Download

1 / 7

70 likes | 317 Views

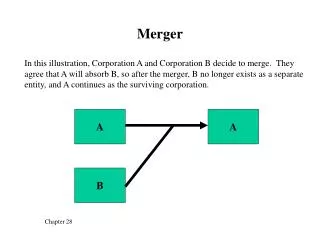

Merger & Acquisitions. takeovers. M&A. Acquisition. Acquisition of stock. Acquisition of Assets. Proxy contest. LBO /MBO. Taxes and Acquisitions. Taxable acquisitions Gains or losses are subject to tax Target firms shareholders demand higher price in a taxable acquisitions

E N D

Merger & Acquisitions • takeovers M&A Acquisition Acquisition of stock Acquisition of Assets Proxy contest LBO /MBO

Taxes and Acquisitions • Taxable acquisitions • Gains or losses are subject to tax • Target firms shareholders demand higher price in a taxable acquisitions • Target firms assets are revalued in a taxable acquisitions (written up), therefore depreciation of the assets of acquiring firm increases. • The 1986 Tax reform Act curtailed the benefits of write up as it taxes the gain • If shares are offered for the acquisitions, it is generally tax free

Accounting for acquisitions • Pooling • Purchase • 2001 FASB eliminated pooling of interest. • Under purchase, the assets of target firm is reported at fair market value, by creating goodwill on the book of the bidding firm. • The goodwill is then the difference between the purchase price and the fair market value of the net assets. • Prior to 2001 goodwill was amortized, however, after 2001 FASB requires no amortization.

Synergy • If (AB)>A+B Positive synergy • Incremental net gain=(AB)-(A+B) • Incremental cash flow • CF= EBIT+ DEP-Tax-capital requirement • CF =Revenue-cost-Tax-capital Require

Benefits of Merger • Revenue gain • Marketing gains Marketing gains in MSFT acquisition of Vermeer (webpage) 3. Strategic benefit ( real option) 4. Market power • Increase in price, reduced competition • Cost reduction, economies of scale • Vertical integration; Airlines acquiring hotels and car rental companies, or forest products buying hauling and sawmills companies. • Complementary resources • Lower taxes on tax loss, unused debt capacity

General Rules In M&A • So much of the value is usually intangible or difficult to quantify. • Do not ignore market value • Estimate incremental cash flows • Use risk adjusted discount rate • Consider transaction cost and disclosure requirements.