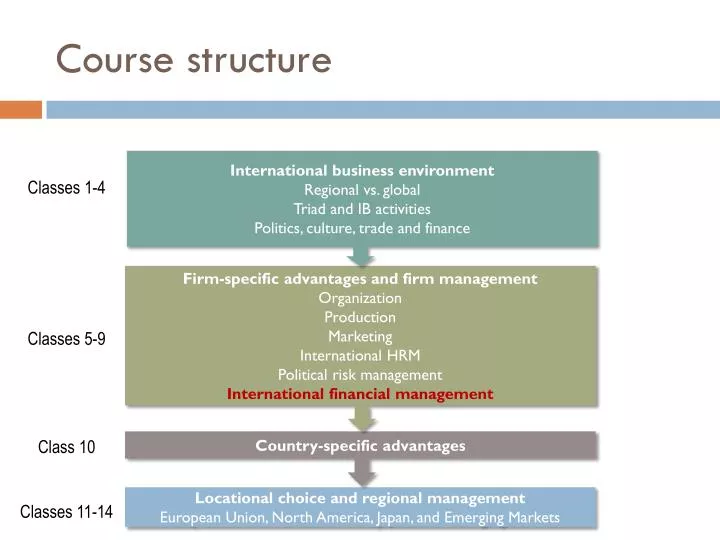

Course structure. Classes 1-4 Classes 5-9 Class 10 Classes 11-14. International business environment Regional vs. global Triad and IB activities Politics, culture, trade and finance. Firm-specific advantages and firm management Organization Production Marketing International HRM

E N D

Course structure Classes 1-4 Classes 5-9 Class 10 Classes 11-14 International business environment Regional vs. global Triad and IB activities Politics, culture, trade and finance Firm-specific advantages and firm management Organization Production Marketing International HRM Political risk management International financial management Country-specific advantages Locational choice and regional management European Union, North America, Japan, and Emerging Markets

International Financial Management • Management of funds within MNEs Sources of funds Bank borrowing Foreign currency loan from Country C Bank borrowing Intracompany loan MNE subsidiary abroad MNE parent Issuing securities (e.g., bonds, stocks) Issuing securities (e.g., bonds, stocks) Fee (e.g., license, franchise, loyalty) Payment for intrafirm sales (e.g., internal transfer) Issuing foreign currency securities (e.g., bonds, listing abroad) In Country C Retained earnings Retained earnings Exchange risk management * Capital projects (e.g., investment) Use of funds Capital projects (e.g., investment) Increased (reverse) FDI MNE subsidiary abroad MNE parent Working capital (e.g., salary, interest, dividend) Remittances Working capital (e.g., salary, interest, dividend) Other FDI projects Country A Country B * Exchange risk management is a companywide concern in all issues above, but usually managed by the parent.

International Financial Management • Parent-subsidiary relationship • Polycentric • A decentralized decision-making framework in which financial decisions are largely allocated to foreign affiliates, and financial evaluation of affiliates is done in comparison to other firms in that context. • Ethnocentric • A centralized decision-making framework in which financial decisions and control for foreign affiliates are largely integrated into home-office management. • Geocentric • A decision-making framework in which financial decisions and evaluation related to foreign affiliates are integrated for the firm on a global basis.

A comparison of the three types of parent-subsidiary relationships

Within an MNE:Financial management through global cash flows MNE parent Equity capital investments Interest payments Dividends, loyalties, and fees Loan MNE subsidiary 1 MNE subsidiary 2 Interest payments Loan

Within an MNE:Financial management through intra-firm trade • Intra-firm trade is very common among MNEs • In 2009, 50% of US goods imports were intra-firm, including 58% from OECD countries and 29% from BRICS – mainly in intermediate goods, connecting the different stages of global value chains. MNE parent Intermediary goods/services Payments MNE subsidiary 1 MNE subsidiary 2

Transfer pricing (TP) as an approach of financial management through intra-firm trade • TP is an internal price that is set by a company in intra-firm trade such as the price at which subsidiary A will purchase intermediate goods from subsidiary B. • TP is usually motivated by profit maximization through the transfer of profit to countries where the governments levy lower corporate taxes. • One underlying market principle (to avoid government scrutiny) is that the price of sales cannot be lower than the cost of sales in the exporter country.

