Download

1 / 20

210 likes | 372 Views

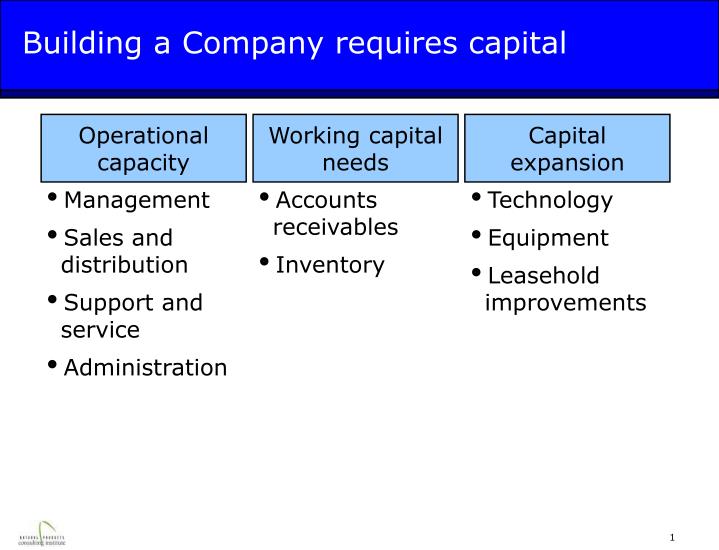

Working capital needs. Capital expansion. Accounts receivables Inventory. Technology Equipment Leasehold improvements. Building a Company requires capital. Operational capacity. Management Sales and distribution Support and service Administration.

E N D

Working capital needs Capital expansion • Accounts receivables • Inventory • Technology • Equipment • Leasehold improvements Building a Company requires capital Operational capacity • Management • Sales and distribution • Support and service • Administration

Think about the sources of funding across the life of your business Angel investors Institutional Investors Banks Friends & family Business Lifecycle Concept Sales Growth Profitability

Angel vs. Institutional Investors Angels Institutional Source of Funds • Own money • Other’s money (e.g. pension funds, insurance companies, foundations) Business stage • Mostly seed, start-up and early stage (but moving more and more to later….) • Most are later stage investors 3

The front line of equity investors: Angels • Angel investors: Wealthy individuals who make equity investments in private companies, typically early stage • Investment range (~$10-$250K) • Use referral networks (attorneys, CPAs, bankers) • 140K+ active angels in the US, investing $20B+ annually • “Accredited” Investors ($200K annual income & $1MM+ in net worth) • Many are former entrepreneurs • Angel groups • Larger investments; follow-on capacity • Regular meetings • Syndication

Goal of Angel Rounds: Prove you have a scalable business that can succeed if funded • Capital is hard to get at any stage, the further you can go and the more you can prove before approaching professional capital, the better your odds • Build a strong, numbers driven story that has shown it can scale • Product in the market • Sales/Concept proven • Proving you can gain distribution and drive velocity at the shelf is most important … quality of revenue is as important as quantity • Things from which you can extrapolate: “show the white space” • Team/Advisors in place • If you can get capital, valuation will be based both on your past performance and the strength of your “going forward” story • Be capital efficient early on • Delay all unnecessary costs: premature IP, legal, PR, “2.0” website • Bootstrap; work without a salary; moonlight; run lean ops; focus on revenue-generating aspects of the business; partner for equity • “The more self-sufficient a company is, the less risky it appears…” 5

Average 15-20% Annualized Return on Investment As… *Memo: Years = 5 year horizon *Chart Courtesy of ASW

Angel Round Dynamics • It’s a numbers game so you need to build investor momentum • In many angel investments, 1/3 comes from a lead investor; • Second third from a team of people following the lead • Last third, random … cast a wide net, be Fearless, Accept No’s • Go hunting for that lead! • The simpler and more straightforward the terms in the angel round, the better for all parties • Equally importantly, terms shouldn't impede any future financings Always think FIRST about the NEXT round of capital

Materials for Investors • Make the Company as Real as Possible • Pictures of Packaging • Effectively Frame up in the Competitive Context • Make realistic assumptions • Be concise, compelling & realistic • Write well; look professional • Preempt obvious questions/concerns and be mindful issues which might knock you out of consideration. • You’re selling an investment and not just an idea/product … be legally prepared to take in capital

You’ll need a core set of materials when you enter the fundraising market Communicate a Vision, an Understanding and The Capability to Execute Against It Executive Summary Business Plan Investment Documents Company Presentation Financial Model • 2-4 pages • Something you can send to virtually anyone • 10-15 pages • Detailed 20-40 page document • Detailed bottoms-up • Scenario Driven • PPM • Term Sheet • Subscription Agreement • Shareholder Agreement 9

