Download

1 / 1

10 likes | 140 Views

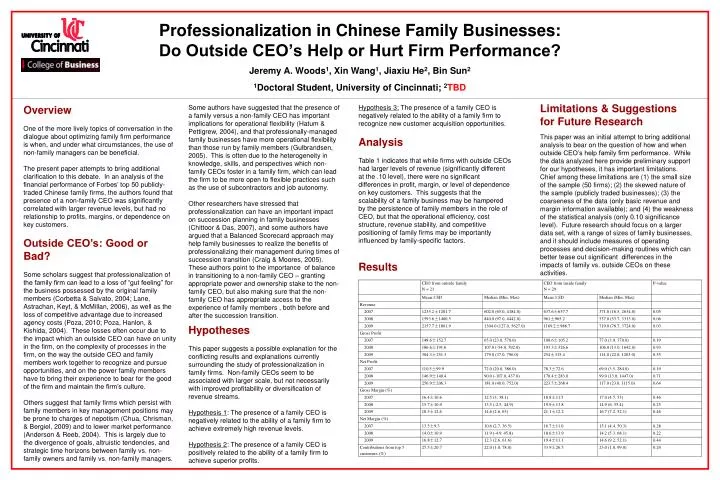

Jeremy A. Woods 1 , Xin Wang 1 , Jiaxiu He 2 , Bin Sun 2. 1 Doctoral Student, University of Cincinnati; 2 TBD. Limitations & Suggestions for Future Research

E N D

Jeremy A. Woods1, Xin Wang1, Jiaxiu He2, Bin Sun2 1Doctoral Student, University of Cincinnati; 2TBD Limitations & Suggestions for Future Research This paper was an initial attempt to bring additional analysis to bear on the question of how and when outside CEO’s help family firm performance. While the data analyzed here provide preliminary support for our hypotheses, it has important limitations. Chief among these limitations are (1) the small size of the sample (50 firms); (2) the skewed nature of the sample (publicly traded businesses); (3) the coarseness of the data (only basic revenue and margin information available); and (4) the weakness of the statistical analysis (only 0.10 significance level). Future research should focus on a larger data set, with a range of sizes of family businesses, and it should include measures of operating processes and decision-making routines which can better tease out significant differences in the impacts of family vs. outside CEOs on these activities. Overview One of the more lively topics of conversation in the dialogue about optimizing family firm performance is when, and under what circumstances, the use of non-family managers can be beneficial. The present paper attempts to bring additional clarification to this debate. In an analysis of the financial performance of Forbes’ top 50 publicly-traded Chinese family firms, the authors found that presence of a non-family CEO was significantly correlated with larger revenue levels, but had no relationship to profits, margins, or dependence on key customers. Outside CEO’s: Good or Bad? Some scholars suggest that professionalization of the family firm can lead to a loss of “gut feeling” for the business possessed by the original family members (Corbetta & Salvato, 2004; Lane, Astrachan, Keyt, & McMillan, 2006), as well as the loss of competitive advantage due to increased agency costs (Poza, 2010; Poza, Hanlon, & Kishida, 2004). These losses often occur due to the impact which an outside CEO can have on unity in the firm, on the complexity of processes in the firm, on the way the outside CEO and family members work together to recognize and pursue opportunities, and on the power family members have to bring their experience to bear for the good of the firm and maintain the firm’s culture. Others suggest that family firms which persist with family members in key management positions may be prone to charges of nepotism (Chua, Chrisman, & Bergiel, 2009) and to lower market performance (Anderson & Reeb, 2004). This is largely due to the divergence of goals, altruistic tendencies, and strategic time horizons between family vs. non-family owners and family vs. non-family managers. Some authors have suggested that the presence of a family versus a non-family CEO has important implications for operational flexibility (Hatum & Pettigrew, 2004), and that professionally-managed family businesses have more operational flexibility than those run by family members (Gulbrandsen, 2005). This is often due to the heterogeneity in knowledge, skills, and perspectives which non-family CEOs foster in a family firm, which can lead the firm to be more open to flexible practices such as the use of subcontractors and job autonomy. Other researchers have stressed that professionalization can have an important impact on succession planning in family businesses (Chittoor & Das, 2007), and some authors have argued that a Balanced Scorecard approach may help family businesses to realize the benefits of professionalizing their management during times of succession transition (Craig & Moores, 2005).These authors point to the importance of balance in transitioning to a non-family CEO – granting appropriate power and ownership stake to the non-family CEO, but also making sure that the non-family CEO has appropriate access to the experience of family members , both before and after the succession transition. Hypothesis 3: The presence of a family CEO is negatively related to the ability of a family firm to recognize new customer acquisition opportunities. Analysis Table 1 indicates that while firms with outside CEOs had larger levels of revenue (significantly different at the .10 level), there were no significant differences in profit, margin, or level of dependence on key customers. This suggests that the scalability of a family business may be hampered by the persistence of family members in the role of CEO, but that the operational efficiency, cost structure, revenue stability, and competitive positioning of family firms may be importantly influenced by family-specific factors. Professionalization in Chinese Family Businesses:Do Outside CEO’s Help or Hurt Firm Performance? Results Hypotheses This paper suggests a possible explanation for the conflicting results and explanations currently surrounding the study of professionalization in family firms. Non-family CEOs seem to be associated with larger scale, but not necessarily with improved profitability or diversification of revenue streams. Hypothesis 1: The presence of a family CEO is negatively related to the ability of a family firm to achieve extremely high revenue levels. Hypothesis 2: The presence of a family CEO is positively related to the ability of a family firm to achieve superior profits.