Download

1 / 23

240 likes | 395 Views

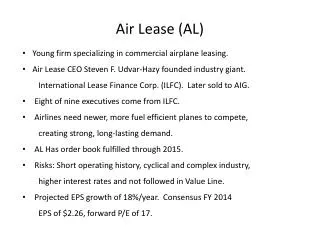

Air Lease Corporation. Wu Qianwen (Joven) Xu Wenqiang (Wayne) Presented 10-29-2013. Agenda. Introduction & Current Holding Macroeconomic Factors & Industry Overview Company Overview Management Outlook Financial Analysis Valuation Conclusion & Recommendation.

E N D

Air Lease Corporation Wu Qianwen (Joven) Xu Wenqiang (Wayne) Presented 10-29-2013

Agenda • Introduction & Current Holding • Macroeconomic Factors & Industry Overview • Company Overview • Management Outlook • Financial Analysis • Valuation • Conclusion & Recommendation

Introduction: Air Lease Corp. is an aircraft leasing company • Business: • Principally engaged in purchasing commercial aircraft which the Company, in turn, lease to airlines around the world • 98% of revenue is rental income • Fleet: • 174 aircraft as of Jun, 2013 • 132 single-aisle narrowbody jet aircraft, 30 twin-aisle widebody jet aircraft and 12 turboprop aircraft • Weighted average age of 3.5 years • Net book value grew by 11.7% to $7.0 billion as of June 30, 2013 compared to $6.3 billion as of December 31, 2012 • Employees: • 52 in 2012, far fewer than competitors • Financials: • 2012 annual sales: $ 645.853 million • 2012 net income: $ 131.919 million Revenue Million $ Net Income Million $ Source: 2012 Annual Report, Jun 30 2013 10-Q P15

Current Holding: We bought 400 shares at $ 22.32 on Dec 18, 2012 • Cost basis = $ 8,928 • Closed @ $ 30.47 on Oct 28, 2013 • Market value = $ 12,188 • Gain = 36.51% Source: Yahoo Finance

Industry & Macro: International airline industry demands drive aircraft leasing industry historically • Late 1960s and early 1970s, airlines generally own all of their aircraft • Airlines outsourced ownership of many of their airplanes through leases as fleets expanded and fixed costs grew • Leasing companies can provide airlines with a diversity of aircraft types, capacities, as well as economic flexibility Aircraft Operating Leases as a Percentage of Total WorldwideAircraft Fleet Source: Air Lease Prospectus P75

Industry & Macro: Aircraft leasing industry was expected to grow in 2010... • Number of aircraft on operating lease in 2010: 6,800 • Expected number of aircraft on operating lease in 2015: 8,500 • Implied CAGR: 4.56% • This increase will be driven by both new aircraft deliveries as well as sale-leaseback transactions Aircraft Lease vs. Other Ownership-History and Extrapolation Source: Air Lease Prospectus P76

Industry & Macro: ... And the story doesn’t change much today IMF GDP Growth Forecast %, Oct, 2013 World RPK1 Growth Projection %, By Major Regions Global New Aircraft Deliveries 2013-2032 Commercial air travel and air freight activity are broadly correlated with world economic activity and expanding at a rate of 1 to 2 times the rate of global GDP growth. – AYR 2012 annual report Footnote: 1. revenue passenger kilometers (RPKs) are measures of traffic for an airline flight, bus, or train calculated by multiplying the number of revenue-paying passengers aboard the vehicle by the distance traveled Source: IMF World Economic Outlook Database, AVITAS, Boeing and Airbus 2013 Market Outlook, AYR 2012 Annual Report

Industry & Macro: Emerging markets are driving the future growth of the industry Emerging Economies 2013 VS. 2032 Source: Airbus 2013 Market Outlook, IHS Global Insight

Industry & Macro: Overall, aircraft leasing is a highly competitive market Rivalry Competition Suppliers’ Bargaining Power • Strong (4)1 • Competition from aircraft manufacturers, banks, financial institutions, other leasing companies, aircraft brokers and airlines • Similar products • Internationalized market • Fragmented market with 100 lessors in 2010, top 5 control 50%+ number of aircraft and 60%+ of aircraft value • Strong (4.5) • Only a few huge suppliers in the market such as Airbus and Boeing Buyers’ Bargaining Power • Medium (3), emerging market (2.5) and mature market (3.5) • Large numbers of relatively smaller airlines in emerging market, with few financing channels for aircraft and weak pricing power • Relatively concentrated airline market in mature economies, with larger and more mature airline companies Substitutes • Medium (3) • Only substitute is for airlines to own aircraft themselves, which is common but not as efficient as leasing • Often airlines enter into “Sale and Lease Back” contract with lessors • Operating leasing is the trend Threat of New Entrants • Weak (2) • The industry requires expertise and customer relationships • Smaller companies tend to own more aged aircraft, which is not a very direct threat to the large players Footnote: 1. Number in the brackets is the overall rating for this factor, larger number means stronger power Source: AL Prospectus, AL Annual Reports

Company Overview: As a relatively young company, AL business is growing fast... Revenue Million $ Fleet Size and Age 98% of revenue is rental income Net Income Million $ Planned Aircraft Acquisition As of Dec 31, 2012 Planned 2013-2023 total acquisition number is 325, as of the end of 2012 Source: AL 2012 Annual Report

Company Overview: ... With an increasing focus on emerging markets Percentage of Net Book Value of Fleet by Region % Percentage of Rental Revenues by Region % Source: AL 2012 Annual Report

Management Outlook • Increasing Percentage of Unsecure Debt Borrowing • Consistently adding new aircraft to the portfolio • Owned 155 aircrafts as of December 31, 2012 • Operating in 49 countries • Net income increases 148% from 2011 to 2012 Source: AL 2012 Annual Report, Air Lease Website

SWOT Analysis SWOT Analysis Source: AL 2012 Annual Report

Financial Analysis (1) Footnote: 1. Cash Return on Equity=(Net Income + Depreciation)/Equity, this is to take the large depreciation into account when evaluating investor return Source: AL 2012 Annual Report

Financial Analysis (2) Source: AL 2012 Annual Report

DCF Analysis-Discount Rate Source: AL 2012 Annual Report, Stock Price

DCF Analysis Source: AL 2012 Annual Report, Stock Price

DCF Analysis-Sensitivity Test Source: AL 2012 Annual Report, Stock Price

Comps Analysis-Stock Performance Source: Google Finance

Comparable Analysis Air Lease Corporation Comparable Company Analysis, Millions $ Source: AL 2012 Annual Report

Decision Drivers • Strengths • Young fleet: 3.5 years • Diversified portfolio of airlines lessees • High percentage of unsecure debt • Management expertise and established network • Concerns: • Rising interest rate environment • Emerging market economy volatility

Recommendation • Valuation Summary • Current Stock Price: $30.47 • DCF Valuation: $28.81 • Comps Valuation: $23 • Recommendation • Hold

Q&A Thank you ,any questions?