Download

1 / 28

280 likes | 408 Views

THE FINANCIAL CRISIS AND REFORMING GLOBAL FINANCE Problem Statement, Recent Developments, and Contours of a Reform Agenda Leonardo Burlamaqui l.burlamaqui@fordfoundation.org. New Delhi, India, January 29-30,2010. THE VISION.

E N D

THE FINANCIAL CRISIS AND REFORMING GLOBAL FINANCE Problem Statement, Recent Developments, and Contours of a Reform Agenda Leonardo Burlamaqui l.burlamaqui@fordfoundation.org New Delhi, India, January 29-30,2010

THE VISION “Public institutions need to be the vehicles by which leaders take public responsibility for the public interest. Otherwise, markets determine the public interest, which manifestly does not work, especially in finance.”

THE PROBLEM STATED PROPERLY “I believe that the root cause of the present crisis lies in the intellectual failure of economics. It was the wrong ideas of economists which legitimized the deregulation of finance which led to the credit explosion which collapsed in the credit crunch” ( Lord Skidelsky, 2009 – Keynes: The Return of the Master )

THE INSTITUTIONAL IMPLICATIONS “At a deeper level, the crisis of 2008-09 and our continued dangerous financial system are very much the fault of our regulators. Bank executives are supposed to make money. They pursues profits – and rent extraction from the government. “It is the government’s responsibility to prevent people like Jamie Dimon from creating massive social costs. The failures here – and they were colossal – were on the part of the people who ran the Federal Reserve, the Treasury, and associated agencies over the past 20 or so years.” (S. Johnson . Jan/2010) .

THE POLITICAL ECONOMY DIMENSION We’re facing a big trade-off between corporate sponsored globalization and democracy.

THE ANALYTICAL DIMENSION CAPABILITIES REQUIRED: Unique knowledge of business firms competences; strategies and of their competitive ecology Creative destruction Late 19th Century trough the end of Bretton-Woods Financial innovation financing productive Investment Long-term Funding & Venture Capital Development/ Structural Change Schumpeterian RETURNS HedgeFunds, Securitization & Leverage PONZI/ MADOFF CAPITALISM Financial innovation financing speculation Post-Reagan Washington-Consensus Sorosian CAPABILITIES REQUIRED: Knowledge about the regulatory/legal loopholes and how to structurebetson the formation & evolution of prices in currency, commodities & securities markets Destructive creation

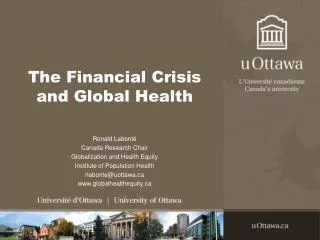

The Global Financial System: Burlamaqui Multilateral and Public DC and Geneva Multilateral and Public Asia, Russia, Middle East and Latin America BIS (G20 Central Banks) SEC FED BRICS Reg Dev Banks SWFs IMF OECD European Central Bank • Much broader than the banking system • Totally interconnected • Mostly unregulated • Structurally changing as we speak WTO WB EUROPE Chang Mai Init South Bank National Fin Reg Agencies FSB Fin Stability Board IAIS Int Ass of Insurance Supervisors GATS Credit Rating Agencies IOSCO Int Org of Sec Comm. IASC Int Acc Standards Board WFE World Fed of Exchanges IFAC Int Fed of Accountants Insurance Companies LAW FIRMS Banking System ACC FIRMS Export Credit Agencies Credit card Companies Bilateral Trade & Investment Treaties Int. Arbitration Tribunals Fiscal Shelters Mortgage Funds Hedge and Private Equity Funds Pension Funds RMBS SIVs COUNTRIES & NATIONAL STATES Global Corporations GLOBAL PRIVATE

The financial landscape: new developments in 2009 • The G20 leaders’ summit in November 2008 urged that the FSB “must expand to a broader membership of emerging economies”. • In January 2009, the IASB expanded its members and guaranteed geographical diversity on its Board for the first time. • In February 2009, IOSCO invited securities regulatory authorities from Brazil, India and China to join a body that previously included mostly G7 countries.