A Strong Executive Summary is critical • Cover all core parts of the business in 2-4 pages • Topics (usually in this order – same for business plan) • Problem • Your solution • Business Model • Underlying point of differentiation, i.e. the unique selling proposition (secret sauce) • Marketing and Sales • Competition (features/benefits – comparison slide) • Team • Projections and milestones (Financials, historic & projected) • Status and timeline • Summary and Call to action • Exit strategy/market comps • Ask/Use of Proceeds • Capitalization to date 10

Manage-ment • Previously made money for investors • Successful startup, ideally in same sector/space • Complete team in core areas (sales, marketing, finance, etc) Market • Large, fast growing with few competitors Product/Tech. • Great Packaging • Differentiated yet understandable and priced appropriately • Proprietary position (barrier to entry such as established market position and/or intellectual property, patents) • Scalable: Can extend into multiple channels and geographies, no structural barriers to growth • Exitable: A range of potential acquirers exist Business Model Financial • Sustainable gross margins > 40% • Limited financing risk (future rounds likely) • No financial liabilities that affect value or equity position Legal • No legal contracts that affect value or equity position • No outstanding litigation around intellectual property or other assets Your business is assessed against an “ideal” Source: Clear Venture Partners, Inc.

Valuation Terminology Basics Pre-money + New money = Post-money • Valuation before the investment • “Pre” • The investment • Valuation that the company is “sitting on” • Post” Post-money valuation $2M buys 40% of company $3M pre-money 12

$2M raise scenarios: Staged Rounds Series A Series B New Pre • Raise $1M on a $1M Pre • Pre = Entrepreneur Ownership • New investor buys 50% of company • Achieve milestones and prove early business model • 18 months later raise $1M on a $4M pre • Up round: $2M company value “steps up” to $4M • New Investor buys 20% • Entrepreneur owns 40% • Srs A has 40% at 2X the value –$1M now “worth” $2M

Some resources Events • Nutrition Capital Network • 2x/year • 20 Companies presenting to 50+ institutional/strategic investors • Investors’ Circle • 2x/ year • Tracks for Health & Wellness/Other consumer companies to present to “socially responsible” angel/fund investors • Newsletters Angel Associations • Angel Capital Association (www.angelcapitalassociation.org/) • Directory of 330+ angel groups, organized by state Investment Bankers • Bankers know the market and players • Many have industry newsletters for free

Some resources Blogs • “Healthy Living and Consumer Venture Capital, Consulting and Investment Banking” (Mike Burgmaier) www.nevc.blogspot.com • “A VC” – Fred Wilson from Union Square Ventures – great blog on general VC trends: http://www.avc.com/a_vc/ • “Ask the VC” – General blog with great archive http://www.askthevc.com/blog/ • 2X Partners Blog & Trend Watch: http://www.2xpartners.com/ 15

Some Summary Considerations in Finding the right capital • Consider your personal goals • Your role in company over time • When you take someone else’s money, you have taken on an entirely new responsibility to the company and shareholders • Shareholders need to be paid back: Is this a lifestyle for you or the next Microsoft • Be realistic on time and effort it takes to secure funding • Find investor/company alignment • Stage of development • Goals; return objectives; timing…. • Respect the Capital • Valuation and Terms • Don’t take “No”s in the process personally Source: Clear Venture Partners, Inc.

Additional Slides Appendix 17

Institutional investors can come in several types • Family Offices • Wealthy family private investment arms • Fundless Sponsors • Deal-by-deal economics • No dedicated pool of capital • Investor deal fees • Term sheet “lock up” first step • Dedicated Private Equity funds • Many investors/”Limited Partners” (LPs) create a dedicated pool of capital • Defined life vehicle (10 years) 18

Finding the right institutional investor for you is important Stage • Early, Development, Late Fund size/Amount to invest • Alignment needed • Average investment over multiple rounds +/- 25%: Take the size of the fund & divide by 15 Active/Passive Investors • People and funds are different • Active, expert “accelerators” /operating partners vs. “just” money Expectations • Returns (Spectrum of pure financial to “social”) • Timing to exit: Year of fund matters • Communication: Frequencty/depth Temperament • Whatever your plan is, you are unlikely to hit it….boardroom dynamics…logical? Rational? Which investor/ not just which fund • Who will join your board? 19

Some active funds Later Stage Early/Development Stage Hosts: Financing Fast Growth