Download

1 / 8

80 likes | 106 Views

Aleksey Krylov Waterfall Analysis Case Study 07-21-2023

E N D

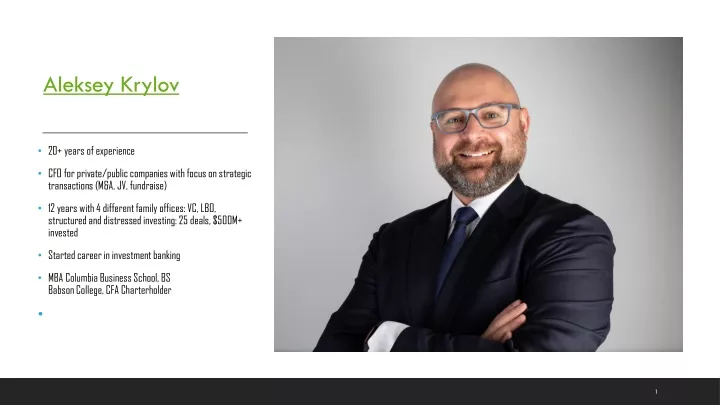

Aleksey Krylov • 20+ years of experience • CFO for private/public companies with focus on strategic transactions (M&A, JV, fundraise) • 12 years with 4 different family offices: VC, LBO, structured and distressed investing: 25 deals, $500M+ invested • Started career in investment banking • MBA Columbia Business School, BS Babson College, CFA Charterholder • 1

Sunrun example: Business will drive financing structures 1. Seed 2. Series A 3. Senior Secured Debt “Particulars of a funding round often reflect strategic goals the company is targeting in the next 12-18 months,” - Aleksey Krylov 2

Waterfall analysis Frequent structures TOC Example 3

Scenario #1 1) Founder launched the business with $0 – CEO, Sales & Marketing ◦ 1.1) Founder found a co-founder, took $0 – CTO – for 35% of the business 2) Angel investors put in $500,000 via convertible note, capped at $10M, 5% interest 3) Series A investors put in $5M via pref @$15M pre “One has to consider several funding paths and optimize transaction structuring for downside risk,” - Aleksey Krylov 4) Series B investors put in $20M via pref @$65M pre 5) IPO investors put in $50M via common @$100M pre 4

Scenario #2 1) Founder launched the business with $0 – CEO, Sales & Marketing 1.1) Founder found a co-founder, took $0 – CTO – for 35% of the business 2) Angel investors put in $500,000 via convertible note, capped at $10M, 5% interest “Sometime the startup needs to raise capital at the most inopportune time and incur strong dilution,” - Aleksey Krylov 3) Series A investors put in $10M via pref @$50M pre 4) Series B investors put in $10M via pref @$25M pre 5) IPO investors put in $50M via common @$100M pre 5

Protections ROFR ? Anti-dilution ◦ WA? ◦ Full-ratchet? “Negotiated protections can help protect investor rights and economic interest,” - Aleksey Krylov Dividends ? 6

Scenario #3 1) Founder launched the business with $0 – CEO, Sales & Marketing 1.1) Founder found a co-founder, took $0 – CTO – for 35% of the business 2) Angel investors put in $500,000 via convertible note, capped at $10M, 5% interest 3) Series A investors put in $10M via pref @$50M pre “Capturing upside through creative structuring is a balancing act between being greedy and getting deal done,” - Aleksey Krylov 4) Series B investors put in $10M via pref @$25M pre 5) 7

Scenario #3 – liquidation • IP Value sold for $12.5M • Liquidation – waterfall triggered • Series B gets $10M + (remember dividends and/or liquidation preference) • Series A gets $2.5M • Angels get zero “No one wants to hit the brick wall but it happens…,” - Aleksey Krylov • Common gets zero 8