The financial landscape: new developments in 2009 • In March, the BASEL COMMITTEE expanded its membership by inviting Australia, Brazil, China, India, Korea, Mexico, and Russia to join the existing members (who had previously all been from developed countries). • Most dramatic of all was the announcement that same month to expand the FSB to include all G20 countries. • Summing-up : the emergence of G20 as a new – potential- source of power in global financial governance. • BUT also: the emergence of the G2. G2 overriding G20 ?

The financial landscape: new developments in 2009 Mr. Turner is daring to ask the very question that many Britons, and indeed, many Americans, are asking themselves: What good are banks if all they do is push money around and enrich themselves?As he sees it, the City takes too much from British society and gives back too little. It has grown too big and too powerful. And, he contends, the bankers have co-opted many of the regulators who watch over them ( A. Turner: Chief British Financial Regulator, quoted in NYT 9/24/2009) • Aggressive calls from European regulators for a comprehensive overhaul of the financial system. Will it last (?) • Asian and Latin American emerging economies surface as better equipped the weather the financial storm thanEurope or the US.A structural change (?) • The American Recovery and Reinvestment Act (5.8 % GDP) starts to impact the non financial sector. Depression avoided (?) • The Chinese stimulus package kicks in (13.5 % of GDP). Asian growth reassured (?) • The “Return of the State”: Public ownership of financial assets and financial institutions skyrockets. A new form of capitalism shaping up (?) “ Banks should be split into separate utility companies and risky ventures…. It’s a delusion to think tougher regulation [alone] would prevent future financial crises” ( Mervyn King. Governor of the Bank of England, quoted in FT 10/21/2009)

ON THE DOMESTIC FRONT (US): Theunderlying roots of the crisis remain • Toxic assets are still in hidden in bank’s balance sheets (which the Fed refuses to disclose). • A year after Washington rescued the banks considered too big to fail, the ones deemed too small to save are approaching a grim milestone: the 100th bank failure of 2009– 400 on the watch list .(NYT – October 10, 2009). • Economic conditions in the real economy continue to deteriorate – unemployment has climbed to almost 10 % (not seen since 1983) and could reach 11% in 2010. • The mortgage crisis far from solved:

ON THE DOMESTIC FRONT: Theunderlying roots of the crisis remain • "And the banks – hard to believe • in a time when we're facing a banking crisis that many of the banks created • are still the most powerful lobby on Capitol Hill. And they frankly own the place.“ • Senator Dick Durbin (D-IL), April 27, 2009 . • Financial concentration has increased: the top 3 US banks now control 30 % of all deposits, (up from 20 %). • Or…“Too big to fail” got worse… • Investment banks are back in business ( JP Morgan: +11.9 B in 09), butcredit is not flowing… • And other jumbo banks are still on the ropes (BOFA: -5.9 B in 4th Q, Citigroup: -1.6 B in 09). • The “Volcker Plan” (1/2010). Will it succeed? Is it enough ? • The elephant in the room: the political influence of finance. • “Lobbyists Mass to Try to Shape Financial Reform” • “The financial services industry has poured more than $220 million into lobbying • in 2009” • NYT, October 15, 2009. • “The Obama administration’s proposal for a new Consumer Financial • Protection Agency risks being watered down by lawmakers in Congress after • lobbying from banks” • FT, October 16, 2009.

THE COUNTOURS OF A REFORM AGENDA - US • Resolve the mortgage crisis through the homeowners side – not the banks - & demand complete transparency of mortgage lending, • Rationalize the regulatory “maze” (ex. Dodd proposal), • Establish a broad Financial Products Safety Agency, • Realign compensation schemes to ensure “skin in the game” for fund-managers, traders, and CEO’s, • Address financial industry political influence peddling – stop revolving door and reform campaignfinance.

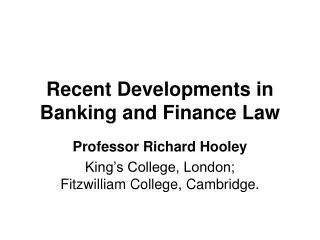

Governance Failure : Financial Regulation in the US:A Very Inefficient Maze Commercial banks Thrifts Industrial Loan Companies Bank Holding Companies Securities and Exchange Insurance Credit Unions Futures

THE COUNTOURS OF A REFORM AGENDA - GLOBAL • Re-regulate the financial system: a Glass-Steagallfor the 21st Century • Establish a new division of labor among banks and financial institutions in general: traders should not be deposit takers and vice versa. • Regulate credit and liquidity: limit leverage and raise capital requirements to banking and non-banking institutions(from Ponzi to Hedge units). • Subject OTC custom made derivatives to a pre-approval process (like prescription drugs…). If regulators don’t fully understand them, don’t allow. If they do, establish a trial period.

