Download

1 / 64

650 likes | 790 Views

K-12 School Finance Challenges and Opportunities. Contact Information. Larry Sigel, developed at the request of the Urban Education Network (UEN) Iowa School Finance Information Services 4685 Merle Hay Road, Suite 209 Des Moines, IA 50322 larry.sigel@isfis.net 515-251-5970 office

E N D

Contact Information Larry Sigel, developed at the request of the Urban Education Network (UEN) Iowa School Finance Information Services 4685 Merle Hay Road, Suite 209 Des Moines, IA 50322 larry.sigel@isfis.net 515-251-5970 office 515-490-9951 cell Last updated 1/30/2012

Overarching Problems • Funding is not equal per student. • Funding is not sufficient to produce desired outcomes. • Property tax rates still vary greatly around the state. • Property taxes are generally viewed as “too high”. • Outdated requirements in the law have not kept pace with changes in operations.

Funding Inequality • Under the foundation formula, the basic concept is that “every child is worth the same no matter where they live”. • Due to what is included in the definition of the General Fund from a revenue and expenditure perspective, it can produce unequal funding per student.

Funding Inadequacy • General funding inadequacy and unpredictability lead to financial distress and inability to produce student achievement gains which are now expected. • Due to increased expectations or societal changes, funding streams may no longer be sufficient to promote achievement.

Property Tax Equity • Schools were funded primarily with property taxes until the adoption of the current foundation formula in the early 1970’s. • Property taxes are partially equalized under the formula, but disparities still remain. • Rates range from a low of $8.34 per thousand to a high of $23.30 per thousand.

Property Tax Relief • Various proposal for property tax relief were offered in the last legislative session. • Property tax “reform” can take two approaches: • Impact valuation (ie, the value that is used in computing rates) • Impact tax rates

Property Tax Relief • Impacting valuation impacts all levying authorities: • Schools • Cities • Counties • Community colleges • Etc. etc. etc.

Property Tax Relief • Impacting tax rates impacts all classes of property similarly • Residential • Commercial • Agricultural • Industrial • Utilities/Railroads

Property Tax Relief • Greatest sin in the system – one commercial business pays $8.34 per thousand in school taxes and another exactly like it pays $23.30 (179% deviation) • Property tax reforms should be targeted at first removing taxpayer inequity and then focus on reducing overall property taxes.

Background • The current Iowa School Foundation Formula was put into place in the early 1970’s. Statement of purpose in 257.31: • “…the intent of this chapter to equalize educational opportunity, to provide a good education for all the children of Iowa, to provide property tax relief, to decrease the percentage of school costs paid from property taxes, and to provide reasonable control of school costs.”

Criteria for Formula Reform: • Improve outcomes for children • Improve property tax equity • Improve predictability • Nonpartisan • Broad support (internal/external) • Knowable and provable

Types of Reform • Equity reforms – these are reform efforts ensuring equality of funding. Can impact both students and/or taxpayers. • Adequacy reforms – these are reform efforts ensuring that funding is adequate to promote achievement. Adequacy reforms can impact Equity reforms and vice versa (imprecise). • Process reforms – these are system reforms that are less visible to the public at large but produce increased efficiency or transparency.

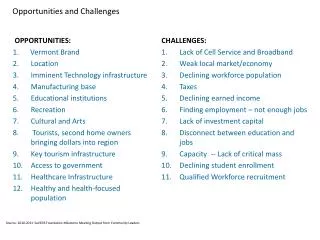

InstructionalSupport Levy • Problem: Elimination of state match (25%) and proration formula impacts some districts more than others. • Property poorest only generate about 5.5% additional resources while property richest generate 9.4% (even though both approved 10%). This equates to $318 per pupil disparity in funding each and every year.

Instructional Support Formula Funding Gap Widens Source: LSA Issue Review Nov. 3, 2011 Instructional Support Program Funding Inequities

Instructional Support Levy • Solution: • Eliminate state match funding. Allow all districts to receive the full 10% (or the amount they have specified locally). • Impact: total promised by state and not allowed $61.8 million.

State Aid for Special Education Deficits • Problem: Districts receive no state aid for special education spending above the amount allowed by state but expenditures are often out of the control of districts (ordered by each child’s IEP as determined by AEA and state and federal law). • This disproportionately impacts property poor schools – it takes a higher tax rate to generate same funds. • Also impacts those districts with relatively larger special education populations.

State Aid for Special Education Deficits • Solution: • Sliding scale adjustment based on property value per pupil (lower value = greater funds). • Goal: equalize property tax rate impact of special education. • Provides targeted property tax relief in those areas with highest tax rate. • Total statewide property tax relief potential of $37.1 million

Local Option Income Surtax for General Fund • Problem: The current formula does not give districts an alternative to property tax to fund some of the burden in the General Fund. • District property tax rates range from a low of $8 to a high of $23 per thousand. • Can currently only use income surtax for ISL and PPEL – not replace current General Fund property taxes.

Local Option Income Surtax for General Fund • Solution: • Allow a school district to impose a income surtax (reverse referendum) for maximum of 10 years to replace a portion of property taxes in the formula. • Maximum surtax cannot exceed current law of 20% . • Guaranteed dollar for dollar property tax reductions. • Local decision – based on local conditions and values.

Categoricals and Overhead Expenses • Problem: “Overhead” costs are not allowed from categorical funding sources and this places an unfair burden on Regular Program funding. • Solution: • Districts may allocate up to 5% annually for overhead for any categorical program except Teacher Salary Supplement and Professional Development.

Categoricals and Overhead Expenses • Recognizes that categorical funding sources have an impact on administration costs. • Standardizes and simplifies accounting and oversight. • Does not disadvantage regular education students to the benefit of categorical funded students.

