Download

1 / 27

270 likes | 430 Views

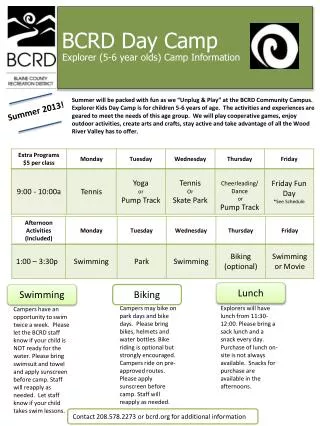

ALASBO Power Lunch. Time and Effort Reporting. General Outline of Training. Purpose and Learning Objectives Training Topic Questions. PURPOSE. Discuss regulatory authority and requirements for federal grant time & effort reporting. Learning Objectives. Source of regulatory authority

E N D

ALASBO Power Lunch Time and Effort Reporting 7/22/10

General Outline of Training • Purpose and Learning Objectives • Training Topic • Questions 7/22/10

PURPOSE Discuss regulatory authority and requirements for federal grant time & effort reporting 7/22/10

Learning Objectives • Source of regulatory authority • Time and effort requirements • Sample time and effort documentation 7/22/10

Time and Effort Reporting – Where are the Requirements? • Required under OMB’s Circular A-87, Cost Principles for State, Local, and Indian Tribal Governments • Attachment B, Selected Items of Cost, Item 11, Compensation for Personnel Services, para. h, Support of Salaries and Wages. 7/22/10

When is Time and Effort Reporting Required? • Time and effort reporting is required when any part of an individual’s salary is: • Charged to a federal program. • Used as a required match for a federal program (even though not charged to a federal program). 7/22/10

When is Time and Effort Reporting Required (cont.)? • Must demonstrate=If employee paid with federal funds, then employee worked on that specific federal program and/or cost objective. 7/22/10

Terminology Differences • Payroll records • Worked 8:00 to 5:00 • Time and effort records • Worked 50% on Title I administration and 50% on non-federal 7/22/10

What Type of Reporting is Required? • Single or blended cost objective • Semi annual certification • Multiple cost objectives • Personnel activity reports (PARs) 7/22/10

What is a “Cost Objective” • Circular A-87 Definition: A function, organizational subdivision, contract, grant or other activity for which cost data are needed and for which costs are incurred. 7/22/10

Typical Examples of a Single Cost Objective • Federal Program: Title I Part A; Carl Perkins; IDEA; ARRA Stimulus and Stabilization Grants • Federal Program Cost Objective: • Title I Program Services; • Title I Administration; • Title I Parent Involvement; • Stabilization Grant; 7/22/10

Typical Examples of Multiple Cost Objectives If an employee works on: • More than one federal award (with different cost objectives); • A federal award and a non-federal award (with different cost objectives); • A federal award with specific earmarking or matching requirements 7/22/10

“Blended” Cost Objective Cost objective as defined in the Montana Compact: • A set of work activities that are allowable to one or more funding sources and which may be funded out of a variety of eligible funding sources where the activities and purposes or population served are not distinguishable. 7/22/10

“Blended” Cost Objective (cont.) • Provides flexibility because focus is on “work activity” • OK to simply report activity and not specific federal program cost objective • Activity must be allowable under grant 7/22/10

Typical Examples of a Blended Cost Objective The set of work activities allowable under: • Federal IDEA funds and State and/or local special education funds • Professional development that is allowable under more than one federal program (i.e., professional development that is authorized under Titles I, II, and V) • A federal program and its state/local match 7/22/10

What is a semi-annual certification? • Statement individual(s) worked solely on activities related to a single (or blended) cost objective • Completed at least every six months • Signed by employee or supervisor with first-hand knowledge of work performed 7/22/10

Sample Semi-Annual Certification • If employee is subject to semi-annual certification, send certification to direct supervisors twice a year. • Consider using two different certifications: • Single Cost Objective, and Single Cost Objective 7/22/10

Sample Semi-Annual Certification (cont.) • Two different certifications (cont): • Single Grant Single Grant 7/22/10

What is a Bi-Weekly Personnel Activity Report (PAR)? • Accounts for total employee effort as units of time as opposed to percentages. • Prepared & signed at least monthly (must coincide w/one or more pay periods). • Must be Signed by employee. 7/22/10

What is a Bi-Weekly PAR (cont.)? • Reflects actual work performed (not budgeted % or FTE). • Agrees to supporting documentation. 7/22/10

What Type of PAR Supporting documentation is Needed? • Requires a judgment call • Examples include, but are not limited to: • Lesson plans • Calendar notes • Time log 7/22/10

Sample Personnel Activity Report 7/22/10

When is a PAR “Reconciliation” Required? • IF: Payroll is processed based on budgeted or estimated time and effort. • THEN: Payroll records must be compared to time and effort reports as least quarterly. 7/22/10

When is an Accounting Adjustment Required? If the qtrly difference is 10% or more: • Payroll charges must be adjusted at the time of comparison. • AND: The following quarter’s estimate must be adjusted to more closely reflect actual activity. If the qtrly difference is less than 10%: • No action required until next quarterly reconciliation. • BUT: Difference between estimated and actual time as supported by time and effort reports must be adjusted at year-end regardless of size. 7/22/10

Sample PAR Reconciliation • The leave analysis box at the bottom allows us to allocate leave taken during the pay period to the various funding sources based on actual hours worked. • Pay attention to the difference between actual effort and budgeted effort. 7/22/10

Determination of Semi-Annual Certification or PAR • Sample of form you might use for: • Employees new to the District • Employees transferring to your grant • Terminating employees if no rehire. • Helps determines if the position is subject to semi-annual certification or PAR reporting. 7/22/10

Time and Effort Reporting • General discussion • Questions? 7/22/10