THE COUNTOURS OF A REFORM AGENDA - GLOBAL • Access best regulatory practices outside the US and UK and incorporate them. • Bring all bank assets and liabilities onto bank balance sheets, subject to reserve & capital requirements. • After a “grace period”, all off-balance sheet assets and liabilities declared null and void, unenforceable contracts. • Create an adequate incentive system for regulators ( unless we want “good regulation under bad regulators”).

THE COUNTOURS OF A REFORM AGENDA - GLOBAL • Reform the BIS/BCBS: make it transparent assure broad representation and coordination capabilities. • Replace Basel II in the direction of more intense macro-prudential regulation, less leverage and an early-warnings risk assessments system. • Make rating agencies a public utility. • Prevent “too big to fail”: restore the distinction among financial institutions and…. • Use competition policies to prevent excessive concentration.

THE COUNTOURS OF A REFORM AGENDA - GLOBAL • Develop a global financial governance for development agendabased on regional financial cooperation and enhanced representation by non- G20 countries (The UN back at the negotiating table) . • Create a “global financial governance body” (GFGB) where national regulation would prevail, but would be supplemented by international supervision, regulatory coordination and enforcement power (Housed where?). • Establish a mechanism for coordinated capital account control under this GFGB. • Reform the GATS agreement under the WTO.

QUESTIONS FOR DISCUSSION: The tensions between recovery and reform. The political influence of the financial industry versus democracy. The need to overcome the Anglo-American intellectual hegemony. The need to evolve from criticism towards building a coherent alternative.

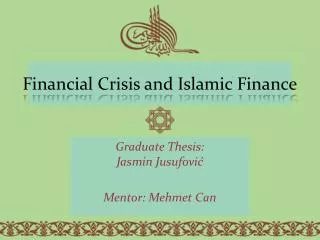

THE SYSTEM IN MOTION MINSKY’S MODEL AND THE NEW FINANCIAL SYSTEM :MAD MONEY INSTITUTIONAL FRAMEWORK: MARKETS AS WEBS OF CREDIT AND DEBT CONTRACTS Fin Deregulation: Δ liquidity + Opaqueness Δ Leverage ∆ Debt Bad debt/ Losses Asset price deflation Overshooted expectations SIVs, Derivatives ,& Securitization Long Expansion: Δ credit + Fin innov. Reckless finance Asset price inflation Financial fragilization Financial meltdown Δ Debt financing Δ Profits Liquidity & solvency problems Trade Imbalances (Δ liquidity) Lax monetary policy Hedge & Private Eq Funds Exc rate fluctuations Exc rate volatility Profits ∆ Policy Change ∆ interest rates interest rates ∆ MADOFF FINANCE PONZI FINANCE PONZI SQUARE FINANCE

The Fin Governance Grant’s Cluster: Burlamaqui Multilateral and Public DC and Geneva Multilateral and Public Asia, Russia, Middle East and Latin America LEVY BIS (G7 Central Banks) LEVY SEC FED OXFORD (GEG) BRICS Reg Dev Banks SWFs IMF IBASE OECD European Central Bank OXFORD (GEG) EURODAD CEDES NEW RULES ERF/ IDEAS WB WTO SIENA IPD CEPR National Fin Reg Agencies EUROPE Chang Mai Init South Bank PUBLIC CITIZEN TWN TWN BIC FSF Fin Stability Forum IAIS Int Ass of Insurance Supervisors South Center GATS Credit Rating Agencies IOSCO Int Org of Sec Comm. IASC Int Acc Standards Board LEVY WFE World Fed of Exchanges IFAC Int Fed of Accountants Insurance Companies LAW FIRMS Banking System ACC FIRMS Export Credit Agencies North South Credit card Companies IPD FORUM DEM Center. CUUS CEPR LEVY Bilateral Investment Treaties Int. Arbitration Tribunals Fiscal Shelters Mortgage Funds Hedge and Private Equity Funds CFI TJN IPD Pension Funds RMBS SIVs COUNTRIES & NATIONAL STATES Global Corporations De Justicia GLOBAL PRIVATE