TP - 1 • Shifting profits by transfer pricing

TP - 2 • Transfer pricing by using a tax heaven

TP – 1 & 2 • Shifting profits by transfer pricing • Transfer pricing by using a tax heaven

Practical question 1 • How would you price intra-firm exports of intermediate goods manufactured in Charlotte of US to the next production stage in Dubai of UAE ? (fill these question marks) • Where would your profit be made eventually? • How much would be the maximal net profit? • Answers will be discussed in class and posted on the course website on Friday night.

Practical question 2 • How would you price intra-firm exports of intermediate goods manufactured in Charlotte of US to the next production stage in Tampere, Finland? (fill these question marks) • Where would your profit be made eventually? • How much would be the maximal net profit? • Answers will be discussed in class and posted on the course website on Friday night.

Practical question 3 • Now assuming you had a profit management center in Hong Kong SAR, PR China, as a financial gateway to global operations, how would you price intra-firm exports of intermediate goods manufactured in Charlotte of US to the next production stage in Dubai, UAE? (fill these question marks) • Where would your profit be made eventually? • How much would be the maximal net profit? • Answers will be discussed in class and posted on the course website on Friday night.

Exchange risk management • Translation risk • HypoUS is a US-based MNE, which is legally required to consolidate the financial reports of all its foreign subsidiaries every year-end. • In the end of year 2011, its total holding in HypoMX, a Mexican subsidiary, was worth100 million Mexican Peso (MXN). The spot exchange rate for translation and consolidation was 0.081USD/MXN. • In the end of year 2012, its total holding in HypoMX was worth 101 million MXN, a 1% gain in MXN. The spot exchange rate for translation and consolidation was 0.08USD/MXN. • What was the gain/loss in % caused only by foreign exchange risk during the period? • Answers will be discussed in class and posted on the course website on Friday night. • Other examples: receivables (sales on credit); payables (purchase on credit).

International Financial Management Exchange risk hedging techniques

International Financial Management Exchange risk hedging techniques

Exchange risk management • Hedging techniques • HypoUS is a US-based MNE, which is legally required to consolidate the financial reports of all its foreign subsidiaries every year-end. • In the end of year 2011, its total holding in HypoMX, a Mexican subsidiary, was worth100 million Mexican Peso (MXN). The spot exchange rate for translation and consolidation was 0.081USD/MXN. • In the end of year 2012, its total holding in HypoMX was worth 101 million MXN, a 1% gain in MXN. The spot exchange rate for translation and consolidation was 0.08USD/MXN. • Hedging technique 1: in the end-2011, enter a 360-day forward rate agreement for end-2012 at 0.0802USD/MXN at an ignorable cost. What would be the total gain/loss in USD? • Hedging technique 2: in the end-2011, buy a 360-day forward call option for end-2012 at 0.0802USD/MXN at an ignorable cost to cover the entire holding. What would be the total gain/loss in USD? What if the spot exchange rate in the end-2012 was 0.082USD/MXN? • Answers will be discussed in class and posted on the course website on Friday night.

Team assignment 4 (5 points) • How would you price intra-firm exports of intermediate goods manufactured in Charlotte of US to the next production stage in Tampere, Finland, for maximizing total net profit? The exchange rate was $1.5/€ on the day when Charlotte-Luxembourg transaction was made. All profits should be translated into €. Fill the question marks in the table (3.5 points in total). • Assuming no hedging techniques had been used, what would be the total net profit if the exchange rate on the day of Charlotte-Luxembourg transaction was $1.25/€? All profits should be translated into € (0.5 point). • In an effort to hedge foreign currency risk, you had previously bought a forward call option of $1.3/€ at an ignorable cost. The option can be exercised on the day of Charlotte-Luxembourg transaction, when the spot rate was $1.5/€. What would be the total net profit (0.5 point)? What would be the total net profit if the spot rate was $1.25/€ (0.5 point)? All profits should be translated into €.