Download

1 / 22

220 likes | 316 Views

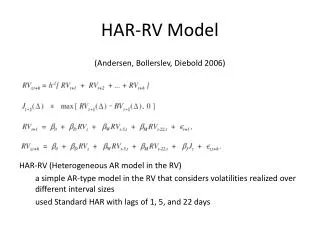

High Volatile Markets HAR-RV and Macroeconomic News. Motivation. Examine how HAR-RV model differs in the financial sector data from 1997 compared to post July 2007 and post September 15 2008 Examine how Macroeconomic News: Feds Fund Rate and the Nonfarm Payroll Announcements Affect RV.

E N D

Motivation • Examine how HAR-RV model differs in the financial sector data from 1997 compared to post July 2007 and post September 15 2008 • Examine how Macroeconomic News: Feds Fund Rate and the Nonfarm Payroll Announcements Affect RV

Financial Sector Data • JPM (JP Morgan) • BK (new) (Bank of New York Mellon) • BAC (Bank of America) • AXP (American Express) • ALL (Allstate) • Others Not Included Because of Data Differences

Financial Sector Data • Equally Weighted • Modify data so that stock splits do not affect the RV • Portfolio: 4/10/1997 through 1/7/2009 (equally weighted)

Regressing Employment Error at t on RV(t) Regressing Employment Error at t on RV(t+1)

Final Research • Continue to Examine Other Macroeconomic Indicators Effect on HAR-RV Model