Increase Uniform Levy and Raise Foundation Percentage • Problem: Property tax buydown legislation has not been funded adequately and is subject to annual appropriation. • Reduction in Use Tax receipts which were to fund the buydown by $17 million resulted in higher property tax rates. • Annual appropriation places districts in position of not knowing buydown amounts when they set their budgets.

Increase Uniform Levy and Raise Foundation Percentage • Solution: • Increase the Uniform Levy to $8.00 per thousand and raise the State Foundation Percentage to a level that produces the same amount of state foundation aid. • Hold harmless any increases. • Takes the annual appropriation out of the mix. • Funding cannot be cut by the legislature because it would be part of State Aid rather than separate appropriation (PTER fund.)

General Fund: State and Local $ A per pupil look at proposal to raise uniform levy and foundation threshold equally Average Valuation (uniform increase offset by additional levy decrease) Property Richest (held harmless from property tax increase) Property Poorest (uniform increase less than additional levy decrease) Additional Levy State Aid Uniform Levy

Equalize the Cost per Pupil • Problem: The amount of formula spending authority is not equal per student. About half of the districts are at the state minimum ($5,883) and about half have a higher amount. • Creates a student inequity – some kids are worth more than others. • Creates a taxpayer inequity – all of the amount above the state minimum is 100% property tax (no state aid).

Equalize the Cost per Pupil • Solution: • Equalize the amount per pupil by raising the per pupil amount from the minimum to the maximum ($5,883 to $6,058 – deviation of $175 per pupil 3.0%). • Phase in over 4 year period ($44 increase per year). Fully implemented cost is $71 million (split between property tax and state aid) • Equalizes the amount per pupil and also results in lower property taxes in those schools that are over the minimum.

Equalize Tax Rate Impact of On-Time Funding • Problem: Because the formula uses prior year enrollment, growing districts must fund this expense solely from property tax. • Creates taxpayer inequity because some growing districts are property rich and others property poor = higher/lower rate. • Districts have no choice but to serve students and consistently growing districts have higher cash demands.

Equalize Tax Rate Impact of On-Time Funding Property Tax Relief: $38 million

Equalize Tax Rate Impact of On-Time Funding • Solution: • Fully equalize the tax rate impact of funding on-time funding. • State buys all rates down to the whatever is annually calculated as the lowest rate impact per student. • Administered by DOM as part of the Property Tax Equity and Relief Fund.

Set and Fund Reasonable Allowable Growth • Problem: Low/no allowable growth produces financial crises in school budgets over the long run. • Districts must still collectively bargain benefits with staff including insurance benefits – districts only have control of the number of staff they bring back the following year. • Other cost increases occur whether or not per student total funding does not increase.

Set and Fund Reasonable Allowable Growth • Solution: Return Allowable Growth to formula based amount – supermajority (2/3 of each chamber) to override. • Provides funding based upon cost increases faced by districts. • Removes as political decision. • Provides predictable and sustainable funding for schools.

Dropout Prevention Funding Changes • Problem: Dropout prevention is limited for every district regardless of local need. • Each district currently receives a maximum amount of 5% of Regular Program. • Some districts serve a much greater number of at-risk students than others. • Funded effectively by all property tax – so just increasing the amount allowable has negative taxpayer equity consequences.

Dropout Prevention Funding Changes Solution • Add 0.3 weighting component to Dropout Prevention for each identified student. • Weighted component funded with a mix of property tax and state aid – so produces less taxpayer inequity than just increasing the percentage. • Roll existing at-risk funding from the formula into Dropout Prevention. • State match for some of the property tax remaining would promote equity and broad tax relief.

Dropout Prevention Funding Changes • Recognizes that every district has students at-risk. • Places additional resources in those districts that have more at-risk students. • Is more fair to property taxpayers. • Adding existing at-risk funding stream minimizes confusion, streamlines funding and improves local accountability.

Transportation Costs • Problem: Some districts pay virtually nothing out of General Fund for transportation costs while others spend over 10 percent of General Fund just getting students to the door of the schoolhouse. • Impediment to reorganization – school transportation costs simply replace savings due to reorganization. • Equity issue for students – some receive less funding than others.

Transportation Costs • Solution: • Remove transportation costs from General Fund and place in Transportation Fund. • Formula driven – create a per pupil amount of transportation each district receives based on actual costs. • 75% based on vehicle miles in base year. • 25% on number of students transported. • Transportation AG set by DE annually based on national index of cost per vehicle mile. • Legislature reviews formula every five years.

Sparsity of Population Weighting • Problem: Current finance formula doesn’t take into account that there are districts in the state which are so large they cannot be made larger. • Some areas of the state will always operate with fewer children (and hence revenue) per classroom and yet costs are not different.

Sparsity of Population Weighting • Solution: • Weighting based formula based on population density – Regular Education weighting of 0.1 students. • Requirements: • District land area must exceed ½ land area of average county. • Must exceed 300 students to receive weighting. • May only be used for funding educational program.

Innovation Fund • Problem: Barriers to innovative programs/processes are hard to overcome. • Local barriers include resistance to change, uncertainty and fear. • State barriers include Dillon’s rule, current waiver process and ???

Innovation Fund • Solution: Creation of State Innovation Fund. • $25 million fund for innovative projects that improve cost effectiveness of student achievement, improve business practices or otherwise improve sharing of information. • Districts would have to provide a 50% local match. • Expenditures would be exempt from provisions of Dillon’s rule.

Extend/Enhance Sharing Incentives • Problem: Major sharing incentives are expiring. • Current Operational Efficiency and Whole-Grade Sharing incentives have been successful at promoting consolidation. Both expiring in FY 2014. • Operational Efficiency incentive allowed five positions to be shared, but more opportunities exist. • Increased sharing leads to more mergers.