Download

1 / 18

190 likes | 414 Views

START-UP COSTS and CAPITAL SOURCES. by Jim Chamberlain Management Counselor James.Chamberlain@SCORE114.org. START UP COSTS. IF YOU DON’T HAVE ENOUGH CASH TO START YOUR BUSINESS RIGHT, WAIT UNTIL YOU CAN. BUSINESS PLAN WILL HELP Gateway Business Bank.

E N D

START-UP COSTS and CAPITAL SOURCES by Jim Chamberlain Management Counselor James.Chamberlain@SCORE114.org

START UP COSTS • IF YOU DON’T HAVE ENOUGH CASH TO START YOUR BUSINESS RIGHT, WAIT UNTIL YOU CAN. • BUSINESS PLAN WILL HELP Gateway Business Bank

START-UP COSTS and CAPITAL SOURCES • START-UP CASH INVESTMENT FIXED CAPITAL INVESTMENTS • START UP • GROWTH • MAINTENANCE WORKING CAPITAL INVESTMENTS • START UP • GROWTH • MAINTENANCE CASH OUTLAYS UNTIL BREAKEVEN

START-UP COSTS and CAPITAL SOURCES • FIXED CAPITAL – How do you calculate how much your business needs at start-up and to maintain growth? Do not confuse the justification with how it will be financed. Justify first, then determine how to finance the investments. SALES FORECAST – 24 to 36 months How much “capacity” investment is required? How fast will you grow? New products or services?

START-UP COSTS and CAPITAL SOURCES • WORKING CAPITAL INVESTMENTS – The excess of current assets over current liabilities or the amount of cash required to fund the business on a day-to-day basis. An indication of short-term financial strength. Don’t be under-capitalized. • No business has ever failed because they had too much working capital. Working Capital = CURRENT ASSETS minus CURRENT LIABILITIES

START-UP COSTS (INVESTMENTS) FIXED CAPITAL Office Furniture $ 2,000 Vehicles 20,000 Tenant Improvements 10,000 Printing Machines 20,000 Total Fixed Capital – start-up $52,000 Vehicles $ 20,000 Printing Machines 10,000 Total Fixed Capital – Year Two $ 30,000

START-UP COSTS (INVESTMENTS) WORKING CAPITAL Start-up Operating Cash $ 10,000 Inventories 15,000 Prepaid Rent 5,000 Prepaid Insurance 8,000 Total Working Capital – start-up $ 38,000 Cash losses – first six months $ 25,000 Total Working Capital – Year One $ 63,000 Required Working Capital – Year Two $ 10,000 (Based on a $50,000 increase in sales)

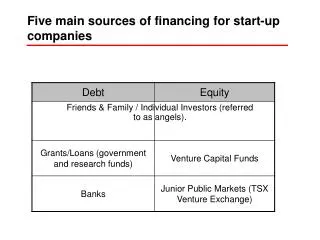

CAPITAL SOURCES HOW BUSINESS ARE REALLY FUNDED Seed Cash – Percentage of Inc 500 CEOs surveyed (2002) who launched their company with seed capital (including personal assets) of: Less than $1,000 14% $1,000 - $10,000 27% $10,001 - $20,000 10% $20,001 - $50,000 15% $50,001 - $100,000 12% More than $100,000 22%

CAPITAL SOURCES • EQUITY FUNDING – Financing your business by selling a minority equity interest. This cash is less risky but more expensive. Valuation issues must be addressed. Initial and target valuation calculations must be made. 43% of founders started the company alone. The rest had: 1 partner 12% 2-3 partners 36% 4+ partners 9%

CAPITAL SOURCES Private Equity and Venture Capital funding Angel investors tend to like proprietary products and non-capital intensive businesses. They anticipate future rounds of financing. Angel investors look for: • Market niches – potential to dominate or be #1 or #2 in the industry • Advanced technology and a disruptive model (going to change things) • Compelling and sustainable advantage – not “me too” • Planned exit in 4-6 years • Reasonable valuation • Performance equal to 5 -10 times original investment • ROI equal to 20-40% per year • Sitting on your board but not having control • Higher risk business models • Angels spend, on average, 51 hours on due diligence per investment

CAPITAL SOURCES BANK LOANS or DEBT FINANCING • Banks will loan 2.5 – 4.0 times Cash Flow – usually based on EBITDA • Banks would like to see a 3-5 year track record or a history of business experience • Debt is less expensive but more risky than equity • Banks will not lend on pure projections: You must have a history of cash flow or a current personal guarantee. • Three sources of repayment: • Cash Flow • Liquidation value of assets • Personal Guarantees of each 25% equity owner

CAPITAL SOURCES NEGATIVES TO A BANKER • Getting involved with something outside your normal business model • Absentee management / ownership • Divorce • Burnout • Growing beyond owner’s capacity to operate the business • Parent turns over business to son or daughter • Computer conversions • Relocation and / or expansion of facility • Companies “hit the wall” at: • Manufacturing companies at $2 million in sales • Distribution companies at $4 million in sales • Retailers at 3 stores and distance • Service companies at 12 employees • Contractors at 2 or more big jobs

CAPITAL SOURCES A bank would rather see a 640 FICO score with all payments as agreed (no late payments, foreclosures, repossessions, charge offs or collection accounts) than a 740 FICO score with a past foreclosure, and three previously delinquent accounts now paid. Having a stable source of income to meet personal income requirements can be a significant factor in reducing business risk for a start-up.

CAPITAL SOURCES QUESTIONS A BANKER WILL ASK YOU • Do you have a Business Plan? • How much experience do you have in this industry? • How is your credit and how much personal debt do you have? • How much is your down payment? Is it at least 25%? • How much collateral do you have? • Who is the competition? • Do you have personal and business insurance? • Do you have services of an accountant and attorney? • Have you ever filed for bankruptcy? • Do you have 2-4 years of tax returns available?

CAPITAL SOURCES SBA ELIGIBILITY • Cannot be a business in lending, life insurance, real estate development or rental property. • Gambling, promoting religion, pyramid sales plans, consumer marketing cooperatives and persons of poor character are ineligible. • Individuals must be lawfully in the U.S. • Business cannot be located outside the U.S. • Import businesses may be ineligible Go to www.SBA.gov for a complete list of ineligible businesses. Also, a good resource for minority and micro-loan plans.

CAPITAL SOURCES MISTAKES ENTREPRENEURS MAKE WHEN RAISING CAPITAL • Don’t understand share prices or valuations • Confuse broad market with served market • Make unrealistic assumptions about an exit strategy • Don’t understand long term capital needs • Have no clue about competition • Don’t understand that marketing beats technology 9 out of 10 times • Write a poor executive summary • Use “off the wall” numbers or pull numbers from thin air • Lack focus; e.g. many products or niches • Develop too simplistic of a market plan / analysis • Underestimate expenses • Rely on financial plans with major inconsistencies; e.g. numbers don’t match or tie • Speak in “techno-jargon”. No one understands what they are saying

CAPITAL SOURCES BEST WAYS TO IRRITATE AN INVESTOR • Lying to investors or not being forthright; omission of material information • Inability to answer direct questions with direct answers • Surprises; e.g. problem with credit checks, hidden liabilities or debts • Over hype or exaggerate upside • Your story always changes • Arguing with investors • Late for meetings • Excessive secrecy or legalese; expect investor to sign NDA • Investing capital in fancy facility and furniture • Fail to attract top talent

QUESTIONS ? SCORE JIM CHAMBERLAIN James.Chamberlain@SCORE114.org